Many Americans are still in shock because our worst fears just came true: European regulators fined an American Big Tech firm a whopping one half of one percent of its annual revenue for violating some kind of “law.” To add insult to injury, radical American enforcers slipped loose from the adult supervision of the defense bar and have filed a volley of their own vindictive lawsuits over the last several years.

Sadly, the onslaught is taking a toll: to staff all of the new investigations, some dominant firms are now likely making do with outside counsel who bill under $2,600 an hour. This translates into skimpy and unimaginative legal defenses.

But protecting our national champions requires more than just copy-pasting now standard unconstitutionality defenses—which often foreshadow separate lawsuits alleging that the FTC’s commissioners and its administrative law judges are unconstitutionally protected from removal by the president—to see what sticks. That’s why we’ve painstakingly curated the following antitrust affirmative defense starter pack for cost-conscious in-house counsel. In giddy anticipation of a coming merger wave unleashed by lax federal antitrust enforcement, there’s no better time to throw merit to the wind and dissolve an enforcement agency or two altogether.

DEFENDANT’S AFFIRMATIVE DEFENSES

FIRST AFFIRMATIVE DEFENSE

(Statute of Limitations / Laches)

The FTC’s claims are barred, in whole or in part, by the fact that we hid evidence from them during the initial merger review process.

SECOND AFFIRMATIVE DEFENSE

(Separation of Norms)

This is not how enforcers did things in the four decades from the day Robert Bork founded the field of antitrust law up until those mean hipsters took over.

THIRD AFFIRMATIVE DEFENSE

(Non-Delegation Doctrine)

The FTC jeopardizes American liberty by delegating this case to lawyers. Only economists steeped in the hard science of cost-benefit analysis can be entrusted with first-chairing trials in this area of the law.

FOURTH AFFIRMATIVE DEFENSE

(Exceeding Hidden Statutory Vibes)

Although to the casual eye, the statute does not literally recite the words “consumer welfare standard,” we reserve the right to submit a supplemental expert microscopy report showing fine graphitic indentations consistent with that phrase on an original paper copy preserved by Robert Bork, Junior. In any event, the claims alleged in the Complaint impermissibly exceed the statute’s inherent vibes.

FIFTH AFFIRMATIVE DEFENSE

(Extratemporal Application of Old Law)

Only precedent dating after the New Deal era is valid, binding law. Accordingly, Brown Shoe (1962) has expired. But old cases that we like still remain valid. So Marbury v. Madison (1803) and that case declaring the exploitation of bakers to be the foundation of American free enterprise (1905) are still good law.

SIXTH AFFIRMATIVE DEFENSE

(Procompetitive Kickbacks)

Bribing our competitors not to compete could, hypothetically, set in motion a chain of events that precipitates world peace. Such procompetitive justifications benefit competition, consumers, sellers, and Mars colonizers alike.

SEVENTH AFFIRMATIVE DEFENSE

(Linguistic Existentialism)

Purported legal standards comprised of meaning-contestable units of language—also known as “words” and “phrases”—violate the Constitution. (Actually, the more Defendant thinks about it, the more Defendant suspects that Defendant’s own “separation of powers” and “non-delegation” doctrines might be void for vagueness and lack intelligible limiting principles. But no matter! That’s why Defendant splurged on the premium “kitchen sink level” affirmative defense package. Ultimately, Defendant is just happy to force federal enforcers to divert scarce resources to defending their very existence).

EIGHTH AFFIRMATIVE DEFENSE

(Hypothetical Monomaniacal Enforcer Test)

The FTC Chair flunks the recusal test we invented for the purpose of flunking enforcers. (We commend certain other Commissioners for preemptively recusing themselves despite the lack of any discernable conflict, and for delegating their authority to economist Mark Israel instead). In any event, our lobbyists are confident that the new Congress will ensure that the act of writing law review articles not commissioned by us will be punishable by deportation and disbarment.

NINTH AFFIRMATIVE DEFENSE

(Branch Errata)

Congress itself was probably just a typo, and must be dissolved to liberate the juristocracy.

TENTH AFFIRMATIVE DEFENSE

(Walker Doctrine)

We only destroyed millions of incriminating communications because California State Bar Member No. 122945 told us to. The “Communicate with Care” policy exemplifies the creative brilliance that Kent Walker brings to his job when advising lawmakers how to write their AI laws. Thus, barring Walker from the remedies phase of this case and from our public affairs efforts would harm innovation.

ELEVENTH AFFIRMATIVE DEFENSE

(No Authority to Proceed in Court)

The FTC lacks authority to pursue the claims alleged and relief sought in district court, because an agency intern once browsed the Terms of Service of Defendant’s parent company’s accountant’s app, which mandates arbitration of all claims. Failing to uphold this freedom of contract would violate the Fourteenth Amendment.

TWELFTH AFFIRMATIVE DEFENSE

(Big Escrow Check)

We reserve our right to reneg on the jury trial we demanded by writing an escrow check that is larger than the entire combined budget of all federal antitrust enforcers and waving it in their faces during voir dire.

