This piece originally appeared in ProMarket but was subsequently retracted, with the following blurb (agreed-upon language between ProMarket’s Luigi Zingales and the authors):

“ProMarket published the article “The Antitrust Output Goal Cannot Measure Welfare.” The main claim of the article was that “a shift out in a production possibility frontier does not necessarily increase welfare, as assessed by a social welfare function.” The published version was unclear on whether the theorem contained in the article was a statement about an equilibrium outcome or a mere existence claim, regardless of the possibility that this outcome might occur in equilibrium. When we asked the authors to clarify, they stated that their claim regarded only the existence of such points, not their occurrence in equilibrium. After this clarification, ProMarket decided that the article was uninteresting and withdrew its publication.”

The source of the complaint that caused the retraction was, according to Zingales, a ProMarket Advisory Board member. The authors had no contact with that person, nor do we know who it is. We would have welcomed published scholarly debate versus retraction compelled by an anonymous Board Member.

We reproduce the piece in its entirety here. In addition, we provide our proposed revision to the piece, which we wrote to clear up the confusion that it was claimed was created by the first piece. We will let our readers be the judge of the piece’s interest. Of course, if you have any criticisms, we welcome professional scholarly debate.

(By the way, given that the piece never mentions supply or demand or prices, it is a mystery to us why any competent economist could have thought it was about “equilibrium.” But perhaps “equilibrium” was a pretext for removing the article for other reasons.)

The Antitrust Output Goal Cannot Measure Welfare (ORIGINAL POST)

Many antitrust scholars and practitioners use output to measure welfare. Darren Bush, Gabriel A. Lozada, and Mark Glick write that this association fails on theoretical grounds and that ideas of welfare require a much more sophisticated understanding.

By Darren Bush, Gabriel A. Lozada, and Mark Glick

Debate seems to have pivoted in the discourse on consumer welfare theory to the question of whether welfare can be indirectly measured based upon output. The tamest of these claims is not that output measures welfare, but that generally, output increases are associated with increases in economic welfare.

This claim, even at its tamest, is false. For one, welfare depends on more than just output, and increasing output may detrimentally affect some of the other factors which welfare depends on. For example, increasing output may cause working conditions to deteriorate; may cause competing firms to close, resulting in increased unemployment, regional deindustrialization, and fewer avenues for small business formation; may increase pollution; may increase the political power of the growing firm, resulting in more public policy controversies and, yes, more lawsuits being decided in its interest; and may adversely affect suppliers.

Even if we completely ignore those realities, it is still possible for an increase in output to reduce welfare. These two short proofs show that even in the complete absence of these other effects—that is, even if we assume that people obtain welfare exclusively by receiving commodities, which they always want more of—increasing output may reduce welfare.

We will first prove that it is possible for an increase in output to reduce welfare under the assumption that welfare is assessed by a social planner. Then we will prove it assuming no social planner, so that welfare is assessed strictly via individuals’ utility levels.

The Social Planner Proof

Here we show that a shift out in a production possibility frontier does not necessarily increase welfare, as assessed by a social welfare function.

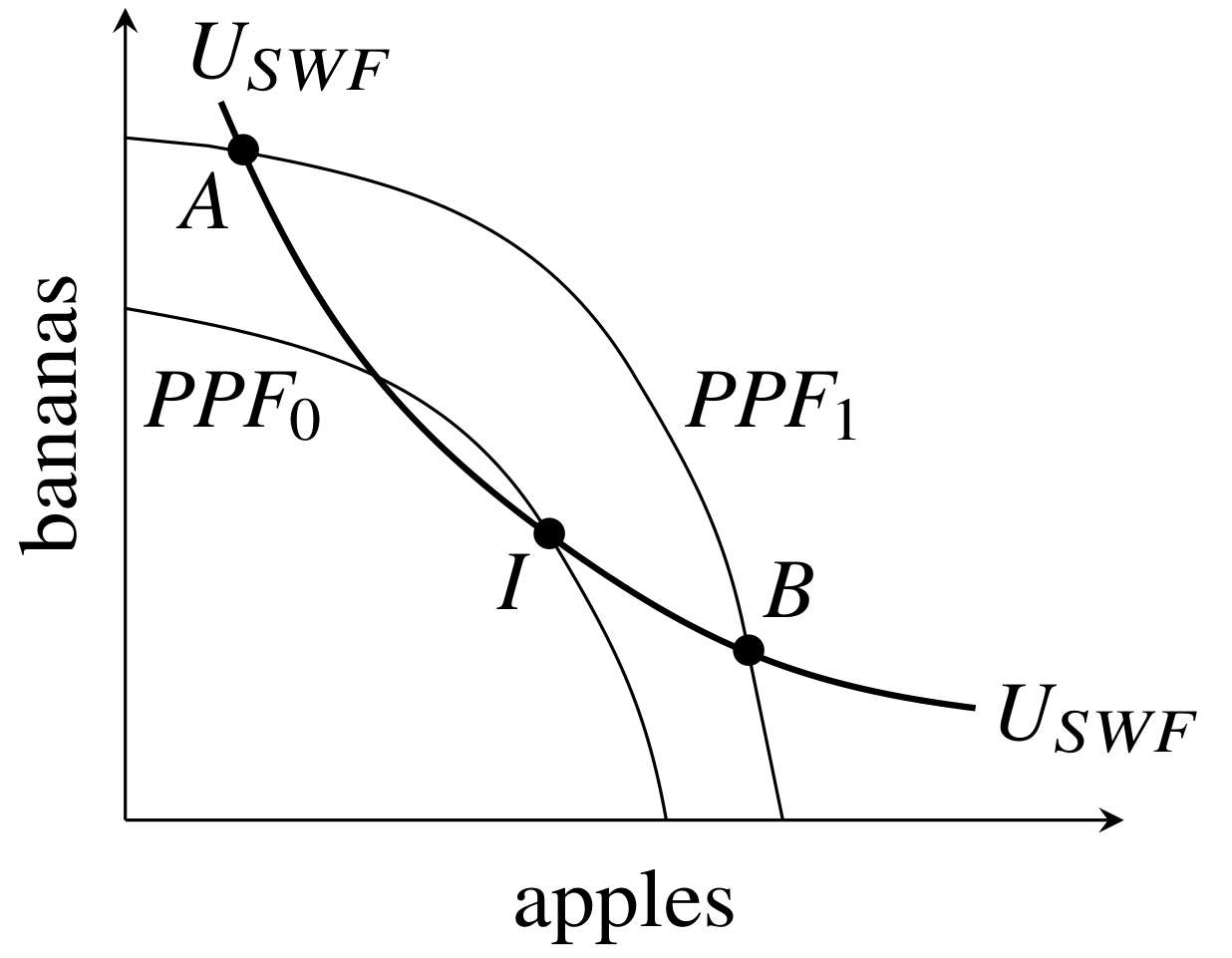

Suppose in the figure below that the original production possibility frontier is PPF0 and

the new production possibility frontier is PPF1. Let USWF be the original level of social welfare, so that the curve in the diagram labeled USWF is the social indifference curve when the technology is represented by PPF0. This implies that when the technology is at PPF0, society chooses the socially optimal point, I, on PPF0. Next, suppose there is an increase in potential output, to PPF1. If society moves to a point on PPF1 which is above and to the left of point A, or is below and to the right of point B, then society will be worse off on PPF1 than it was on PPF0. Even though output increased, depending on the social indifference curve and the composition of the new output, there can be lower social welfare.

