Haters sometimes accuse the Federal Reserve of being a shadowy cabal of private bankers that slipped loose from democratic oversight. But we at The Sling trust our patriotic central bankers, who have never had anything to hide. To help the Fed tell its side of the story, we submitted a Freedom of Information Act (FOIA) request to retrieve recent meeting minutes.

Readers may be surprised to learn that although the Fed has acquired a great deal of independent authority, in some circumstances it must consult with other financial regulators, including the Federal Deposit Insurance Corporation (FDIC). The FDIC’s five-member board includes the FDIC Chair, the Comptroller of the Currency, two members of the minority party, and, much to the Fed’s chagrin, the Director of the Consumer Financial Protection Bureau (CFPB)—an agency created in the wake of the Great Financial Crisis to protect consumers from financial scams and frauds. The CFPB is housed within and funded by the Fed, yet sometimes in its short history it has been led by a director who violates Fed norms by having different values and expressing different opinions than the Fed Chair.

The below meeting minute excerpts shine light on the internal operations of the Fed and its valiant efforts to rein in consensus-destroyer Rohit Chopra, the outgoing director of the CFPB.

Minutes of the Board of Governors of the Federal Reserve System

At its meeting yesterday, the Board discussed how the market-implied path for the federal funds rate forecasted certain headwinds to central bank hegemony (aka “bankocracy”). In particular, over the intermeeting period, options on interest rate futures indicated that market participants were increasingly exasperated with Rohit Chopra.

Such developments reflected elevated concerns among investors that Chopra would not only continue to penalize a broad range of business innovation by returning billions of dollars to swindled consumers, but would also decline to rubber-stamp the Fed’s Basel III endgame proposal to allow banks to hold only a single-digit percentage of capital as a cushion against potential losses. Congress had directed the Fed to impose these reserve requirements shortly after the Great Financial Crisis. That the process is still in the proposal stage over a decade later confirms what the Fed tells every interviewer: its biggest fault is being a perfectionist. The Fed is strongly committed to crafting every clause just right, and sometimes unweaves an entire tapestry at night to punish itself for typos and ward off inappropriate suitors. In any event, the Fed recently retained a new associate therapist; a development that warrants greater investor confidence in a declining VIX and short-term higher yields on its regulatory efforts. Members also concurred that although the Fed sets the price of money, it cannot reasonably be characterized as a “price control agency” because reasons.

Market-based measures of exasperation were further articulated by one Board member who explained that Chopra’s un-collegial actions never would have been tolerated by past chairs: “Paul [Volcker] would have been shocked.” The Board then reviewed other deviations from consensus, such as Chopra’s decision to jeopardize national security by stopping financial institutions from stockpiling strategic junk fee reserves—a policy in marked tension with his professed goal of increasing capital reserves.

A second Board member remarked upon Chopra’s stellar credentials and their alignment with the Fed milieu: Harvard undergrad, Wharton MBA, and close relationships with “financiers, convicted felons, and everything in between.” The member likewise approvingly noted that so far, Chopra has not publicly questioned Supreme Court dicta retconning the existence of the Fed as Constitutionally sound based on the rigorous principle of being a “special arrangement sanctioned by history.” The member further recognized and commended Chopra’s benefits orientation sessions, which helped Board colleagues and staff sign up for the best available health and life insurance options, making Open Enrollment much less stressful. Perhaps as a gesture of good faith, Chopra could also set up a dollar movie night for the incoming staff?

Polite nodding ensued.

A third Board member recalled Chopra’s efforts to oppose political debanking, which encompassed legal action to advance free speech and due process in the banking sector.

Polite nodding ensued again.

Staff then interceded with an update: venture capitalists with a deep portfolio of stage-agnostic bank run expertise have just redefined “debanking” to encompass anti-money laundering requirements that target drug trafficking, terrorism, and fraud. Industry sentiment, as reflected by the whims of the world’s richest man, thus favored action to “Delete CFPB.”

Furrowed brows and smirks ensued.

Consistent with the shift in investors’ perceptions of the balance of risks, nominal Treasury yields across the maturity spectrum increased significantly. Credit quality remained solid in the cases of large and midsize firms, but deteriorated in other sectors. Delinquency rates for credit cards inched upwards. Market data, in other words, suggested aggregate dissatisfaction with Chopra.