THIRTEENTH AFFIRMATIVE DEFENSE

(Defamation)

Filing lawsuits against lawbreakers is mean and irreparably hurts our corporate feelings.

FOURTEENTH AFFIRMATIVE DEFENSE

(Rule 11/Twiqbal Immunity)

Rules about heightened pleading standards and minimum factual and legal bases for taking positions in court apply only to Plaintiffs, not Defendants, silly. (Unless we’re the Plaintiff).

FIFTEENTH AFFIRMATIVE DEFENSE

(Swimming Test, Pricking Test, Spectral Evidence)

Lina Khan is probably a witch (but we can’t know for sure until we subject her to the standard tests).

SIXTEENTH AFFIRMATIVE DEFENSE

(The Reverse Hostage Doctrine)

We’re not trapped in this lawsuit with Lina Khan; Lina Khan is trapped in this lawsuit with us. In fact, we’ll amend our counterclaims to name Lina in her personal capacity when she is replaced as Chair. This is a fight to the death.

SEVENTEENTH AFFIRMATIVE DEFENSE

(Wrong Enforcer Doctrine)

What, Jonathan Kanter filed this lawsuit?

Not Lina Khan?

Fine, then: Defendant admits that AAG Kanter knows the secret biglaw partner handshake, so we hereby stipulate to dismissal of the previous defenses, without prejudice. (We reserve all rights if later discovery reveals that an immigrant woman of color stole Kanter’s CM/ECF electronic filing credentials).

EIGHTEENTH AFFIRMATIVE DEFENSE

(South Pacific Doctrine)

Gonna wash that Part III adjudication right out of our hair.

NINETHEENTH AFFIRMATIVE DEFENSE

(Post-Election Enforcement)

Insofar as the current administration made antitrust “political” for the first time ever, thereby violating our due process rights, Defendant respectfully requests an immediate return to objective economic standards. Our experts have calculated that January 20, 2025 is the most economically auspicious day to drop all pending cases, and we reserve the right to file a motion in limine to enjoin any references to “Inauguration Day” as politicized and unprofessional.

TWENTIETH AFFIRMATIVE DEFENSE

(The Consumer Welfare Standard is Back, Baby)

Not that it ever went anywhere. The radical enforcers both cruelly took it away and never deviated from it. And we all agree on exactly what this objective and easily administrable test means, which is: we know it when we see it. Kind of like that other famous legal test…

TWENTY-FIRST AFFIRMATIVE DEFENSE

(Everyone Hates Matt Gaetz)

We applaud the incoming administration for rethinking its decision to nominate an Attorney General whose private indiscretions do not meet the bar for our moral standards. Our jubilation has nothing to do his obvious bias in favor of enforcing antitrust laws or the fact that his successor’s law firm lobbied for us.

TWENTY-SECOND AFFIRMATIVE DEFENSE

(State Ambush)

Allowing Plaintiff States to continue vigorous enforcement even after federal enforcers diverge in their efforts would be a shocking due process violation.

How could Defendant have known or prepared for this possibility, without any notice other than the listing of 38 distinct signature blocks on every filing as well as active State participation in every meet and confer session, deposition, and hearing for three years? Champagne-swilling Federalist Society boomers assure us that this kind of wanton federalism violates the unitary executive doctrine.

TWENTY-THIRD AFFIRMATIVE DEFENSE

(Denial)

This can’t be happening. Is Thomas on vacation? Did we dial the wrong yacht?

TWENTY-FOURTH AFFIRMATIVE DEFENSE

(Bargaining)

What if we agreed to probation overseen by the esteemed Commissioner Melissa Holyoak instead? Under the vigilant watch of such a fearsome enforcer, we might even be willing to pay a fine of three quarters of one percent of our annual revenue.

TWENTY-FIFTH AFFIRMATIVE DEFENSE

(Acceptance)

Okay fine, we admit that the few hot docs we forgot to destroy mean what they say. But we are still going to take this all the way to the Supreme Court—and then file a motion for relief from the judgment at the district court even after our petition for cert is denied. (Turns out we’re not very good at acceptance, and we had pocket change to spare on rolling the dice).

TWENTY-SIXTH AFFIRMATIVE DEFENSE

(Infinite Placeholder)

Whatever we come up with later, we were retroactively asserting all along, because we have always been at war against Oceania.

TWENTY-SEVENTH AFFIRMATIVE DEFENSE

(Almost Forgot: Failure to State a Claim)

The FTC’s causes of action fail to state a claim upon which relief can be granted.

Laurel Kilgour is a law and policy wrangler. The views expressed herein do not represent the views or sense of humor of the author’s employers or clients, past or present. This is not legal advice about any particular legal situation. Void where prohibited.

There is a tension in the discourse as to the purpose of antitrust policy. In one camp, consumer welfare still reigns supreme. In another, there is greater acceptance that the consumer welfare standard is flawed, or at least controversial. Disciples of the first camp argue that antitrust policy should focus exclusively on increasing output as a proxy for consumer welfare.