The Individual Utility Proof

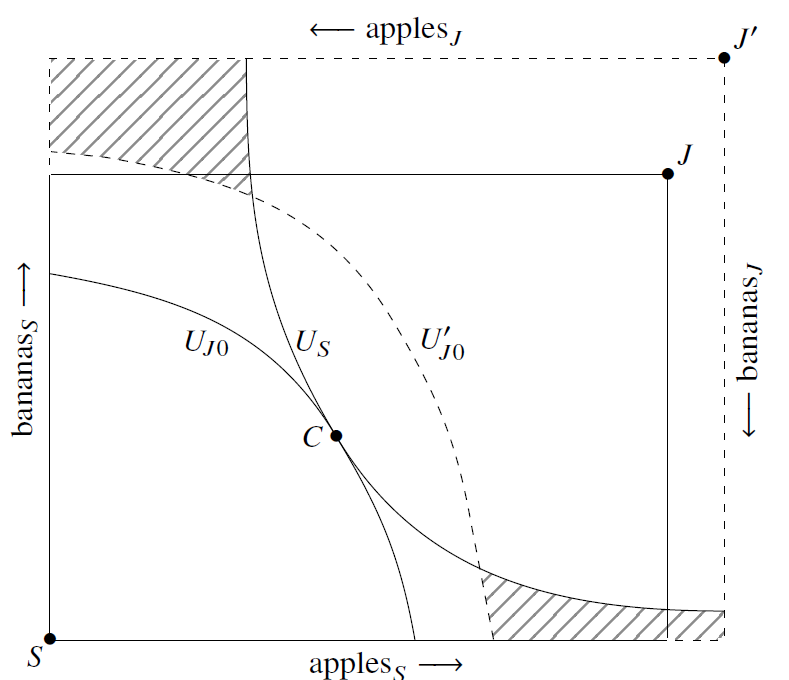

Next, we continue to assume that only consumption of commodities determines welfare, and we show that when output increases every individual can be worse off. Consider the figure below, which represents an initial Edgeworth Box having solid borders, and a new, expanded Edgeworth Box, with dashed borders. The expanded Edgeworth Box represents an increase in output for both apples and bananas, the two goods in this economy.

The original, smaller Edgeworth Box has an origin for Jones labeled J and an origin for Smith labeled S. In this smaller Edgeworth Box, suppose the initial position is at C. The indifference curve UJ0 represents Jones’s initial level of utility with the smaller Edgeworth Box, and the indifference curve US represents Smith’s initial level of utility with the smaller Box. In the larger Edgeworth Box, Jones’s origin shifts from J to J’, and his UJ0 indifference curve correspondingly shifts to UJ0′. Smiths’ US indifference curve does not shift. The hatched areas in the graph are all the allocations in the bigger Edgeworth Box which are worse for both Smith and Jones compared to the original allocation in the smaller Edgeworth Box.

In other words, despite the fact that output has increased, if the new allocation is in the hatched area, then Smith and Jones both prefer the world where output is lower. We get this result because welfare is affected by allocation and distribution as well as by the sheer amount of output, and more output, if mis-allocated or poorly distributed, can decrease welfare.

GDP also does not measure aggregate Welfare

The argument that “output” alone measures welfare sometimes refers not to literal output, as in the two examples above, but to a reified notion of “output.” A good example is GDP. GDP is the aggregated monetary value of all final goods and services, weighted using current prices. Welfare economists, beginning with Richard Easterlin, have understood that GDP does not accurately measure economic well-being. Since prices are used for the aggregation, GDP incorporates the effects of income distribution, but in a way which hides this dependence, making GDP seem value-free although it is not. In addition, using GDP as a measure of welfare deliberately ignores many important welfare effects while only taking into account output. As Amit Kapoor and Bibek Debroy put it:

GDP takes a positive count of the cars we produce but does not account for the emissions they generate; it adds the value of the sugar-laced beverages we sell but fails to subtract the health problems they cause; it includes the value of building new cities but does not discount for the vital forests they replace. As Robert Kennedy put it in his famous election speech in 1968, “it [GDP] measures everything in short, except that which makes life worthwhile.”

Any industry-specific measure of price-weighted “output” or firm-specific measure of price-weighted “output” is similarly flawed.

For these reasons, few, if any, welfare economists would today use GNP alone to assess a nation’s welfare, preferring instead to use a collection of “social indicators.”

Conclusion

Output should not be the sole criterion for antitrust policy. We can do a better job of using competition policy to increase human welfare without this dogma. In this article, we showed that we cannot be certain that output increases welfare even in a purely hypothetical world where welfare depends solely on the output of commodities. In the real world, where welfare depends on a multitude of factors besides output—many of which can be addressed by competition policy—the case against a unilateral output goal is much stronger.

Addendum

The Original Sling posting inadvertently left off the two proposed graphs that we drew as we sought to remedy the Anonymous Board Member’s confusion about “equilibrium.” We now add the graphs we proposed. The explanation of the graphs was similar, and the discussion of GNP was identical to the original version.

The Proof if there is a Social Welfare Function (Revised Graph)

The Individual Utility Proof (Revised Graph)

The New Merger Guidelines (the “Guidelines”) provide a framework for analyzing when proposed mergers likely violate Section 7 of the Clayton Act that is more faithful to controlling law and Congressional intent than earlier Guidelines. The thirteen guidelines presented in the new Guidelines go quite a long way in pulling the Agencies back from an approach that placed undue burden on plaintiffs and ignored important factors such as the trend in market concentration and serial mergers that were addressed by earlier Supreme Court precedent. The Guidelines also incorporate the modern, more objective economics of the post-Chicago school of economics. For these reasons, and others, the Guidelines should be applauded.

Unfortunately, remnants of Judge Bork’s Consumer Welfare Standard remain. In several places the Guidelines refer to a merger’s anticompetitive effects as price, quantity (output), product quality or variety, and innovation. These are all effects that can shift demand curves or equilibrium positions in the output market and thus increase consumer surplus, the only goal recognized by the Consumer Welfare Standard.

To their credit, the Guidelines also mention input markets, referring to mergers that decrease wages, lower benefits or cause working conditions to deteriorate. Lower wages reduce labor surplus (rent), a consideration that would come within a Total Trading Partner Surplus approach. However, the traditional goals of antitrust as articulated by Congress and many Supreme Court opinions, including protecting democracy through dispersion of economic and political power, protection of small business, and preventing unequal income and wealth distribution, are conspicuously absent.

The basis for these traditional goals is well known. Prominent economist Stephen Martin has documented the judicial and congressional statements concerning the antitrust goal of dispersion of power. The historical support for the goal of preserving small business can be found in a recent paper by two of the authors of this piece. Lina Khan and Sandeep Vaheesan, and Robert Lande and Sandeep Vaheesan, have laid out the textual support for the antitrust inequality goal. Moreover, welfare economists have empirically demonstrated significant positive welfare effects from democracy, small business formation, and income equality.

Indeed, the Brown Shoe opinion, on which the Guidelines heavily rely, examined whether the lower court opinion was “consistent with the intent of the legislature” which drafted the 1950 Amendments, and the opinion itself refers to the goal of “protection of small businesses” in at least two places. The legislative history of the 1950 Amendment deemed important by the Brown Shoe Court evinced a clear concern that rising concentration will, according to Senator O’Mahoney, “result in a terrific drive toward a totalitarian government.”

The remnants of the Consumer Welfare Standard are most evident in the Guidelines’ rebuttal section on efficiencies. The Guidelines open the section with the recognition that controlling precedent is clear that efficiencies are not a defense to a merger that violates Section 7; accordingly, the section is offered as a rebuttal rather than a defense. In essence, if the merging parties can identify merger-specific and verifiable efficiencies, it can rebut a finding that the merger substantially lessened competition. The Guidelines do not define “efficiencies.” However, the context makes clear that Guidelines mean to follow previous versions of the Merger Guidelines, that assume “efficiencies” are primarily cost savings. A defendant can offer a rebuttal to a presumption that a merger may significantly harm competition, if such cost savings are passed through to consumers in lower prices, to a degree that offsets any potential post-merger price increase. There are at least six reasons why the Agencies should jettison this “efficiency” rebuttal.

First, lower prices resulting from cost savings are quite a bit different than lower prices resulting from entry (rebuttal by entry). New entry reduces concentration, but cost savings at best will only lower output price, and higher prices (or reduced output) is not the sole problem that results from high concentration except under a strict Consumer Welfare Standard.

Second, to the extent the Guidelines equate efficiencies with cost savings (as in earlier merger guidelines), they have adopted the businessman’s definition of efficiencies. In contrast, economic theory suggests that some cost savings lower rather than raise social welfare. For example, cost savings from lower wages, greater unemployment, or redistribution between stakeholders can both lower welfare and reduce prices. An increase in consumer or producer surplus that comes at the expense of input supplier surplus can also lower welfare.

Third, only under the output-market half of a surplus theory of economic welfare, which is the original Consumer Welfare Standard, can one clearly link cost savings to economic welfare, because lower cost increases consumer and/or producer surplus. As we show elsewhere, this theory has been thoroughly discredited by welfare economists. In fact, for economists, “efficiency” only means Pareto efficiency. As discussed by Gregory Werden and by Mas-Colell et al.’s leading Microeconomics textbook (Chapter 10), the assumptions necessary to ensure that maximizing surplus results in Pareto Efficiency are extreme and unrealistic. These assumptions include quasilinear utility, perfectly competitive other markets, and lump sum wealth redistributions that maximize social welfare. This discredits the surplus approach, which is the only way to reconcile Pareto Efficiency, which is what efficiencies mean in economic theory, with cost savings, which is the definition implied in the Guidelines.