A fourth Board member noted Chopra’s decisions to enact a rule that helps consumers easily switch banks, initiate a review of the FDIC’s merger policies under the guise of “financial stability,” and otherwise leverage the so-called “Chopra Doctrine,” a radical enforcement ideology that consists of actually reading a statute and then using it. Moreover, it was Chopra who first recruited Lina Khan to work at the Federal Trade Commission.

Anger and literal shaking ensued, as these actions transgress the most fundamental Fed consensus norm: the banker welfare standard.

Ultimately, Board consensus deemed Chopra “not a great culture fit” due to his “unreserved and sometimes devastating facial expressions.”

Board members’ ensuing discussion included consideration of options for enhancing Chopra’s understanding of institutional norms, including through collegial exchanges of kitchen utensils and educational water sports.

Given the unusual and exigent circumstances, staff were tasked with implementing the discussed actions on an expedited basis by January 20, 2025, as well as with memorializing the actions through videographic means to inform future CFPB directors about Fed norms. As Chopra himself has observed, institutions “must forcefully address” repeat offenders.

The Chair then adjourned the meeting with the standard ritual sacrifice of depositors at a tiny midwestern bank.

ATTENDANCE:

Jerome H. Powell, Chair

Four other Board members

Various associate directors and senior advisers

Several secretaries and lawyers

Emergency backup economists

Laurel Kilgour is a law and policy wrangler. The views expressed herein do not represent the views or sense of humor of the author’s employers or clients, past or present. This is not legal advice about any particular legal situation. Void where prohibited.

It’s always better to be a monopolist. “Ruinous competition” is a drag on a company’s profits, particularly when slothful incumbents are forced to compete on the merits. In the case of banks, competition on the merits means increasing rates on deposits for customers with sizeable savings or decreasing overdraft fees for customers with limited funds.

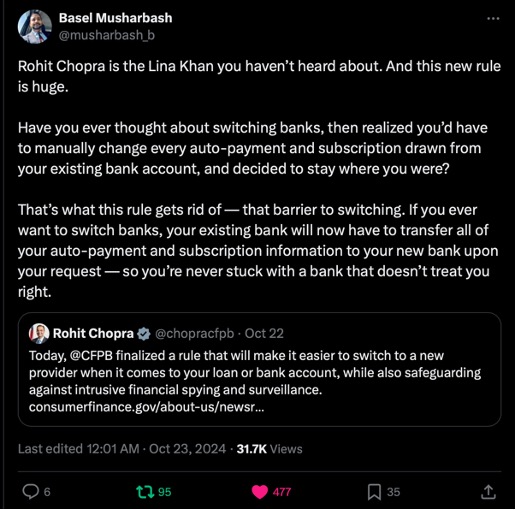

Last week, the Consumer Financial Protection Bureau (CFPB) finalized a rule that requires financial institutions, credit card issuers, and other financial providers to unlock a customer’s personal financial data—including her transaction history—and transfer it to another provider at the consumer’s request for free. It marks the CFPB’s attempt to activate dormant legal authority of Section 1033 of the Consumer Financial Protection Act. Officially dubbed the “Personal Financial Data Rights” rule, or more casually the “Open Banking” rule, the measure was greeted by those in the budding anti-monopolist movement with glee.

Indeed, FTC Chair Lina Khan, the ultimate champion of competition, tweeted an endorsement of the CFPB’s new rule.

But it wasn’t all rave reviews. The Open Banking rule was also greeted by a swift lawsuit from the Bank Policy Institute (BPI), alleging that the bureau exceeded its statutory authority. The lawsuit also claims the rule risks the “safety and soundness” of the banking system by limiting banks’ discretion to deny upstart banks access to transaction histories. Based on its website, BPI’s membership includes JP Morgan Chase, Bank of America, and Barclays, or what I will call the “incumbent banks.” And JP Morgan’s Jaime Dimon is the Chairman of BPI. Why are the incumbent banks so angry about being compelled to share these transaction histories with upstarts, when such data are arguably the property of the banks’ clients in the first place?