Looking backwards, some have argued that the SCOTUS antitrust decisions focus almost entirely on output and price, consistent with consumer welfare. But is that how we should appraise what the Court was doing?

This short missive argues that SCOTUS does not articulate that it is applying consumer welfare. Even if it did, it does not tether that policy to notions of Congressional intent behind the antitrust laws. Indeed, where SCOTUS has said it is embracing Congressional intent, its opinion directly contradicts the notions of consumer welfare.

In a recent paper posted to SSRN titled “Antitrust’s Goals in the Federal Courts,” Herb Hovenkamp argues that to understand antitrust’s objective, we should focus on the words of SCOTUS and the federal courts: “Nearly all of this paper consists of statements from the Supreme Court and lower federal courts and concerns how they define and identify the goals of the antitrust laws.” It bears noting that Hovenkamp has been a strong advocate for consumer welfare theory, which would put him in the first camp. As Hovenkamp pointed out in a previous paper, “In sum, courts almost invariably apply a consumer welfare test.” And as Hovenkamp stated in yet another paper, there is good reason for the courts to do so: “it is a reasonable supposition that consumer welfare is maximized by offering consumers the best quality at the lowest price.”

While others have attempted to insert other policies into consumer welfare—or at least claim it is possible that other policies fit nicely within consumer welfare—the lodestar has always been output. As Hovenkamp professed: “[T]he country is best served by a more-or-less neoclassical antitrust policy with consumer welfare, or output maximization, as its guiding principle.”

Hovenkamp is correct that the courts have used the term consumer welfare. But the push for consumer welfare was not started in the Supreme Court, and the term has not been applied consistently in the way antitrust advocates of the consumer welfare standard might think.

Reading the tea leaves

The first mention of the words “consumer welfare” comes from U.S. v. Dotterweich, a case that sought to interpret the Federal Food, Drug and Cosmetics Act of 1938. The act sought to protect “against abuses of consumer welfare growing out of inadequacies in the Food and Drugs Act of June 30, 1906.”

It is not until 1976, in the Ninth Circuit’s case GTE Sylvania v. Cont’l T.V. Inc., that a court adopted the view that the purpose of antitrust was to protect consumer welfare. “Since the legislative intent underlying the Sherman Act had as its goal the promotion of consumer welfare, we decline blindly to condemn a business practice as illegal per se because it imposes a partial, though perhaps reasonable, limitation on intrabrand competition, when there is a significant possibility that its overall effect is to promote competition between brands.” The Court’s footnote 39 cites to Robert Bork’s 1966 piece. The notion of consumer welfare stayed in the Ninth Circuit for a few years, with Boddicker v. Arizona State Dental Ass’n and Moore v. James H. Matthews & Co.

In 1979, Chief Justice Burger wrote the Supreme Court’s decision in Sonotone. In that case, it appears Burger adopts Bork’s consumer welfare approach. But a careful reading of the full paragraph in which Burger cites Bork leaves that prescription uncertain:

Nothing in the legislative history of § 4 conflicts with our holding today. Many courts and commentators have observed that the respective legislative histories of § 4 of the Clayton Act and § 7 of the Sherman Act, its predecessor, shed no light on Congress’ original understanding of the terms “business or property.”4 Nowhere in the legislative record is specific reference made to the intended scope of those terms. Respondents engage in speculation in arguing that the substitution of the terms “business or property” for the broader language originally proposed by Senator Sherman5 was clearly intended to exclude pecuniary injuries suffered by those who purchase goods and services at retail for personal use. None of the subsequent floor debates reflect any such intent. On the contrary, they suggest that Congress designed the Sherman Act as a “consumer welfare prescription.” R. Bork, The Antitrust Paradox 66 (1978). Certainly, the leading proponents of the legislation perceived the treble-damages remedy of what is now § 4 as a means of protecting consumers from overcharges resulting from price fixing. E.g., 21 Cong.Rec. 2457, 2460, 2558 (1890). [emphasis added]

From there, the lower courts either cited Sonotone, Bork, the Merger Guidelines, or, in one case, Broadcast Music, which did not mention consumer welfare at all.

It was not until Jefferson Parish that the Court again mentions consumer welfare, but only in a concurrence by Justice O’Conner (again citing Broadcast Music). Justice O’Conner wrote: “Dr. Hyde, who competes with the Roux anesthesiologists, and other hospitals in the area, who compete with East Jefferson, may have grounds to complain that the exclusive contract stifles horizontal competition and therefore has an adverse, albeit indirect, impact on consumer welfare even if it is not a tie.” And in the same year, the Court in NCAA v. Board of Oklahoma again quoted Sonotone.

The words appear again in Atl. Richfield Co. v. USA Petroleum Co. in a dissent by Justice Stevens. But here the words are used in contradiction to notions of efficiency. Justice Stevens writes: “The Court, in its haste to excuse illegal behavior in the name of efficiency, has cast aside a century of understanding that our antitrust laws are designed to safeguard more than efficiency and consumer welfare, and that private actions not only compensate the injured, but also deter wrongdoers.” (emphasis added) The line suggests that the purpose of antitrust laws goes beyond short-run welfare maximization.