Fourth, the efficiency section is superfluous. As many economists have recognized, most recently Nancy Rose and Jonathan Sallet, the merging parties are already credited for efficiencies (cost savings) in the “standard efficiency credit” which undergirds Guideline 1. After all, absent any efficiencies, why allow any merger that evenly weakly increases concentration? A concentration screen that allows some mergers and not others must be assuming that all mergers come with some socially beneficial cost savings. Why do we need another rebuttal section when cost savings have already been credited?

Fifth, there is no empirical research to suggest that mergers that increase concentration actually lower costs and pass on sufficient benefits to consumers to constitute a successful rebuttal. As one district court commented, “The Court is not aware of any case, and Defendants have cited none, where the merging parties have successfully rebutted the government’s prima facia case on the strength of the efficiencies.” We have identified nine studies measuring either cost savings or productivity gains or profitability from mergers spanning industries like health insurance, banking, utility, manufacturing, beer, and concrete industries. Five of these studies find no evidence of productivity gain or a cost reduction. The other four studies find productivity gains in terms of cost savings; but three of these four studies report a significant increase in prices to the consumers post-merger, and the remaining study does not report price effects post-merger. In other words, we have not been able to find any empirical study showing post-merger pass on of cost savings to consumers. These results are consistent with those of Professor Kwoka, who performs a comprehensive meta-analysis of the price effects of horizontal mergers and finds that the post-merger price at the product-level increases by 7.2 percent on average, holding all other influences constant. More than 80 percent of product prices show increases, and those increases average 10.1 percent.

Sixth, even if there were cost savings from mergers it is unlikely that they would be merger- specific and verifiable. Earlier versions of the Merger Guidelines expressed skepticism that economies of scale or scope could not be achieved by internal expansion (1968 Merger Guidelines) or that cost savings related to “procurement, management or capital costs” would be merger specific (1997 Merger Guidelines). In their article on merger efficiencies, Fisher and Lande write that “it would be extremely difficult for merging firms to prove that they could not attain the anticipated efficiencies or quality improvements through internal expansion.” Louis Kaplow has argued that the ability to use contracting to achieve claimed efficiencies is seriously underappreciated or studied. Verification of future efficiencies is also inherently problematic. The 1997 Merger Guidelines state that efficiencies related to R&D are “less susceptible to verification.” This problem and other verification hurdles are discussed by Joe Brodley and John Kwoka. In summary, the New Merger Guidelines could be improved by a footnote in Guideline One clarifying the multiple antitrust goals Congress sought to achieve by preventing concentrated markets through mergers. In addition, the Agencies should take seriously the holdings of at least three Supreme Court Opinions, none of which have been overturned (Brown Shoe, Phila. Nat’l Bank and Procter & Gamble Co.) that (as quoted in the Guidelines) “possible economies [from a merger] cannot be used as a defense to illegality.” There are good reasons to abandon an efficiencies rebuttal as well.

Mark Glick, Pavitra Govindan and Gabriel A. Lozada are professors in the economics department at the University of Utah. Darren Bush is a professor in the law school at the University of Houston.

In 2023, Columbia University announced that it would no longer be participating in US News’ college rankings. At the time, the conventional interpretation of Columbia’s withdrawal was that it signaled the incoming demise of US News’ college rankings. Yet to date, no other elite undergraduate university has followed Columbia in withdrawing from US News’ undergraduate rankings. Could the conventional interpretation about Columbia’s withdrawal be wrong?

In 1988, Columbia was ranked eighteenth in US News’ college rankings. But in the years that followed, Columbia’s undergraduate rank kept improving. By 2021, Columbia had surged to an all-time high of second. Naturally, Columbia’s breathtaking climb in US News rankings raised questions. What had Columbia done so well? What should Columbia do more of? How could other universities learn from Columbia? Among the people asking these questions was Columbia’s very own math professor, Dr. Michael Thaddeus. Skeptical by nature, he started studying Columbia’s rankings surge. What he found sent shockwaves through higher education.

In February 2022, Dr. Thaddeus released a 21-page report exposing widespread misrepresentation of data provided by Columbia University to US News’ college rankings. For example, Dr. Thaddeus demonstrated that Columbia’s reported spending per student was inflated by “a substantial portion” of the $1.2 billion spent by its hospital on patient care, a function of the university completely unrelated to education. Because US News’ rankings are calculated, in part, by how much an institution spends per student, this overstatement greatly improved Columbia University’s ranking, or at least that’s what Dr. Thaddeus alleged.

At first, Columbia intimated that Dr. Thaddeus was mistaken. Eventually Columbia came clean. In September 2022, Mary Boyce, Columbia’s provost, said in a statement, “We deeply regret the deficiencies in our prior reporting and are committed to doing better.” While Columbia’s acknowledgement was a step in the right direction, it was also silent on a crucial question. What possessed Columbia to lie to US News in the first instance?

In the edition of the US News rankings that followed Columbia’s rankings scandal, Columbia was demoted to a rank of 18th. The drop from second to eighteenth was incredibly steep. Observers wondered how it was computed. Indeed, Columbia hadn’t submitted any new data to US News following Dr. Thaddeus’s report. Instead, US News seemingly arrived at the new ranking without accurate data from Columbia to correct the inaccurate data from the past. The speculative nature of the ranking was on display, but so too was something else. While some drop for Columbia was nevertheless proper, was the drop to 18th justified? Or was US News making an example out of Columbia?

Finally, in June 2023, Columbia withdrew from US News’ rankings, implying that the US News ranking was reductive, flawed, and distortive. After Columbia’s deeply embarrassing rankings scandal, it’s perhaps not surprising that Columbia would leave the party loudly and in protest. But the more interesting question is, if Columbia felt this way about US News’ ranking, why did it stay at the party so long to begin with? Why did it keep lying to muscle its way into the front of the party? And now that Columbia is gone, why are others refusing to leave the party? What explains all these contradictory facts?

One theory, the charitable theory, is that the elite college ecosystem is just naturally full of uncoordinated institutions, where each institution pursuing its own interpretation of society’s best interests somehow leads to dysfunction in the aggregate. Per this theory, US News tries its best to create a good ranking but falls short because it is impossible to create truly objective ranking. Elite colleges are constantly looking to expand access, as evidenced by their commitment to affirmative action, but they are held back by constraints of resources, now the courts, regulation, or efficiency which are all outside their control. Per this theory, the cost of elite higher education rises because of Baumol’s cost disease. And per this theory, Columbia and other elite colleges don’t purposely lie to US News. Instead, elite colleges get mixed up in vague definitions that lead to understandable mistakes in their submissions.

But the charitable theory is sometimes hard to swallow, in light of the facts. With each passing year, a different, more cynical theory feels increasingly plausible. Per this theory, elite colleges aren’t just independent, uncoordinated actors, but members of a commercially collusive cartel. It implies that US News is a vital hub for collusion among the elite colleges, helping elite colleges coordinate systemic scarcity of seats and raise each other’s costs. It means that elite colleges aren’t committed to access but its opposite. Per this alternative, the cost of education rises because of market structure, not natural economic laws; and it suggests that if elite colleges are merely doing what’s in their best interests, it’s in the context of a rigged system they designed and uphold. Such a cynical theory is inherently speculative, but is there an obvious reason to reject the elite college cartel theory outright?

One obvious reason for objection might be that elite colleges are often in conflict with US News, not in cahoots. To take just one example, Columbia certainly wasn’t doing US News any favors, and US News may have retaliated against Columbia. So, how could US News be a hub for collusion, when it is clearly antagonistic to those that it ranks?

Lessons from The Toy Cartel

A few decades ago, Toys “R” Us was the dominant toy retailer in America. But Toys “R” Us’ future dominance wasn’t assured. The retail toy market was rapidly changing. Disruptive entrants had created a new form of retail experience, the warehouse club. By 1992, warehouse club chains like Costco, Sam’s Club, Pace, Price Club, and BJ’s were expanding quickly.

The secret to the warehouse clubs’ success was that they were able to offer far cheaper prices because they slashed all sorts of operating costs. Club stores opened in places where real estate was cheaper, operated with less staff, and decorated themselves in a spartan way. As the President of Costco testified in the 1990s, “almost invariably our presence in the community is going to have a tendency to drive prices down.”