When I first heard about the CFPB’s new rule, I didn’t understand why I needed a regulatory intervention to play one bank off another. For example, after being offered a high CD rate by a scrappy bank, I asked my stodgy bank to match it, only to be ignored by my stodgy bank; I proceeded to write a check from the stodgy bank to the scrappier rival. But having studied the issue, I now understand the particular market failure that the rule seeks to address.

The Rule Would Induce More Aggressive Offers by Upstart Banks

When an upstart bank seeks to pick off a customer from an incumbent bank, the upstart would prefer to extend the most aggressive offer possible, as an inducement to overcome any switching costs that customer might incur. (Fun fact: When interest rates were regulated and interest on checking accounts was banned, banks used to compete by offering toasters to customers at rival banks!) Today’s competitive offer by a rival bank might include a host of ancillary services or “cross-sales” alongside a checking account, such as a credit card, a loan, a line of credit, and payment services. The terms of such offers are governed by the customer’s creditworthiness.

And that’s the catch—the incumbent bank and only the incumbent bank has access to the customer’s transaction history, which includes nuggets like your history of maintaining a balance, overdraft tendencies, and relative timing of payments to income streams. The scrappy upstart, by contrast, is flying blind. And this granular information cannot be obtained through the purchase of a credit report.

Economists refer to such a predicament as “asymmetric information,” and in 2001 three economists even won a Nobel prize for explaining how such asymmetries lead to market failures. In the absence of this information, when formulating its offer, the upstart bank must assume the average tendencies of the borrower based on some peer group, or even worse, it might hedge by assuming the borrower’s creditworthiness is slightly worse than average. As a result, the competitive offer is unnecessary weaker than it could be, and too many customers are sticking with their stodgy (and stingy) bank.

(A fun digression: Some employers inject provisions into a worker’s employment contract that create similar frictions to substitution, which relaxes competitive pressure on wages. You’ve likely heard of a non-compete, which is the ultimate friction. But you may not have heard of a “right-to-match” provision, which gives the incumbent employer a right to match any outside offer from a rival employer. Because the rival employer knows of the provision, and because it’s costly for the rival to formulate an offer, most rivals will give up and the employee never enjoys the benefit of competition.)

The purpose of the Open Banking rule is to induce more aggressive offers by upstart banks and thereby overcome the switching costs associated with changing one’s bank. Put differently, it juices the part of the fin-tech community that seeks to assist consumers, which likely explains the narrow opposition to the rule from incumbent players only. Suppose the customer’s switching costs are $100 and the (weakened) offer from an upstart would improve the customer by $90; under those circumstances, the customer stays put. But if the rule can induce more aggressive offers, boosting the customer benefits of switching to (say) $200, the customer moves. Or she now, with a powerful offer in hand, credibly threatens to switch banks and her stodgy bank improves her terms.

The Open Banking Rule Could Generate Billions in Annual Benefits

The economists of the CFPB have tried to value what this enhanced competition might mean for bank customers. At page 525 of the rule, in a section titled “Potential Benefits and Costs to Consumers and Covered Persons,” the economists explain their valuation methodology:

First, those consumers who switch may earn higher interest rates or pay lower fees. To estimate the potential size of this benefit, the CFPB assumes for this analysis that of the approximately $19 trillion 207 in domestic deposits at FDIC- and NCUA-insured institutions, a little under a third ($6 trillion) are interest-bearing deposits held by consumers, as opposed to accounts held by businesses or noninterest-bearing accounts. If, due to the rule, even one percent of consumer deposits were shifted from lower earning deposit accounts to those with interest rates one percentage point (100 basis points) higher, consumers would earn an additional $600 million annually in interest. Similarly, if due to the rule, consumers were able to switch accounts and thereby avoid even one percent of the overdraft and NSF fees they currently pay, they would pay at least $77 million less in fees per year.

Hence, bank customers who switch banks due to more robust competitive offers made possible by the Open Banking rule would benefit by $677 million per year, based on very conservative assumptions about substitution. And this estimate does not include benefits created for those customers who stay put but nevertheless benefit from the mere threat of leaving. The economists explain that competitive reactions by incumbent banks could lead to a doubling of the aforementioned benefits, to the extent that interest rates on deposits of the non-switchers increase by a mere one basis point. Those benefits would be a transfer from incumbent banks to consumers.