In his dissent in Eastman Kodak, Justice Scalia accuses the majority of ignoring consumer welfare in application of a per se rule against tying. Similarly, Justice O’Conner, citing consumer welfare, accuses the majority in Edenfield v. Zane of “taking a wrong turn” in areas of speech.

In FCC v. Beach Comm’n Inc., the Court wrestled with an FCC franchising requirement. In explaining its understanding of the purpose of antitrust laws, the Court mentions consumer welfare in a way potentially inconsistent with Bork’s treatment: “Furthermore, small size is only one plausible ownership-related factor contributing to consumer welfare. Subscriber influence is another.” These are not necessarily output- or price-related goals.

In the 1990s, there are two cases in which SCOTUS mentions consumer welfare. In Brooke Group v. Brown & Williamson Tobacco, the Court talks of its precedent, Utah Pie, in terms of how the case has “been criticized on the grounds that such low standards of competitive injury are at odds with the antitrust laws’ traditional concern for consumer welfare and price competition.” It does not, however, explain the meaning of consumer welfare. It merely quotes the usual Chicago School authors as to the point and moves on.

In the 2000s, consumer welfare became more prevalent in SCOTUS discussion, but again without explaining its meaning. Justice Stevens dissents in Granholm v. Heald against the removal of state wine restrictions because of Constitutional concerns. The Court in Weyerhauser notes that without recoupment, predatory pricing improves consumer welfare. Leegin, for all of its careful consideration of overturning Dr. Miles, mentions consumer welfare only three times, once quoting an Amicus brief. In Kirtsaeng, it quotes Hovenkamp in passing for that proposition. In Alston, the Court cautions that judges in implementing a remedy may affect outcomes worse than the market. In a maritime tort case, the dissent warned that overwarning regarding contaminants would injure consumer welfare. In Ohio v. American Express, the Court favorably cites to Leegin for the notion of consumer welfare, but only in passing. In Actavis, too, the dissent points to consumer welfare.

That is the extent of the Supreme Court’s wisdom on consumer welfare. For nearly 100 years, the phrase “consumer welfare” did not appear anywhere in antitrust lore. It did appear elsewhere, a point with which we must contend if the Court knew of term’s existence. Moreover, the Court has inconsistently used the term (within and beyond the antitrust laws), which suggests more haphazard citation than deliberate calculation. Or, perhaps more insidiously, an attempt to alter precedent via seemingly innocent citation leads to its increased usage in antitrust.

Put one shoe on before the other

In contrast to the obscure tea leaves from the aforementioned cases, the Court made a very precise pronouncement as to the purpose of antitrust in 1962. In Brown Shoe v. United States, the Court details the legislative history of the antitrust laws. The Court makes clear it is interpreting legislative history and the will of Congress, not creating its own policy:

In the light of this extensive legislative attention to the measure, and the broad, general language finally selected by Congress for the expression of its will, we think it appropriate to review the history of the amended Act in determining whether the judgment of the court below was consistent with the intent of the legislature.

That legislative history does not detail consumer welfare, and indeed it could not given the passage of the Sherman Act in 1890 and Alfred Marshall’s book, Principles of Economics, published in the same year. Looking backwards—from current understanding and implicitly thrusting that understanding on courts of yesteryear—is a problematic bias of this approach.

The Supreme Court goes on to note other aims of antitrust. It notes a focus on the rising tide of economic concentration. It even mentions some potential defenses, such as two small firms merging or a failing firm:

[A]t the same time that it sought to create an effective tool for preventing all mergers having demonstrable anti-competitive effects, Congress recognized the stimulation to competition that might flow from particular mergers. When concern as to the Act’s breadth was expressed, supporters of the amendments indicated that it would not impede, for example, a merger between two small companies to enable the combination to compete more effectively with larger corporations dominating the relevant market, nor a merger between a corporation which is financially healthy and a failing one which no longer can be a vital competitive factor in the market.

But it fails to mention other goals, including consumer welfare. And it explicitly rejects an efficiencies defense. Indeed, SCOTUS recognized that the goals of antitrust law may contradict expansions of output:

It is competition, not competitors, which the Act protects. But we cannot fail to recognize Congress’ desire to promote competition through the protection of viable, small, locally owned business. Congress appreciated that occasional higher costs and prices might result from the maintenance of fragmented industries and markets. It resolved these competing considerations in favor of decentralization. We must give effect to that decision.

In other words, prices might be higher and output lower when markets are less concentrated, but that is a price we are willing to pay in exchange for greater democracy and greater freedom from economic tyranny.

Looking backwards yields more heat than light

What all of this suggests is a strong movement and perhaps some misunderstandings by the Court about what consumer welfare means. Hovenkamp is right to be skeptical given, as he points out, SCOTUS does not often use the term. But it’s worse than that.