For Toys “R” Us, there was reason to be nervous. In the early 90s, Toys “R” Us’ average margin on toys was above thirty percent. Costco’s margin on toys was nine percent. When Toys “R” Us’ chairman was asked whether the warehouse clubs could hurt his business, he responded, “Sure they could hurt us. Yeah.” When asked, “How so?,” he sharply replied, “By selling that product for a price that we couldn’t afford to sell it at. Simple economics.”

Competition was coming, but in the early 1990s, Toys “R” Us was still the toy manufacturers’ largest and most important customer, often buying 30 percent or more of the output of Hasbro, Mattel, and others. So, to prevent warehouse clubs from catching up, Toys “R” Us organized a cartel conspiracy with the toy manufacturers. Toys “R” Us offered the toy manufacturers a stronger relationship with itself, but only if they sold inferior products to the warehouse clubs like Costco.

The conspiracy worked. As the FTC concluded, “By the end of 1993, all of the big, traditional toy companies were selling to the clubs only on discriminatory terms that did not apply to any other class of retailers.” When the toy manufacturers sold inferior toys to warehouse clubs, fewer consumers bought their toys there. For example, Mattel’s sales to warehouse clubs declined from over $23 million in 1991 to under $8 million in 1993. But it wasn’t pure sacrifice for the toy manufacturers. After all, the toy manufacturers were benefiting from Toys “R” Us’ big purchase orders even as Toys “R” Us was benefiting from suppressing warehouse clubs’ emergence as a threat in the retail toy market.

Still, it wasn’t an easy cartel to operate. Some of the toy manufacturers wanted it all. They wanted to have a strong relationship with Toys “R” Us and they wanted to secretly increase their sales to the warehouse clubs too. As Toys “R” Us’ then-President Roger Goddu testified, “I would get phone calls all the time from Mattel saying Hasbro has this in the clubs or Fisher Price has that in the clubs…. So that occurred all the time.” Importantly, if one toy manufacturer cheated, the other manufacturers that stayed true lost out on market share. A cartel couldn’t run like that.

In response, Toys “R” Us had to punish the cheating toy manufacturer for defecting from this toy cartel. Toys “R” Us would withhold its own orders from that cheating firm until it got back in line by pulling out of the warehouse clubs. Punishment from Toys “R” Us was key to making the whole system work. Indeed, the toy manufacturers acknowledged as much, often explaining to Toys “R” Us executives that they wouldn’t be a part of the toy cartel unless their competitors were too.

The structure of the toy cartel was a variation on a traditional horizontal cartel. Instead of competitors colluding among themselves, a third-party ring leader helped them coordinate. Such a cartel has many names. Sometimes, it is called “hub-and-spoke.” Other times it is known as “rim-and-wheel.” I prefer “head-and-tentacles.” Whatever one calls it, it’s often illegal; and, Toys “R” Us and the toy manufacturers found that out in both Administrative and Appellate Court after the FTC sued them for antitrust violations in 1996.

Why Rankings Matter

Returning to the elite college market, one major question implicit in the elite college cartel theory is whether the obvious tension between US News and the elite colleges it ranks is consistent with a cartel theory. As the toy cartel demonstrates, however, antagonisms are often a natural part of cartels, far from being inconsistent with, some antagonism may be evidence of a cartel. Ultimately, wasn’t US News’ demotion of Columbia all the way down to 18th, after Columbia got caught cheating, eerily reminiscent of the punishment Toys “R” Us used to dole out to promote cartel compliance?

A different reason to scoff at the elite college cartel theory is that the mechanics of US News’ not-so-rigorous ranking surely couldn’t coordinate the policies of universities, each with billions of dollars, sometimes tens of billions of dollars, in their endowments. How could the satellite dictate the movements of the planet?

One reason may be that rankings are an odd market. Credit rating agencies are often much smaller than the companies, states, or nations that they rate. Yet credit ratings often have huge effects on the valuations of those larger entities. For the unfamiliar, US News publishes the “definitive” college ranking. While other publications also publish rankings, US News has near monopoly market share, measured by views, in the college rankings market. Within the first few days of its annual releases, US News’ college ranking routinely captures tens of millions of views from anxious students and parents. One study finds that being on US News’ top 25 list can lead a school’s applications to go up between six and ten percent. A 2013 Harvard Business School study found that “a one-rank improvement leads to a 1-percentage-point increase in the number of applications to that college.” Empirically, when Cornell rocketed in US News’ rankings from fourteenth in the fall of 1997 to sixth in the fall of 1998, applications to Cornell rose by over ten percentage points the following cycle. To the extent that competition among elite colleges exists, Stanford Sociologist Mitchell Stevens describes US News’ rankings as “the machinery that organizes and governs this competition.”

One reason rankings are so influential is that choosing a college is a complicated purchase. Young prospective students just don’t have the ability to forecast differences between four-year experiences with very little information about colleges themselves. Therefore, students and their parents often rely on proxy information, and the US News’ rankings are deeply influential in the admissions process. Plainly, a high US News ranking is a critical input that a college needs to compete in the elite college market. Therefore, because US News is a necessary upstream supplier for elite colleges, it is perfectly positioned to play the hub, consciously or unconsciously. Still, just because students rely on rankings doesn’t explain why students rely on US News’ ranking uniquely. How did US News become so dominant, and why can’t it be replaced?

US News’ path to dominance was paved by elite colleges. The incumbent elite universities of the 1980s implicitly agreed to lend US News an air of credibility, by filling out annual surveys, something that made US News popular with students. In parallel, US News’ helped the incumbent elite universities extend their incumbency into the future by creating a ranking that rated them highly not for their educational quality, but instead for their wealth and exclusivity. It’s unclear how conscious or unconscious this partnership between US News and elite colleges was. Maybe it was totally unconscious, with both sides merely pursuing their dominant business strategy.

Regardless of the mental state, the descriptive truth is that this basic relationship between elite colleges and US News is still operative today. Harvard helps US News dominate the college rankings market in the present, and US News helps Harvard extend its dominance in the elite college market in the future. Bob Morse, one of the architects of US News’ rankings, admitted as much in an interview in 2009 saying, “When the public sees that the schools are wanting to do better in our rankings, they say, well if the schools want to improve in these rankings, they must be worth looking at. So, in essence, the colleges themselves have been a key factor in giving us the credibility.” Credibility is the most important factor for a ranking to be successful. Students and parents can’t independently adjudicate the quality of a ranking for the same reason that they can’t independently adjudicate the quality of a college: it’s complicated and subjective. Therefore, the ranking with the most credibility wins out with students and parents. And a path of least resistance to such credibility was to get the incumbent elites to qualify US News as worthwhile.

US News likely knows that it can’t afford to lose the support of the incumbent elite schools; without it, US News couldn’t offer a credible ranking. US News likely knows that it cannot afford the perception of a boycott from those incumbent elite colleges. This may be why US News publishes a ranking that weights selectivity at seven percent, financial-resources-per-students at ten percent, class-size at eight percent, student-faculty-ratio at one percent, and colleges ranking each other at twenty percent. The US News ranking criteria has a very simple logic. As Washington Monthly magazine observed in 2000, “the perfect school is rich, hard to get into, harder to flunk out of, and has an impressive name.”

There may well be evidence of hyper-elite colleges lobbying US News for changes to this or that criteria to better serve their needs. Yet even in the absence of such an explicit conspiracy, US News uses a criteria that self-justifies why incumbents are already on top of the prestige ladder. Presumably, both US News and the elite colleges know this. But the circular logic of US News’ rankings doesn’t just keep the elite colleges on top. It also incentivizes them to become more extreme versions of themselves.

US News incentivizes colleges to pull in more applications so they can reject them. US News incentivizes colleges to stagnate enrollment growth. US News incentivizes colleges to raise prices further and spend more money per student. Worse, US News incentivizes less-elite colleges to adopt all the worst parts of the elite colleges, such as out-of-control spending.

Plainly, incentivizing colleges to spend more money to compete in the elite market raises barriers to entry by shifting supply curves up for each participant. Plus, incentivizing colleges to be unduly rejective to attract students forces colleges to undersupply more than they otherwise would. In sum, US News’ rankings incentivize intense market dysfunctions like scarcity on the supply side.