Beware of Fraud Arguments

The Open Banking rule requires that a bank make “covered data” available in electronic form to consumers and to certain “authorized third parties” aka the upstart banks. Covered data includes information about transactions, costs, charges, and usage. The rule spells out what an authorized third party must do to get the covered data, as well as what the “data provider” (aka the incumbent bank) must do upon receiving such a request. The data provider will run its normal fraud review process upon receipt of a data request. Indeed, CFPB even included a provision that states when the data provider has a “legitimate risk management concern,” that concern may trump the data sharing rule.

So any claim that the BPI lawsuit is motivated to protect consumers against fraud or to ensure the safety and soundness of the banking system seems farfetched. The more likely motivation for the challenge is that the Open Banking rule will spur competition among banks, and hence put downward pressure on the incumbent banks’ hefty margins. To wit, JP Morgan Chase, America’s biggest bank, has thrived in a rising rate environment, posting record net income figures since 2022. As the CFPB economists estimate, the rule could raise rates on deposits and reduce rates on overdraft fees, cutting into these record margins. In a similar vein, the CFPB’s new rule might spark competition in the nascent payment system market. Some large banks would like to build their own payment systems (think BoA’s Zelle). By compelling the incumbent banks to share their customers’ transaction histories, however, the Open Banking rule reduces the costs for a scrappy entrant to build a competing payment system. If pay-by-bank gets going, it will be a threat to the incumbent banks’ lucrative credit card and debit card interchange fees. And that threat alone provides billions of reasons to sue the CFPB.

Last week, the Consumer Financial Protection Bureau and the Biden White House proposed to limit prices on overdraft protection by banks. This is smart policy and is backed by sound economics.

While inflation ran hot in 2022 and 2023, talk of price controls bubbled to the surface, even in economic circles. University of Massachusetts economist Isabella Weber pointed out that price controls were used successfully during World War II, and deployed effectively by Germany more recently to handle spiraling natural gas prices. Health policy professors interviewed last week by the New York Times noted that other countries, including Canada and France, use price controls to limit inflation in pharmaceuticals. Just a few years ago, price controls were a dirty word in economics—the only imaginable exception being for natural monopolies, where a price cap was set in a way to permit a normal rate of return.

Given the shifting attitudes towards price controls, the CFPB’s overdraft-fee proposal is likely to receive a friendlier reception among economists. The financial watchdog estimates that banks collect about $9 billion annually in overdraft fees, and customers who pay overdraft fees pay about $150 on average every year. Overdraft fees averaged $35 per event in recent years, and a bank can assess multiple fees for one overcharge episode whenever multiple checks bounce due to the overdraft. Moreover, banks engage in practices that induce overdrafts (or greater fees), such as refusing to deposit a check without a ten-day hold or engaging in “high-to-low reordering” (processing a large debit before smaller transactions, even if the latter are posted earlier).

The CFPB’s proposed rule would require banks to justify their overdraft fees on the basis of the bank’s incremental costs; if the banks could not do so, then the fee would be regulated at some price between $3 and $14. The rule would apply to large banks only, which some commentators have pointed out misses some of the worst offenders.

Vulnerable Aftermarkets

Economists recognize that market forces are especially weak when it comes to disciplining the price of ancillary or aftermarket services. The classic teaching example is movie theater popcorn. Customers do not have the price of popcorn on the top of their minds when choosing among theaters; the movie choice and the drive time are paramount. And when they arrive at a theater, customers are not likely to reverse their ticket transaction and find a new theater in response to sky-high popcorn prices; the switching costs would be too steep. The same is true for the price of other common aftermarket services, such as movie rental in hotels and printer cartridges.