Where the trouble comes in is when Hovenkamp starts looking for output and price discussions as a proxy for consumer welfare. Here, he finds slightly more support in the tea leaves. But my critique of those considerations, beyond the points that overlap here, will have to wait for another blog post. At the very least, suffice it to say: If we’re using output as a measure of welfare, output holds the same problems as have been repeatedly stated as to consumer welfare. And if output is a not a proxy for consumer welfare, then why are we measuring it again?

Using the lens of our current understanding to assess older cases leads to biases that are more inclined to find the Court’s understanding is consistent with ours. Thorstein Veblen said it best: For the economist, “[a] gang of Aleutian Islanders slushing about in the wrack and surf with rakes and magical incantation for the capture of shell-fish are held, in point of taxonomic reality, to be engaged in a feat of hedonistic equilibr[ium] …. And that is all there is to it. Indeed, for economic theory of this kind, that is all there is to any economic situation.”

What we see looking backwards is not necessarily what the Court saw in the moment. And the only time the Court gave explicit meaning to antitrust’s purpose, it recognized that deconcentrating the economy might lead to higher prices and reduced output. More importantly, it recognized other antitrust goals apart those espoused by consumer welfare advocates.

It has become quite common to accuse antitrust enforcers of bias and seek their recusal. FTC Chair Lina Khan and DOJ Antitrust Division AAG Jonathan Kanter have been the subject of calls for recusal in cases involving corporate giants such as Meta, Amazon, and Google.

The argument is that these individuals are biased in their enforcement of antitrust law. Ideology, in the case of Chair Khan, was initially honed by writing an article in law school and working for a non-profit. Learned and developed understanding is something that is somehow problematic to some in the pursuit of antitrust enforcement.

In contrast, nominees to run the DOJ and the FTC frequently have experience defending against agency enforcement. They will spend time at the agency, to varying degrees, making minute changes to the state of current enforcement (or lack thereof). Then, they will leave and go back to the defense bar. That does not create calls of bias. In fact, that time “in the trenches” is celebrated as valuable experience.

Whether defending an action or enforcing an action before returning to the defense bar, the reason that no one objects to that “bias” in those realms is that they share the same faith. Thus, it doesn’t matter if you once represented corporations—the common belief is that antitrust enforcement agencies should not delve too deeply into monopolization, there should be blessing of efficiencies in mergers, and that the risk of improper enforcement is greater than the risk of non-enforcement. All believers of the same principles cannot be biased, after all.

The faith is called “Consumer Welfare.”

But these new enforcement officials aren’t practitioners of that faith. And that is perhaps the primary reason that there is much ire about the draft Merger Guidelines and one if its (many) drafters, FTC Chair Lina Khan. The drafters of those guidelines are seeking to disrupt the Consumer Welfare faith, replacing it with the science of modern economics and a return to the statutory goals.

Yet disciples of the faith do not like change. And their belief system has been beneficial to everyone who spins through the revolving door, often times at rapid velocity. But that same system harms consumers, workers, independent business people, citizens, and anyone else lacking voice and who are not members of this particular faith.

In what follows, I detail why Consumer Welfare Theory is a faith, not science. I then explore how there are multiple sects within that faith and how they interplay with one another, all the while perpetuating the faith. I then detail ways in which the faith protects itself from challenge, both scientific and policy based. Finally, I propose a solution.

The Faith of Consumer Welfare

Consumer Welfare Is Internally and Irretrievably Flawed

A faith, according to one definition in Merriam-Webster dictionary, is a “firm belief in something for which there is no proof.” Faith is closely held, and not readily dismissed even in the face of evidence to the contrary. Faith is powerful and should not be discounted.

But faith is not science. There is no ability to verify empirically someone’s faith. Nor is it necessarily logical. Logic suggests that should some assumption prove false; the claim is rejected. Faith exists even when there is evidence to the contrary.

Consumer Welfare, which is the faith adhered to by agency heads past, is not logical because it is based on disproven theory. Modern economics—the social science of economics and not the Consumer Welfare faith of antitrust practitioners—has disproven consumer welfare theory and surplus approaches to welfare. My coauthors and I have detailed this literature here, here, here, and here. In some instances, we have made new claims of intractable problems, and have been met with silence.

Consumer Welfare and its assumptions have also been empirically disproven in many aspects.

For example, mergers do not create efficiencies by and large, except perhaps by happenstance. But notions of efficiency that flow through merger have been disproven. Much of Consumer Welfare has even been disproven by its own followers, the Post-Chicago School. Yet its disciples cling on. There is also strong evidence of increasing concentration in industries across the United States, lower productivity, greater disparities of income. As a policy for the goals of antitrust, evidence suggests Consumer Welfare theory empirically performs poorly.

Despite these criticisms that condemn the theory, and even though modern economics as a science has moved on from it, Consumer Welfare Theory is embraced today in antitrust law. One might hope for a Kuhnian scientific revolution, but rejection of empiricism and logic is a faith-based decision. Indeed, it is fanatical devotion.