Per the elite college cartel theory, the role of Toys “R” Us is played by US News. US News allegedly coordinates collusion among all the different elite colleges. But the way US News allegedly coordinates its spokes is subtle and ingenious, as it facilitates seat scarcity coordination through its ranking formula instead of explicit communication. In this narrative, US News became dominant precisely because it chose to play the coordinating role that elite colleges may have wanted, and it played that role just as elite colleges may have wanted it to.

There are facts that support an inference of collusion. For one, links between US News and hyper-elite colleges are deep. In the 2000s and 2010s, Mortimer Zuckerman, the owner of US News, became a mega-donor to Ivy League colleges like Harvard and Columbia. He served on the Board of Trustees at Princeton. In that same period, US News’ monopoly consolidated. The hyper-elite colleges continued to support the regime. They didn’t boycott the rankings. They embraced them, continuing to give US News exclusive answers to surveys that no other ranking receives. When President Obama’s administration sought to roll out a public competitor to US News’ college rankings in 2013, elite college administrators rallied to kill the ranking effort. Instead, the public got a limp scorecard, and US News didn’t face a public, credible competitor.

For another, elite colleges have horizontal links among themselves. For instance, there is large surface area for coordination in things such as lobbying for government policies, joint research, patent commercialization, and admissions. Moreover, elite colleges often have interlocking governance boards. Jurisprudentially, these types of interlocking links have supported inferences of conspiracy in many antitrust cases.

Empirically, elite colleges have been pulled into court for allegedly collusive cartel behavior before. The Ivy League colleges were sued by the Department of Justice for fixing prices on financial aid in the 1990s. In 2022, a group of seventeen elite colleges was sued for price-fixing by a class of students on financial aid. The NCAA has been sued many times for cartel tactics that limit compensation for student-athletes. So, might seat scarcity, and exclusion of competitors, be another area where elite colleges collude?

Lastly, another factor supporting an inference of conspiracy are the market dynamics themselves. The demand for seats at elite institutions has proven to be remarkably inelastic. If the Varsity Blues scandal proves anything, it’s that people will go through a lot of trouble to capture a seat at an elite school. Importantly, inelastic demand, in other markets, has attracted cartel formation. For example, OPEC operates in the inelastic oil market. Big tobacco companies operate in the inelastic cigarette market. In those markets, cutting output by one percent has often raised prices by more than one percent, making scarcity a profitable strategy.

In some markets with inelastic demand, a cartel isn’t needed to produce scarcity because only one or two companies control the entire market anyway. But the elite college market isn’t like that. Many different elite colleges exist. Without some machinery to coordinate scarcity, it likely would not be possible to produce systemic scarcity.

In a system structured as ours, explicitly or accidentally, Penn’s acceptance rate necessarily drops from 47 percent in 1991 to less than 6 percent in 2023. As authors Carnevale, Schmidt, and Strohl quantify, in their book, The Merit Myth, “There are 1.5 million high school seniors with better than an 80 percent chance of graduating from one of the top 193 colleges, but those colleges annually admit only 250,000 freshmen.” As economists Kent and Smetters quantified in 2021, if elite colleges ignored relative prestige and simply maintained student quality, since 1990 their total enrollments would have doubled or tripled. Instead, Harvard, Princeton, Yale, and Stanford only increased enrollment by seven percent between 1990 and 2015.

Let’s be clear: The artificial scarcity in slots, made possible by the ranking system, allows elite colleges to under-produce relative to a world in which such coordination was not possible; and by under-producing, the elite colleges are able to impose supra-competitive prices for admission.

You can see the market failure all around you. Tuition prices keep rising well beyond the average inflation rate. Scarcity-induced admissions scandals like Varsity Blues continue to pop up. But perhaps the most obvious sign is that the demographics at formerly less exclusive colleges have also gone wacky. The rankings are warping the whole market into copycatting the worst parts of the hyper-elite colleges. Safety schools have morphed into reach schools. Reach schools have slipped out of sight. Seats at American universities have turned needlessly scarce, and the privileged few have largely outcompeted the aspiring many for those seats.

Indeed, elite colleges might object to the entire conjecture of this article. They might say that there is no fusion between themselves and US News. They might claim that they are increasingly diverging from US News’ rankings. They might point to their boycott of the US News’ law school rankings. Harvard might point out that it pulled out of US News’ medical school rankings.

Yet it’s not clear if these objections comprehensively rule out a cartel explanation. Even if elite colleges are pulling out of US News’ rankings at the graduate levels, they refuse to do so at the undergraduate level. There is absolutely no evidence that a boycott is forthcoming for the undergraduate rankings. Instead, we see only continuing participation. Importantly, undergraduate rankings matter far more than law school or medical school rankings. They matter more because an elite college’s undergraduate reputation is also often used as a proxy for its graduate programs.

Pitiful Growth in Seats

Skeptics might also assert that elite colleges have always been exclusive, independently of US News. Elite colleges might argue that the whole reason that they’re elite is because they’re exclusive. This argument is more persuasive on first glance than on close examination. While it’s true that elite colleges must reject some students to maintain class quality, the question is one of degree.

How exclusive does an elite college need to be? Do we need Ivy League colleges to reject 95 percent of applicants? Or will rejecting 80 percent, as they did in the 1980s, suffice? It is a false argument to assert that growth and quality are necessarily opposed. For example, before the rankings-era, Stanford increased its enrollment by over 250 percent from 1920 to 1970. It managed to stay very elite in that period of time.

Nor is undue rejection necessary to maintain academic quality. A common quip on Harvard’s campus is that the hardest thing about Harvard is getting in. There are many students of diligent character and great intellect who are routinely rejected by the elite colleges, and those rejections have nothing to do with quality. Instead, those rejections may be the collateral damage that a hub-and-spoke cartel produces. Absent this concern for relative prestige, driven home by the rankings, the elite colleges would naturally admit more students.

Elite colleges might alternatively object that acceptance rates are a poor measure for increasing exclusion. They might argue that each student applies to far more schools than she once did. This is true. But the reason each student applies to more schools today is because she is dramatically more likely to get rejected at each one. If you leave behind acceptance rates, and merely look at raw numbers, the growth in seats at elite colleges has been pitiful. As Economists Kent and Smetters explained in 2021, “While college enrollment has more-than doubled since 1970, elite colleges have barely increased supply, instead reducing admit rates.” For example, in the 2005–06 school year, Yale enrolled 1,321 undergrads, and in 2016–17, Yale enrolled a whopping 1,367 students.

A market fundamentalist might argue that the scarcity produced by elite colleges is opening space for formerly less elite colleges like Tulane and BU to fill the new market need by becoming more exclusive themselves. Fundamentalists might argue that the market is responding as it should, by creating more supply to meet the growing demand of qualified students eager for prestigious degrees. But, of course, such fundamentalists miss the crucial point.

At what cost is Tulane filling in for Penn? The rankings that US News has set up requires everyone to get more expensive. So, as more students were rejected by Penn, Tulane experienced an increase in demand for its slots, which justified higher prices. Even then it’s not a real substitute. As economists Blair and Smetters quantified in 2021, the consumer welfare loss of being rejected from Harvard, Yale, Stanford, or Princeton is estimated to be around 140 percent of the mean total tuition, an amount in the order of hundreds of thousands of dollars. This is despite the rise of the so-called substitutes.

In the end, whether the elite colleges have explicitly colluded to produce dysfunction or whether it is some freak accident is probably the least interesting thing about the elite college market to the vast majority of Americans. For the average student coming of age, it doesn’t matter if the elite college market is dysfunctional because of an explicit conspiracy or because of an unfortunate accident of market development. What matters to the applicant is that she may not be accepted to the college of her dreams because rankings incentivize each elite college to slow growth in enrollments. With each new college scandal, a simple fact becomes more and more clear. We need a serious conversation about how to restructure this market.

Sahaj Sharda is a student at Columbia Law School and author of the book The College Cartel.

Over the past two years, heterodox economic theory has burst into the public eye more than ever as conventional macroeconomic models have failed to explain the economy we’ve been living in since 2020. In particular, theories around consolidation and corporate power as factors in macroeconomic trends–from neo-Brandeisian antitrust policy to theories of profit seeking as a driver of inflation–have exploded onto the scene. While “heterodox economics” isn’t really a singular thing–it’s more a banner term for anything that breaks from the well established schools of thought–the ideas it represents challenge decades of consensus within macro- and financial economics. This development, of course, has left the proponents of the traditional models rather perturbed.

