Last month, the Justice Department cleared the merger between two giants of the entertainment industry, with Paramount agreeing to pay $110 billion to take over Warner Bros. Discovery. The Antitrust Division ostensibly looked at the markets for streaming, cable, and movie studios, and evidently felt the merger would not generate anticompetitive effects. That sentiment was not shared, however, by the twelve states that sued to block the merger days later. And just this week, the Writers Guild of America (WGA) filed its own lawsuit seeking to stop the deal, arguing it would suppress writers’ pay and reduce employment opportunities.

The WGA is right to sound the alarm. Much of the attention so far, however, focused on one theory of harm—a reduction in the number of television shows and films will reduce the demand for talent in the labor market, leading to lower wages. We want to bring to light a separate, more direct mechanism: the elimination of an outside employment option, and what it does to workers’ bargaining power.

Right now, seven companies compete to buy scripted television shows and films: Netflix, Disney, Amazon, Apple, NBCUniversal, Paramount, and Warner Bros. Discovery. After this merger, it will be six. It may seem like a small decline, but it could make a big difference in compensation.

Think of every writer’s deal, or every director’s overall contract, as the outcome of an auction: each studio solves for its best response given what it expects rivals to bid, and the winning offer is set by how hard the next best bidder is willing to push. If we take one bidder out of the game, then every remaining studio’s best response is to temper its bid. They can win the same talent with a lower offer, because there is one less rival forcing them to bid aggressively.

It bears noting that this direct mechanism of harm does not depend on how many shows get made. Paramount could keep every promise it makes about output, and writers would still end up worse off, because the auction in which their work is being sold has one less buyer.

Closing career doors

The proposed merger is not merely a horizontal combination of two employers. The two companies are vertically integrated companies that control both the production and various routes through which content reaches audiences.

Today, if a television project is rejected by Paramount, the project may still be taken to Warner with a shot at gaining access to HBO Max, HBO, TNT, or another Warner Bros. affiliated outlet. And the same is true for a project rejected by Warner. After the merger, however, those routes would lead back to one corporate owner. As the WGA complaint stresses, rejection by the combined company would shut down writers out of Paramount Pictures, Warner Bros., Paramount+, HBO Max, and a much wider collection of affiliated distribution channels simultaneously.

This is more severe than merely losing a bid. A writer may be willing to accept less money to get their project made, but that willingness provides little leverage if the company rejecting the project controls several of the important routes through which the production reaches the audience.

The independent producers of shows or films face a very similar dilemma. They may develop a promising show. Lacking financing, however, they are eventually forced to ask large distributors or platforms to carry their work to fruition. Yet a vertically integrated distributor has an incentive to favor content produced by its own affiliated studio, as the parent corporation retains more of the resulting value.

An anticompetitive presumption

We do not need an auction model to assess the merger’s impact on workers. The states suing to block the merger built their own concentration measure using the Herfindahl-Hirschman Index (HHI) for the three markets they examined: wide-release theatrical films, blockbuster films, and basic cable licensing. All three HHIs land above 2,000 post-merger, with merger-induced increases in HHI ranging from 321 to 445 points. Under the antitrust agencies’ 2023 Merger Guidelines, any deal that raises the HHI by more than 100 points and leaves a market above 1,800 is presumed anticompetitive. All three of the states’ own numbers clear that line comfortably.

We estimated our own HHIs for theatrical releases and counted productions rather than box office revenue. That metric might be a better proxy for how many times a studio actually goes out and hires a cast and crew.

The resulting HHI moves from 1,594 pre-merger to 1,938 post-merger, an increase of 344. No matter how we look at it, this industry was already concentrated, and this merger pushes it well past the threshold the government itself uses to presume a deal illegal.

Blocking a merger based on labor harms is not a novel antitrust theory. In 2022, the Justice Department blocked Penguin Random House from acquiring Simon & Schuster on almost an identical theory of harm. Combining two of the biggest buyers of books would leave authors with fewer publishers bidding for their work, squeezing compensation. At trial, the DOJ’s expert built an auction model of how publishers compete for manuscripts. The model estimated what happens to an author’s advance when one of those bidders disappears. Penguin Random House’s advances would decline by 4.3 percent, about $44,000 a book. And Simon & Schuster’s advances would shrink by 11.6 percent, about $105,000 a book. Based in part on this model, the judge sided with the government and blocked the deal.

We are not claiming the numbers would be identical for screenwriters or directors. Only the merging parties possess the contract-level data to run that calculation for Hollywood the way the DOJ’s expert ran it for publishing. But it does mean the mechanism itself has already been tested in court and held up.