“Follow the Gourd! Follow the Shoe.”

In Monty Python’s The Life of Brian, Brian, a false prophet, drops his shoe and his gourd (literal, not metaphorical gourd). His followers splinter into camps of shoe followers and gourd followers. But Brian remains the leader of both sects.

Similarly, the Chicago School and the Post-Chicago School still cling to the same prophet of Consumer Welfare. The Post-Chicago School debunked many of the claims of the Chicago School, but still clung to the religion. To mark their distinction, the Post-Chicago School argued for a kinder, gentler form of Consumer Welfare: A new testament, if you will. Consumer Welfare as embodied in modern antitrust law was the faith created by High Priest Robert Bork and his followers who sought to curb antitrust enforcement. Yet the faith has expanded, in large part due to defenses of the Consumer Welfare standard stemming from people claiming that they are pro-enforcement.

But it’s hard to know what the various sects of this faith are. As Professor Scott-Morton and Leah Samuel point out, there is no clear definition among the devout about what consumer welfare means:

This divergence in terminology means that participants in a debate about CWS are often talking about fundamentally different things. At some point, despite the best efforts of many economists at many antitrust conferences, this barrier to effective communication has become insurmountable. For reasons that are entirely understandable, Neo-Brandeisians have won the terminology debate in policy discourse and the media. Clear communication isn’t possible among Neo-Brandesians, Borkians, and academic economists when they use different definitions of the same term. Making things worse, any quotation from jurisprudence or analysis of past decades reflects the definition of its time.

The lack of an objective reference is further evidence of the faith-based quality of Consumer Welfare among antitrust practitioners and scholars. However, followers of this approach often blend together and come back to the original faith.

Consider the “output” sect led by Professors Herb Hovenkamp and Fiona Scott-Morton, who appear to believe the goal of antitrust is to maximize output. In this discussion, there is an explicit recognition that output does not increase welfare without strict assumptions. Yet this sect exhibits a faith-based defense of using output to measure welfare and defending consumer surplus: “When those tools [regulation, consumer protection, and product labeling] do a good job, output returns to its role as a good proxy for consumer welfare.”

The authors add: “When an economist examines a practice and concludes that it increases ‘welfare,’ the evidence supporting that claim is commonly that the practice increased output or reduced price.” But that simply isn’t true anymore.

Thus, it appears that the output sect is linking output to consumer welfare (with some herculean assumptions). But not necessarily: Professor Hovenkamp has said that you “don’t even need a welfare metric.” So, output as a sect of welfare assumes output on its own is good. But then again, apparently not always.

Post-Chicago economics added the Trading Partners sect. This sect claims a pro-enforcement stance, but cling to a version of surplus measurement known as “trading partners.” As they point out, as several post-Chicago lawyers and economists stated in their comments regarding the draft Merger Guidelines:

We understand merger analysis to be concerned with the risk that a merger will enhance the exercise of market power, thereby harming trading partners (i.e., buyers, including consumers, and suppliers, including workers). Market structure matters in merger policy when it is an indicator of the risk that firms will have the ability and incentive to lessen competition by exercising market power post-merger (or an enhanced ability and incentive to do so), to the detriment of trading partners (buyers or sellers) in the relevant market.

Professor Hovenkamp, an apparent advocate of this sect as well, states:

What we really want is a name for some class of actors who is injured by either the higher buying price or the lower selling price that attends a monopolistic output reduction. In the case of a traditional consumer the primary cause of this injury is reduced output and higher prices. In the case of a supplier, including a supplier of labor, the primary cause is reduced output and lower selling prices. In both cases there are also injuries to those who are forced out of the market.

As my coauthors and I have stated elsewhere, “This is really a wrinkle on the original Consumer Welfare Standard because it simply adds the input market surplus to the consumer surplus.” It does not account, however, for all the other things that modern economics would include for consideration and the original intent of Congress. However, “to their credit, the Post-Chicago School has demonstrated that even when the antitrust inquiry is limited to prices and costs (that is, total surplus), the Chicago School’s program of weak merger enforcement is not justified.” A New Testament for Consumer Welfare, if you will, without the hellfire and damnation cast toward enforcement like the original.

But that original school of Consumer Welfare still exists. Namely, the original notion that most, if not all intrusions by the government into the market will do more harm than good. While there might be exception for realms of naked price fixing, the remainder of antitrust enforcement should be restrained to a great degree. Let’s call this group the Inner Chamber.

Members of the trading partners sect, the output sect, and the Inner Chamber may be talking past each other in ways that science would not be able to grasp. However, stepping outside the “trenches,” one finds a very common meaning of consumer welfare and a very common understanding of welfare in the science of economics.

Let’s Not Call It Death Grip Consumer Welfare Anymore

In The Wire, Stringer Bell is tasked with the sale of an inferior product. It simply doesn’t work. To attract new customers, Stringer, after consulting his economics professor, decides to rebrand. He has some things to teach his followers:

Stringer: “Alright. Let’s try this. Y’all get jacked by some narcos. But y’all clean. Y’all got an outstanding warrant, like everybody in here, and what do you do?”