One of the heterodox ideas that has seen the most media attention is the idea of sellers’ inflation: the theory that inflation can, at least partially, be a result of companies using economic shocks as smokescreens to exercise their market power and raise the prices they charge. The name most associated with this theory is Isabella Weber, a professor of economics at the University of Massachusetts, but there are certainly other economists who support this theory (and many more who support elements of it but are holding out for more empirical evidence before jumping into the rather fraught public debate.)

Conventional economists have been bristling about sellers’ inflation being presented as an alternative to the more staid explanation of a wage-price spiral (we’ll come back to that), but in recent months there have been extremely aggressive (and often condescending, self-important, and factually incorrect) attacks on the idea and its proponents. Despite this, sellers’ inflation really is not that far from a lot of long standing economic theory, and the idea is grounded in key assumptions about firm behavior that are deeply held across most economic models.

My goal here is threefold: first, to explain what the sellers’ inflation and conventional models actually are; second, to break down the most common lines of attack against sellers’ inflation; third, to demonstrate that, whatever its shortcomings, sellers’ inflation is better supported than the traditional wage-price spiral. Many even seem to recognize this, shifting to an explanation of corporations just reacting to increased demand. As we’ll see, that explanation is even weaker.

What Is Sellers’ Inflation?

The Basic Story

As briefly mentioned above, sellers’ inflation is the idea that, in significantly concentrated sectors of the economy, coordinated price hikes can be a significant driver of inflation. While the concept’s opponents generally prefer to call it “greedflation,” largely as a way of making it seem less intellectually serious, the experts actually advancing the theory never use that term for a very simple reason: it doesn’t really have anything to do with variance in how greedy corporations are. It does rely on corporations being “greedy,” but so do all mainstream economic theories of corporate behavior. Economic models around firm behavior practically always assume companies to be profit maximizing, conduct which can easily be described as greedy. As we’ll see, this is just one of many points in which sellers’ inflation is actually very much aligned with prevailing economic theory.

Under the sellers’ inflation model, inflation begins with a series of shocks to the macroeconomy: a global pandemic causes an economic crash. Governments respond with massive fiscal stimulus, but the economy experiences huge supply chain disruptions that are further worsened with the Russian invasion of Ukraine. All of these events caused inflation to increase either by decreasing supply or increasing demand. The stimulus checks increased demand by boosting consumers’ spending power–exactly what it was supposed to do. Both strained supply chains and the sanctions cutting Russia off from global trade restricted supply. Contrary to what some opponents of sellers’ inflation will say, the theory does not deny the stimulus being inflationary (though some individual proponents might). Rather, sellers’ inflation is an explanation for the sustained inflation we saw over the past two years. Those shocks led to a mismatch between demand and supply for consumer goods, but something kept inflation high even after the effects of those shocks should have waned.

The culprit is corporate power. With such a whirlwind of economic shocks, consumers are less able to tell when prices are rising to offset increases in the cost of production versus when prices are being raised purely to boost profit. This, too, is not at odds with conventional macro wisdom. Every basic model of supply and demand tells us that when supply dwindles and demand soars, the price level will rise. Sellers’ inflation is an explanation of how and why prices rise and why prices will increase more in an economy with fewer firms and less competition.

Sellers’ inflation is really just a specific application of the theory of rent-seeking, which has been largely accepted since it was introduced by David Ricardo, a contemporary of the father of modern economics, Adam Smith. (Indeed, this point, which I raised nearly a year and a half ago in Common Dreams, was recently explored in a new paper from scholars at the University of London.) As anyone who has ever watched a crime show could tell you, when you want to solve a whodunnit, you need to look at motive, means, and opportunity. The greed (which, again, is at the same level it always is) is the motive. Corporations will always seek to charge as high of a price as they can without being dangerously undercut by competitors. Sellers’ inflation doesn’t posit a massive increase in corporate greed, but a unique economic environment that allows firms to act upon the greed they have possessed.

Concentration is the means; when the market is in the hands of only one or a few firms, it becomes easier to raise prices for a couple of reasons. First, large firms have price-setting power, meaning they control enough of the sector that they are able to at least partially set the going rate for what they sell. Second, when there’s only a few firms in a sector, wink-wink-nudge-nudge pricing coordination is much easier. Just throw in some vague but loaded phrases in press releases or earnings calls that you know your competition will read and see if they take the same tack. For simplicity, imagine an industry dominated by two firms, A and B. At any given point, both are choosing between holding prices steady and raising them (assume lowering prices is off the table because it’s unprofitable, let’s keep it simple.) This sets up the classic game-theoretical model of the prisoner’s dilemma:

| A Maintains Price | A Raises Price | |

| B Maintains Price | →, → | ↓, ↑ |

| B Raises Price | ↑, ↓ | ↑, ↑ |

In the chart above, the red arrows represent the change in A’s profit and the blue represent the change in B’s. If both hold the price steady, nothing changes, we’re at an equilibrium. If one and only one firm raises prices without the other, the price-hiker will lose money as price-conscious consumers switch to their competitor, who will now see higher profits. This makes the companies averse to raising prices on their own. But, if both raise their prices, both will be able to increase their profits. That’s why collusion happens. But, wait, isn’t that illegal? Yes, yes it is. But it is nigh on impossible to police implicit collusion, especially when there is a seemingly plausible alternative explanation for price hikes.

As James Galbraith wrote, in stable periods, firms prefer the safer equilibrium of holding prices relatively stable. As he explains:

In normal times, margins generally remain stable, because businesses value good customer relations and a predictable ratio of price to cost. But in disturbed and disrupted moments, increased margins are a hedge against cost uncertainties, and there develops a general climate of “get what you can, while you can.” The result is a dynamic of rising prices, rising costs, rising prices again — with wages always lagging behind.

And that gets us to opportunity, which is what the macroeconomic shocks provide. Firms probably did experience real increases in their production costs, which gives them good reason to raise their prices…to a point. But what has been documented by Groundwork Collaborative and separately by Isabella Weber and Evan Wasner is corporate executives openly discussing increasing returns using “pricing power,” which is code for charging more than is needed to offset their costs. This is them signaling that they see an opportunity to get to that second equilibrium in the chart above, where everyone makes more money. And since that same information and rationale is likely to be present at all of the firms in an industry, they all have the incentive (or greed if you prefer) to do the same. This is easiest to conceptualize in a sector with two firms, but it holds for one with more that is still concentrated. At some point, though, you reach a critical mass where suddenly there’s one or more firms who won’t go along with it. As the number of firms increases, it becomes more and more probable that one won’t just go along with it, which is why concentration facilitates coordination.

And that’s it. In an economy with significant levels of concentration — more than 75 percent industries in the American economy have become more concentrated since the 1990s — and the smokescreen of existing inflation, corporate pricing strategy can sustain rising prices due to the uncertainty. Now, if you ask twenty different supporters of sellers’ inflation, you’ll likely get twenty slightly different versions of the story. However, the main beats are mostly agreed upon: 1) firms are profit maximizing, 2) they always want to raise prices but usually won’t out of fear of either being undercut by the competition or being busted for illegal collusion, and 3) other inflationary pressures provide some level of plausible deniability which lowers the potential downside of price increases.

What Evidence Is There?

The evidence available to support theories of sellers’ inflation is one of the main points of contention between its proponents and detractors. Despite that, there is strong theoretical and empirical evidence that backs the theory up.

First is a basic issue of accounting that nobody in the traditional macro camp seems to have a good answer for. Profits are always equal to the difference between revenues (all the money a company brings in) and costs (all the money a company sends out).

Profits= Revenue – Costs

This is inviolable; that is simply the definition of profits. As I’ve written before, this means that the only two possible ways for a company to increase profits is by generating more revenue or cutting costs (or a combination of the two, but let’s keep it simple). Costs can’t be the primary driver in our case because we know they’re increasing, not decreasing. Inflationary pressures should still have increased production costs like labor and any kind of input that is imported. Companies also have been adamant about the fact that they are facing rising costs; that’s their whole justification for price hikes. And mainstream economists would agree. They blame lingering inflation on a wage price spiral, which says that workers demanding higher wages have driven cost increases that force companies to raise prices – resulting in higher inflation. As both sides agree that input costs are rising, the only possible explanation for increased profits is an increase in revenue. Revenue also has itself a handy little formula:

Revenue = Price * Units Sold

While the units sold may have increased, price was the bigger factor. We know this for at least two key reasons: because of evidence showing that output (the units sold) actually decreased and because of the evidence from earnings calls compiled by Groundwork. Executives said their strategy was to raise prices, not to sell more products. And there’s two very good reasons to believe the execs: (1) they know their firms better than anyone, and (2) they are legally required to tell the truth on those calls. (That second reason is also evidence of sellers’ inflation on its own; if the theory’s opponents don’t buy the explanation given by the executives to investors, they must think executives are committing securities fraud.)