Overdraft protection can be understood as an ancillary service to standard checking account services. As one economist at the Federal Reserve put it, “Most bank fees represent an example of add-on or aftermarket fees. Aftermarkets can be found in many industries such as printers (for toner), computers (software), razors (blades) and many others.” When someone is shopping around for where to set up their checking account, they will primarily consider the bank’s reputation and geographic footprint, the proximity of a physical office to their home, and the interest rate offered on savings. Overdraft protection likely is not top of mind, and even if it were, the bank won’t prominently display its overdraft fee on its webpage. Economists have learned through experiments that sending repeat messages to customers with a propensity to incur an overdraft fee was effective, consistent with customers having limited attention.

Indeed, I learned of Bank of America’s overdraft fee ($10) only by invoking the help tab on its website, and then looking through several documents that contained the term “overdraft.” The fee is buried in a document titled “Personal Schedule of Fees.” Given the high costs of switching banks, when a customer is hit with an exorbitant overdraft fee, there is little chance the customer will terminate the relationship—that is, the traditional forces that discipline supracompetitive prices are absent.

The American Bankers Association (ABA) rushed out a statement in opposition to the CFPB proposal, claiming that overdraft fee caps “would make it significantly harder for banks to offer overdraft protection to customers.” (This would only be true if the cap were set below the incremental cost of providing the service.) In support of its opposition, the ABA cited a Morning Consult survey, showing that 88 percent of respondents “find their bank’s overdraft protection valuable,” and 77 percent who have paid an overdraft fee in the past year “were glad their bank covered their overdraft payment, rather than returning or declining payment.”

There’s no doubt bank customers value overdraft protection and detest the notion of bouncing checks to multiple vendors. The relevant economic question, however, is whether market forces can be counted on to price overdraft protection at competitive levels (i.e., near marginal costs). So this survey was a bit of misdirection.

A relevant survey, by contrast, would ask bank customers whether they considered a bank’s overdraft fee when choosing with which company to bank, and whether they would consider switching banks upon learning of the bank’s high overdraft fee. If the answer to either of those questions is no, then bank customers are vulnerable to excessive pricing on overdraft protection.

Who Bears The Burden Matters

The typical customer who bears the burden of excessive overdraft fees is low-income, which means a policy of tolerating overcharges here is highly regressive. Consumer Reports notes that eight percent of bank customers, mostly lower-income, account for nearly three quarters of revenues from overdraft fees. According to a CFPB survey released in December 2023, among households that frequently incurred overdraft fees, 81 percent reported difficulty paying a bill at least once in the past year, another indication of poverty. The CFPB survey also notes that “[w]hile just 10% of households with over $175,000 in income were charged an overdraft or an NSF fee in the previous year, the share is three times higher (34%) among households making less than $65,000.”

When deciding whether to impose price controls of the kind contemplated in the CFPB proposal, the economic straights of the typical overdraft fee payor is important. Economists recognize that customers is aftermarkets are generally vulnerable to high prices, but do not counsel an intervention in each of these markets. A middle-class family that overpays for popcorn at a movie theater does not engender much sympathy; if the price is too high, then can abstain without much consequence. Similarly, learning that an upper-class family overpaid for in-room dining at a boutique hotel similarly does not tug at the heartstrings. But a low-income family that pays a $35 overdraft fee could be missing out on other important things like meals, and is in no position to refuse the service; refusing to comply might jeopardize their credit or banking relationship.

The Element of Surprise

In addition to the weak market forces disciplining the price of aftermarket services, bank customers are particularly vulnerable to exploitation given their lack of knowledge about the fees. The same CFPB survey mentioned above showed that, among those who paid an overdraft fee, only 22 percent of households expected their most recent overdraft fee—that is, for many customers (almost half), the overdraft fee came as a surprise. In discussing the fairness of surprise fees, Nobel prize winner Angus Deaton notes in his new book, Economics in America, that “If you need an ambulance, you are not in the best position to find the best service or to bargain over prices; instead you are helpless and the perfect victim for a predator.” Neoliberal economists might ignore these teachings, and instead trust the market to deliver competitive prices for ambulance services and overdraft fees. But anyone with a modicum of understanding of power imbalances and information asymmetries will quickly recognize that an intervention here is well grounded in economics.

From online banking to e-commerce, advances in technology have given consumers in the digital age new products and services. But the rise of the digital economy has been accompanied by the emergence of digital robber barons. Just as social media companies entrenched their dominance by making it hard for users to port their own content and connections to rival platforms, big banks restricted users’ access to their own financial data to cement their monopoly power.