Poot: “Give another name.”

Stringer: “Why?”

Bodie: “Because your real name ain’t no good,”

Stringer: “All right — it ain’t good, and? Follow through.”

[silence]

Stringer: “ Alright. ‘Death Grip’ ain’t shit.”

Poot: “We change up the name.”

Stringer: “What else?”

Shamrock: “Yo I got it. Change the caps from red to blue. Make it look like we got some fresh shit.”

To maintain popularity, oftentimes faiths “rebrand.” The goal of rebranding, perhaps, is to regain appeal as time passes.

Rebranding has been advocated in the faith of Consumer Welfare. Consider Leah Samuel and Professor Scott-Morton’s take:

Economists face a huge problem with the label they use for the textbook consumer welfare concept if they want to be understood by a larger society that uses the now-common restrictive definition. To foster understanding, economists should be happy to rebrand what they used to call “consumer welfare.” In his presentation to the FTC in 2018, Carl Shapiro suggested a “Protecting Competition” standard (cheekily subtitled “The Consumer Welfare Standard Done Right With Better Name”). It would have almost the same textbook economic meaning as consumer welfare, but the legal meaning would be explicitly framed as broader than the “consumer welfare standard” that is so railed against in the press and employed by courts.

Rebranding seems like an odd thing for a science to do. If the polestar of antitrust were gravity instead of Consumer Welfare, would we tell academics to stay out of the antitrust lane because in antitrust we mean something different by gravity? Maybe not call it gravity? Apparently.

Physics principles, from which much of neo-classical economics is taken, is still called Physics, although I recognize sub-disciplines emerge. But those sub-disciplines cling to the same principles of science. One simply does not rebrand “gravity,” despite it being the source of many failures of grace.

On the other hand, if no one knows to what they are referencing before the rebrand, there is a risk of Charlatanism. It is already the case that some of the sect leaders move freely between the sects, and there is great potential that even a well-meaning, pro-enforcement sect will be coopted by the dominant anti-enforcement sect within the faith. No, that is not what we mean. You are wrong as to what we mean. As we’ve seen in the Google trial already and in the Microsoft trial, given this confusion, even one’s deeply held core beliefs might change depending on time and place. Take, for example, the cross-examinations of Hal Varian and Richard Schmalensee with their own teachings. Even Robert Bork’s faith has been questioned.

Keeping the Faith

Practitioners of a faith can be harsh to those outside their belief system

Unlike the truly devout, New Brandeisians hate low prices and more output, the story goes:

… Neo-Brandeisians generally do not reject the conclusion that larger firms can benefit from economies of scale and scope. Indeed, Neo-Brandeisians often point to expected economies of scale as a cause for concern regarding mergers and acquisitions because combined entities may be able to lower prices and out-compete some other incumbent firms. This demonstrates that the implementation of Neo-Brandeisian policy prescriptions would likely burden consumers with higher prices and reduced output and/or quality in exchange for some mix of Neo-Brandeisian priorities, such as smaller firm sizes and a larger number of total firms.

Because New Brandeisians take into account other considerations, they must be seeking to injure consumers. Low prices and greater output are THE goal, and competing notions will injure that goal. They are thus labeled “activists” who engage “bad faith” arguments and “myths.”

Faiths frequently use parable to defend the defenseless notion. Rather than debate the importance of measures which modern economics (and ancient Congresses) have deemed important, easier to pin the label of “high price heretic” on the New Brandeisians.

This is perhaps why FTC Chair Lina Khan has been the subject of so much hostility in the antitrust world. The Wall Street Journal, the oracle of Consumer Welfare, has devoted enough space to the FTC Chair that no one could question its devotion to the faith. The defense bar is up in arms. And, with the new draft Merger Guidelines, there are even suggestions that the lords of Consumer Welfare—the Courts—would surely cast out such heresy.

It is common to see the New Brandeisians being cast as the zealots. In recent conversations, people have described the New Brandeisians as “activists” and the draft Merger Guidelines as a “manifesto,” perhaps coming from “Marxists.” Heretics aligned with such heresy must be cast out and shunned.

Faiths Appeal to Established Beliefs, Often to Protect Against a Threat

Faith-based anti-intellectual arguments are not new to economics. Consider the reaction to Pierre Sraffa’s “double switching argument,” which proved that the neoclassical theory of distribution was untenable. Sraffa proved, that in “general, there is no logical way by which the “intensity of capital” can be measured independently of the rate of interest — and hence the widely held neoclassical explanation of distribution of income was logically untenable.”

Paul Samuelson sought to defend the neoclassical religion from the logical contradiction Sraffa proved through allegory–an allegory with heroic assumptions. It was an attempt to defend a lapsed logical proof, but one that was still appealing as a religious allegory. As E.K. Hunt points out by citing Bernard Harcourt:

The neoclassical tradition, like the Christian, believes that profound truths can be told by way of parable. The neoclassical parables are intended to enlighten believers and nonbelievers concerning the forces which determine the distribution of income between profit-earners and wage-earners, the pattern of capital accumulation and economic growth over time, and the choice of the techniques of production associated with these developments. . . . [These] truths . . . were thought to be established . . . before the revelations of the false and true prophets in the course of the recent debate on double switching.