In rebuttal to the accounting issue, Brian Albrech, chief economist at the International Center for Law and Economics, has argued that using accounting identities is wrongheaded:

Just as we never reason from a price change, we need to never reason from an accounting identity. My income equals my savings plus my consumption: I = S + C. But we would never say that if I spend more money, that will cause my income will rise.

This, on face, seems like a reasonable argument, except all it really shows is that Albrecht doesn’t understand basic math. Tracking just one part of the equation won’t automatically tell us what the others do…duh. But we can track what a variable is doing empirically and use that relationship to make sense of it. We would never say that someone spending more money on consumption causes their income to rise. But we certainly could say that if we observe an increase in personal consumption, then we can reason that either their income increased or their savings decreased. The mathematical definition holds, you just have to actually consider all of the variables. In fact, Albrecht agrees, but warns “Yes, the accounting identity must hold, and we need to keep track of that, but it tells us nothing about causation.” No, it tells us correlation. Which, by the way, is what econometrics and quantitative analyses tell us about as well.

The way you get to causation in economics is by tying theory and context to empirical correlations to explain those relationships. Albrecht’s case is just a very reductive view of the actual logic at play. He continues:

After all, any revenue PQ = Costs + Profits. So P = Costs/Q + Profits/Q. If inflation means that P goes up, it must be “caused” by costs or profits.

No, again. Stop it. This is like saying consumption causes income.

Once again, Albrecht is wrong here. This is like saying higher consumption will correspond to either higher income or lower savings. Additionally, there’s a key difference between the accounting identities for income and for profits: income is broken down into consumption and savings after you receive it, whereas costs and revenues must exist before profits. This makes causal inference in the latter much more reasonable; income is determined exogenously to that formula, but profits are endogenous to their accounting identity.

In addition to these observations, though, there is also various economic research that supports the idea of seller’s inflation. Some of the best empirical evidence comes from this report from the Federal Reserve Bank of Boston, this one from the Federal Reserve Bank of San Francisco, and this one from the International Monetary Fund.

Another key piece of evidence is a Bloomberg investigation that found that the biggest price increases came from the largest firms. If market power were not a factor, then prices should have been rising roughly proportionally across firms, regardless of their size. If anything, large firms’ economies of scale should have cut down on the need to hike prices. Especially because basic economic theory tells us that when demand increases, companies want to expand supply, which should have resulted in more products (especially from larger firms with more resources) and a corresponding drop in price increases. And yet, what we actually saw was a drop in production from major companies like Pepsi, who opted instead to increase profits by maintaining a shortfall in supply.

That said there’s plenty more, including this from the Kansas City Fed, this from Jacob Linger et al., this from French economists Malte Thie and Axelle Arquié, this from the European Central Bank, this one from the Roosevelt Institute, and more. The Bank of Canada has also endorsed the view. It seems unlikely that the Federal Reserve, European Central Bank and the Bank of Canada have all become bastions of activist economists unmoored from evidence. Perhaps it’s time those denying sellers’ inflation are labeled the ideologues.

The Case Against Sellers Inflation

A Few Notes on Semantics

Before we get into the substance of critiques against sellers’ inflation as a theory, there are a few miscellaneous issues with the framing its opponents often use. There is a tendency for arguments against sellers’ inflation to use loaded words or skewed phrasing to implicitly undermine the legitimacy of people who are spearheading the push for greater scrutiny of corporations as a part of managing inflation.

For instance, Eric Levitz says the debate sees “many mainstream economists against

heterodox progressives.” This phrasing suggests that the debate is between economists on the one hand and proponents of sellers’ inflation on the other. But that’s not true! There are both economists and non-economists on both sides of the issue. Weber is an economist, as are the researchers at the Boston and San Francisco Feds. And others, including James Galbraith, Paul Donovan, Hal Singer, and Groundwork’s Chris Becker and Rakeen Mabud are on board. Notably, Lael Brainard, the head of President Biden’s Council on Economic Advisors (and former Federal Reserve Vice Chair) recently endorsed the view.

Or take how Kevin Bryan, a professor of management at the University of Toronto described Isabella Weber as a “young researcher” who “has literally 0 pubs on inflation.” Weber is old enough to have two PhDs and tenure at UMass and–will you look at that–has written about inflation before! Presenting her as young sets the stage for making her seem inexperienced, which saying she has no publications doubles down on. But his claims are false. Weber wrote a paper with Evan Wasner specifically about sellers’ inflation. But even if we take Bryan’s point as true and ignore the very real work Weber has done on inflation and pricing, Weber still has significant experience with political economy, which helps to explain how institutional power is able to influence markets—exactly the type of thinking sellers’ inflation is based upon.

(And this is nothing compared to the abuse that Weber endured after an op-ed in The Guardian provoked a frenzy of insulting, condescending attacks from many professional economists. For more on that, see Zach Carter’s New Yorker profile of Weber and/or this Twitter thread that documents Noah Smith’s outlash at Weber.)

But even the semantics that don’t get into ad hominem territory are confusing. Here is a list of the topline concerns that Kevin Bryan raised:

Let’s just run through that list of concerns real quick:

- What does very online even mean? Sellers’ inflation has been embraced as at least a plausible concept by the President of the United States, the European Central Bank, at least two Federal Reserve Banks, and the International Monetary Fund. If that’s not enough legitimization it’s hard to know what would be. This concern makes it sound like the proponents are random reddit users, rather than the serious academics and policy makers they are.

- I don’t know why the presence of “virulent defenders” undermines the idea itself. Defenders of traditional economics are virulent as well; Larry Summers called the idea of relating antitrust policy to inflation “science denial.”

- Traditional monetary policy is often (but not always) associated with centrist, pro-business politics. Also, conventional Industrial Organization theory and even Borkian consumer welfare theories recognize a relationship between price and the structure of firms and markets, so the fundamental ideas are certainly not leftist.

- That proponents of sellers’ inflation refer to gatekeepers shooting down these theories seems disingenuous. Everyone who supports sellers’ inflation would probably rather be discussing it because of its merits. But when people like Bryan or Larry Summers refuse to even consider the idea as potentially legitimate, the only option left is to discuss it because of the iconoclasm. If there isn’t a story about changing academic opinions, then the story about challenges to conventional wisdom being shut out by the old guard will have to do.

All of this is to set up the next point in that Twitter thread, which is that “being an Iconoclast is not the same thing as being rigorous, or being right.” True, but dodging the debate by attacking the credibility of an idea’s advocates and taking issue with the method of dissemination are also not the same as being rigorous. Or as being right.

These are just a couple of examples, but opponents of this theory really lean into making it sound like its champions are inexperienced and don’t know what they’re talking about. Aside from being in bad faith, this also indicates a lack of confidence in comparing the contemporary story to that of sellers’ inflation.

The Theoretical Substance of the Opposition

With the semantics out of the way, it’s time to get into the meat of the case(s) against sellers’ inflation. There is no singular, unified case here, more of a constellation of related ideas.

The first line of defense against theories of sellers’ inflation is asserting that traditional macroeconomics is good and has solved our inflation problem. For example, Chris Conlon of NYU has credited rate hikes with inflation cooling. Conlon says “I for one am glad Powell and Biden admin followed boring US textbook ideas.” But there’s a problem with that: the contemporary economic story does not actually explain how rate hikes can cool inflation without a corresponding rise in unemployment.

The traditional story starts in the same place as the sellers’ inflation story: macroeconomic shocks create inflation. (Although the traditionalists prefer to emphasize fiscal stimulus as the primary shock, rather than supply chains. The evidence largely indicates that stimulus did have some inflationary effect, but not much. The global nature of inflation also undercuts the idea that American domestic fiscal policy could be the main explanation.) The shock(s) create a supply and demand mismatch, with too much money chasing too few available goods. After that, however, the traditional mechanism for explaining inflation remaining high is supposed to be a wage-price spiral.