Data portability is the idea that users should be free to move their data to rival platforms. Before number portability was mandated by Congress in the 1996 Telecom Act and implemented by the FCC in 2003, cellphone customers faced high switching costs—imagine the hassle of informing your friends and family of your number—which limited churn and kept cellphone prices artificially inflated. Now big banks are up to the same tricks: To curb competition from newer and smaller companies, large financial institutions have restricted consumers’ data portability, by for example, making acts as basic as sharing personal financial data or transferring their own funds with a new institution a hassle.

Fortunately, the Consumer Financial Protection Bureau (CFPB) is initiating rulemaking that would facilitate enhanced consumer access to their financial data. Through a provision of the Dodd-Frank Act known as Section 1033, the agency can help take big banks to task and give emerging financial service providers a fair shot to compete.

Like other corporate giants that have faced regulatory scrutiny, big banks aren’t going down without a fight. Bank Policy Institute (BPI), a lobbying group whose membership includes Wells Fargo and JPMorgan Chase, argued in a recent comment letter that strong Section 1033 rulemaking would fuel the rise of Big Tech in the financial industry. BPI’s angle is obvious here: CFPB director Rohit Chopra is a noted supporter of regulating Big Tech, and has scrutinized the tech giants’ encroachment into the payments sector while in office.

But BPI’s spin conveniently ignores that Big Tech has been pushing into the financial services industry largely in collaboration with—and not to compete against—big financial institutions. From Goldman Sachs’ partnership with the Apple Card to TikTok’s recently exposed collaboration with JPMorgan Chase, the giants of the financial and tech industries have a vested interest in shoring up their respective monopoly positions. That BPI member JPMorgan Chase is so eager to collaborate with TikTok, a Chinese-based company drawing increasingly intense bipartisan scrutiny and even calls for its ban in the United States, is just the latest and most galling example of these developments.

Contrary to the bank lobby’s self-serving narrative, strong Section 1033 rulemaking stands to foster innovation by giving emerging companies a fair shot to compete against entrenched incumbents in both industries. Indeed, Section 1033 rulemaking will help level the playing field by giving small players and new entrants the same right to access data that Big Tech can already get its hands on quite easily.

This reality explains why consumer and competition advocates have long argued that strong Section 1033 rulemaking will help encourage competition in the financial services industry. In a 2021 comment before the CFPB, a coalition of consumer organizations led by the National Consumer Law Center argued that “Improved access to consumer-authorized data can benefit competition, which will benefit consumers.” Monopoly power comes at a grave expense to innovation, and at a time when consumers are increasingly interested in alternative relationships, this rulemaking will be a boon to the broader economy and consumer choice.

In the absence of strong Section 1033 rulemaking, access to financial services data risks being decided primarily through backroom dealmaking. It goes without saying that these informal arrangements stand to benefit mega-corporations like Google or Apple, not small players. After all, Google executives will never have a problem getting a meeting with Jamie Dimon, nor will TikTok leadership or the likes of Elon Musk. But emerging players and innovative startups are unlikely to have such opportunities, meaning that a lack of rulemaking will only entrench Big Banks’ gatekeeper status.

It would be a mistake to dismiss these concerns as merely hypothetical. As one recent example, big banks like Chase are fearful that direct account-to-account payment options will cut into their ability to profit off credit card transactions. In response, Chase is using its dominant position to steer consumers away from paying vendors directly from their own bank account. Without strong regulatory intervention, mega-corporations in tech and finance will continue to inhibit the growth of promising new ventures.

Shortly after becoming CFPB director, Chopra noted that “Big Tech companies are eagerly expanding their empires to gain greater control and insight into our spending habits.” He is correct. With the agency finally initiating rulemaking on Section 1033 more than a decade after Dodd-Frank passed into law, Chopra must reject the bank lobby’s bad faith efforts to water down the rules. The CFPB should empower consumers to fully control their personal financial data in the interest of cultivating a fair and truly competitive financial services industry.

Morgan Harper is Director of Policy and Advocacy at the American Economic Liberties Project.