Having said that, Paramount has promised various preemptive remedies such as running studios independently, or a commitment to produce a fixed number of shows or films in a year. But none of those promises touches the direct pathway to harm articulated here. A commitment to hold output steady would do nothing to reduce the number of companies bidding on the same writer, putting downward pressure on compensation.

Paramount’s case against the merger

When Paramount’s rival Netflix was aiming to acquire Warner, Paramount argued in a December 2025 SEC filing that competition among streaming services keeps Netflix paying fair prices to creators and producers:

A combined Netflix-WBD would so dominate subscription streaming that it would gain the market power to raise prices with little or no fear of losing subscribers, while underpaying creators and talent with little or no fear of those projects going to competitor services. That’s exactly the kind of harm antitrust law guards against, which is why we expect regulators in the US and elsewhere will block the proposed deal were it to move forward.

That is the same mechanism spelled out here. Paramount cannot consistently argue that a merger between Netflix and Warner would harm talent, while a merger between Paramount and Warner Bros. will not. The identity of the purchaser has changed, but the economics is the same.

Paramount might respond to the concerns by saying that the transaction would strengthen competition with Netflix and Amazon and preserve theatrical distribution. Those claims can be evaluated separately. Yet none explain how the removal of a bidder in the labor market benefits creators.

Promises, promises

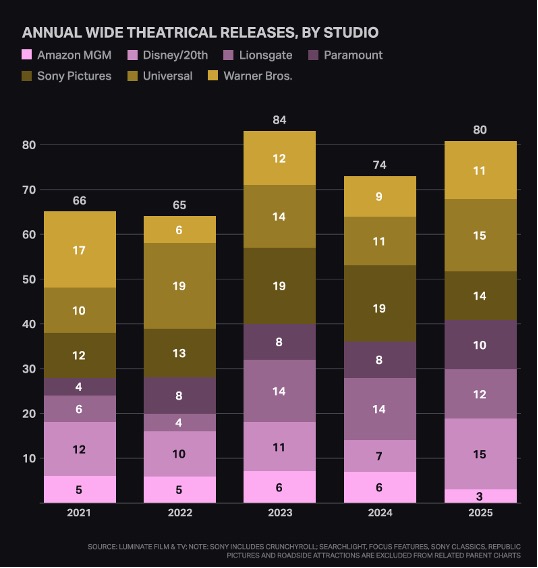

Pledges by merger parties to preserve output have a track record of not delivering. To wit, Warner Bros. promised 16 theatrical films in 2023 as part of his push to convince theater owners the studio was recommitting to film after its Discovery merger; it delivered only eleven. It promised more than 20 in 2024 and delivered only nine.

Penguin Random House also made promises during its own acquisition—namely, that its imprints would keep bidding against each other independently. But testimony from its own president revealed they would not bid against each other, because, in his own words, they were the “same company,” and bidding against each other would just be “driving up the price of an auction amongst ourselves.”

If there’s any doubt about whether to credit these promises to preserve output, look no farther than the last major merger among studios. When Disney acquired 20th Century Fox in 2019, output collapsed. Indeed, Fox’s theatrical output was cut by more than half in a few years.

In any event, as explained above, workers can suffer without an output reduction. Writers and directors can be harmed directly via the reduction of an output employment option. An output reduction is a sufficient but not necessary condition for worker harm. That output will likely fall, as it did when Fox was acquired, simply means that workers can suffer indirectly as well.

Finally, Paramount’s production pledge assumes that every film represents the same kind of opportunity. Yet studios are not identical for buyers. Each has its own executives, franchises, audience strategy, distribution model, tolerance for risk, and appetite for particular genres. The number of employers existing on paper thus is much larger than the number genuinely interested in purchasing a specific kind of project.

According to David Koepp, the screenwriter of films including Jurassic Park and Mission Impossible, when Disney acquired Fox, writers stopped treating Fox as a destination for original adult thrillers, political dramas, and mid-budget character pieces because its unique creative identity had been absorbed into Disney’s franchise-centered strategy. Rather than migrating to Disney, Fox buyers simply disappeared.

A commitment to fix production thus does not preserve this diversity of demand. Paramount could easily make 30 films by replacing original films with sequels, mid-budget projects with franchise extensions, or independently developed stories with material drawn from its own library. With this approach, the title count will remain constant while entire categories of writers will lose meaningful buyers. And it is this direct pathway to labor harm that is most concerning.

Ahmad Rafay Abid is a rising senior at Colby College, majoring in economics and physics. Devesh Ray is an economics graduate student at Columbia University. Both are summer analysts at Econ One.