The story goes something like this: the stimulus boosted consumer demand, which overheated the economy, and created more jobs than could be filled, meaning job seekers negotiated higher pay when they took positions. They then spent that extra money which increased demand further, leading to even higher prices as supply couldn’t keep up with demand. Workers saw that their cost of living went up, so they took the opportunity to demand better pay. Companies were forced to give in because they knew in a hot labor market, their workers could leave and earn more elsewhere if employers didn’t meet workers’ demands. Once their wages went up, those workers had more spending power, which they used to buy more things, further increasing demand. That elevated prices more, as the supply-demand mismatch increased. Now workers see their cost of living rising again, so they ask for another raise. If this pattern has held for a few rounds of pay negotiations, maybe workers ask for more than they otherwise would, trying to get out ahead of their spending power shrinking again. Rinse and repeat.

But we know that this story doesn’t describe the inflation that we saw over the last couple of years. Wage growth lagged behind inflation, which indicates that something else had to be driving price increases. Plus the Phillips curve, which is meant to illustrate this relationship between higher employment and higher inflation, has been broken in the US for years. It simply does not show a meaningful positive relationship any more.

It’s important that we understand this story as a whole. Levitz, in his piece, tries to separate the initial supply-demand mismatch from the wage-price spiral as a way of making the conventional model stack up better against sellers’ inflation. But that doesn’t actually hold because if you omit the wage-price spiral (which Levitz agrees seems dubious), the mainstream macro story has no mechanism for inflation staying high. If it were just a one-time stimulus, that would explain a one-time inflation spike, but once that money is all sent out (say by the end of 2021), there’s no source for further exacerbating the supply-demand mismatch (in say the end of 2022 or early 2023). (Remember, inflation is the rate of change of prices, so if prices spike and then stay the same afterwards, that plateau will reflect a higher price level but not sustained high inflation.)

Similarly, focusing on only the supply-side shocks provides no reason for why inflation remained elevated long after supply chain bottlenecks had cleared and shipping prices had fallen.

The incentive shift that occurs in concentrated markets is key to understanding this. In a competitive market, firms’ response to a surge in demand is to produce more. But, when the market is concentrated and some level of implicit coordination is possible, increased production is actually against a firm’s best interest, it will just put them back at that first equilibrium from earlier. They want to enjoy the high prices and hang out in the second equilibrium as long as they can

Sellers’ inflation, at least, has an internal mechanism that can explain how we got from one-off shocks to the economy to sustained inflation. Yet its opponents wrongly describe what that mechanism is. Remember the story from earlier: the motive of profit maximization, the means of market power in concentrated industries, and the opportunity of existing inflation. The most basic objection to this mechanism is to mischaracterize it as blaming sustained upward pressure on prices on an increase in the level of greed among corporations. That’s what economist Noah Smith did in a number of blogs that have aged quite poorly. But no one is seriously arguing companies are greedier, only that there is an innate level of greed, which conventional models also assume.

The strawmanning continues when we get to the means, which is what this Business Insider piece by Tevan Logan of Ohio State does by pointing out how Kingsford charcoal tried and failed to rent seek by raising prices, which just caused them to lose market share to retailers’ generic brands. Exactly! The competition in the charcoal market demonstrates why consolidation is a key ingredient in sellers’ inflation. If Kingsford had a product without so many generic substitutes, then consumers would not have had the chance to switch products. And that’s why a lot of the biggest price hikes occurred with goods like gas, meat, and eggs, all of which are controlled by cartel-esque oligopolies.

The opportunity component actually seems to be a point that there’s broad agreement on. For example, Conlon says that the “idea that firms might raise prices by more than their costs is neither surprising nor uncommon.” He goes on to suggest, however, that this is likely because firms expect costs to continue rising. There’s certainly an element of truth to that, but also consider the basic motivation of corporations: maximizing profits. As a result, if companies expect their costs to rise by, say, 5 percent over the next year and they’re going to adjust prices anyway, why not raise prices by 7 percent, more than enough to offset expected cost increases?

The theoretical case against sellers’ inflation is, as Eric Levitz noted, “deeply confused;” he was just wrong about which side was getting stumped.

The Empirical Case Against Sellers’ Inflation

The other side of the opposition to sellers’ inflation focuses on the empirics. To be fair, there’s certainly more work that needs to be done. But that’s about as far as the critique goes. The response is just “the data isn’t there.” I’ll refer you to Groundwork’s excellent work on executives saying that they are raising prices beyond costs, Weber’s paper, the Boston and San Francisco Fed papers, Bloomberg’s findings about larger firms charging higher prices, Linger et al.’s case study of concentration and price in rent increases, and the IMF working paper.

Setting aside the very real empirical evidence in support of seller’s inflation, the argument about a lack of empirics still gives no reason to default to the traditional model of inflation. Even if we accept a lack of data for sellers’ inflation, we have quite a lot of data that directly contradicts the mainstream story. Surely, something unproven is still preferable to something disproven.

Some economists like Olivier Blanchard have raised questions about methodology and the need for more work. Great! That’s what good discourse is all about; being skeptical of ideas is fine, as long as you don’t throw them out on gut instinct. Unfortunately, critics often simply reject the theory, rather than express skepticism. When they do, however, they often fall into the same methodological gaps in which they accuse “greedflation” proponents. For example, Chris Conlon egregiously conflating correlation and causation of the Fed’s monetary policy. Or Brian Albrecht taking issue with inductive logic while siding with a traditional story that makes up ever more convoluted, illusory concepts.

So Where Does That Leave Us?

The traditional model of inflation is broken. The Phillips curve is no longer a useful tool for understanding inflation, a wage-price spiral flies in the face of reality, and there’s no viable alternative mechanism for sustained inflation within the demand-side model. Enter sellers’ inflation.

From the same starting point, and drawing on several cornerstone pieces of economic theory, sellers’ inflation is able to provide a consistent vehicle for one-off shocks to create prolonged upward pressure on price levels as firms exercise their market power. The bedrock ideas of the theory are consistent with seminal economic thought from the likes of David Ricardo and even Adam Smith himself and has the support of a number of subject matter experts. Is it a perfect theory? No, but to paraphrase President Biden, don’t compare it to the ideal, compare it to the alternative. More empirics would be preferable, but the case for sellers’ inflation remains much stronger than the case for a fiscal stimulus igniting a wage-price spiral, which is entirely anathema to most of the evidence we do have.

One way or another, inflation is trending down and, by some measures, is closing in on the target rate again. Many have rushed to credit the Federal Reserve for following the textbook course, but they don’t have any internal story about how the Fed could have done that without increasing employment. As Nobel laureate Paul Krugman (who supported rate hikes and once bashed the theory of sellers’ inflation) asked, “Where’s the rise in economic slack?” The conventional story is missing its second chapter and yet its advocates are eager to point to an ending they can’t explain as all the justification they need to avoid reconsidering their priors. One possibility Krugman notes, which Matthew Klein explicates here, is that inflation really was transitory the whole time. The sharp upward pressures were, indeed, caused by one-off shocks from the pandemic, supply chains, and Russian aggression, but the effects had unusually long tails. This theory aligns very well with sellers’ inflation; corporate price hikes could simply be the explanation for such long lasting effects.

Additionally, as Hal Singer pointed out, the recent drop in inflation corresponds to a downturn in corporate profits. Some, including Noah Smith (in that tweet’s comments), disagree and argue that both lower profits and less inflation are caused by new slack in demand. But that doesn’t really match what we’re seeing across macroeconomic data. True, employment growth has slowed, as has the growth of personal consumption, but that still doesn’t match up with the type of deflationary pressure that we were supposed to need; Larry Summers was citing figures as high as 6 percent unemployment. Plus, the metrics that do show demand softening largely only show that employment and consumption are steadying, not decreasing. On top of that, the contraction in output that The Wall Street Journal identified makes the case for simple shifts in demand driving price levels dubious. Additionally, if a wage-price spiral were at fault, leveling off employment growth would not be enough, the labor market would still be too tight (aka inflationary), hence why we’d need to increase unemployment.

Good economic theories always need more work to apply them to new situations and produce quality empirics. But pretending that sellers’ inflation is a wacky idea while the conventional macro story maps perfectly onto the economy of the past three years is thumbing your nose at the most complete story available, significant empirical evidence, and centuries of economic theory.

Dylan Gyauch-Lewis is Senior Researcher at the Revolving Door Project.

The Federal Trade Commission’s scrutiny of Microsoft’s acquisition of game producer Activision-Blizzard did not end as planned. Judge Jacqueline Scott Corley, a Biden appointee, denied the FTC’s motion for preliminary injunction, ruling that the merger was in the public interest. At the time of this writing, the FTC has pursued an appeal of that decision to the Ninth Circuit, identifying numerous reversible legal errors that the Ninth Circuit will assess de novo.