The required assumptions for Consumer Welfare to be measured by output are nigh-impossible to be satisfied on earth. The trading partner approach has flaws that are equivalent to the flaws repeatedly detailed about Consumer Welfare theory. In fact, no sect in the Consumer Welfare religion is immune for these damning scientific criticisms. Unlike scientific revolutions, faith continues merrily on, although some have chosen to cast those proving such criticisms (and moving on to more sound policy) as heretics who seek to do harm, lacking in understanding of science.

Indeed, with regard to any faith lacking in evidence, the appeal is to emotion. C.E. Ferguson, in his preface to the book, admits this (in defense of Samuelson’s parable): “Placing reliance upon neoclassical economic theory is a matter of faith. I personally have the faith; but at present the best I can do to convince others is to invoke the weight of Samuelson’s authority.”

Joan Robinson concluded the debate about double switching with a quote that is apt about consumer welfare and its unproven and unproveable theory. In lambasting Ferguson for failing to engage in scientific endeavor:

No doubt Professor Ferguson’s restatement of “capital” theory will be used to train new generations of students to erect elegant seeming arguments in terms which they cannot define and will confirm econometricians in the search for answers to unaskable questions. Criticism can have no effect. As he himself says, it is a matter of faith.

If Consumer Welfare theory is faith, then I must still provide an answer as to why it is so appealing as such. My answer: Because all the players win.

Faith Is Rewarded

The popularity of a faith is in its ability to create comfort. Karl Marx’s famous line about religion was not disparaging: “Religion is the sigh of the oppressed creature, the heart of a heartless world, and the soul of soulless conditions. It is the opium of the people.” Thus, a religion makes you feel good. Or at least one would hope.

The faith of Consumer Welfare does make everyone involved feel good.

Practitioners and consulting economists can feel good because they are representing the parties before the agencies. They are limiting the excesses of government, while being paid well to do so. For government attorneys, a “win” involves a settlement (it does not matter the degree). A consent decree is a win, for budgetary purposes. A successful trial is a win. And, if the parties abandon a transaction, that is a win, too. While government attorneys are not paid well, they can take solace in doing the “people’s work,” or eventually leave to work on the better-paying side.

I am not stating that there are merchants in the temple that should be cast out. Because this faith allows for profiting from it.

The Faithful Gather to Reinforce Their Faith

Faith is based in part on gathering. The temple for Consumer Welfare adherents is the Marriott Marquis in D.C. The service is the ABA Antitrust Section Spring Meeting. During this service, the practitioners of the religion discuss the meanings of ancient texts. Some are rejected because of their age and in light of modern interpretations, such as Brown Shoe. Others are lauded still because they are consistent with modern thought, such as Marine Bancorp. (Justice Powell wrote the famous memo advocating for conservative antitrust and Consumer Welfare theory). High priests, people who have wrestled with these tomes—economists, law professors, and lawyers—debate within small margins the meanings of these sacred texts, often picking and choosing verses that appeal mostly to themselves.

Unlike other religions, debate (within limits) is welcomed, particularly those who play an important role on “both sides” of the debate. But the debate is friendly compared to the nastiness of attacks on the New Brandeisians. Here, people might switch sects in the Consumer Welfare faith and still be welcomed. They might even switch sides “in the trenches” between government and private practice. It’s not a war. No French crossed into German Bunkers in World War I without being called a traitor or deserter.

Friendly discourse in the faith does not yield an unending number of Wall Street journal op-eds attacking you personally, or your FTC Commissioner colleague calling you a Communist. Both sides, within each sect, is still within the Church of Consumer Welfare’s teachings.

This is perhaps why Chair Khan has been the subject of so much hostility in the antitrust world. The Wall Street Journal, the oracle of Consumer Welfare, has devoted enough space to the FTC Chair that it could itself be the foundation of its own faith. The defense bar is up in arms. And, with the new draft Merger Guidelines, there are even suggestions that the lords of Consumer Welfare—the Courts—would surely cast out such heresy from “Marxists.”

Faith Wavers, but Never Fails

Should one point out that the arguments of faith themselves go against the teachings of the faith, things get awkward. I have at various points sardonically argued that antitrust should only be about per se illegal activity such as price fixing and bid rigging. If monopolies cannot undermine the competitive process because they are temporary and most mergers are efficient, why create such huge taxes on corporations by applying the rule of reason? Indeed, detractors of recent proposed amendments to HSR filings have argued such a point.

If enforcement only makes sense for per se violations, and if the deterrent effect were properly understood by would-be cartels, shouldn’t nearly everyone in the ABA defense bar be out of a job? Shouldn’t most antitrust enforcers similarly be fired? Isn’t antitrust enforcement for single-firm monopolization and merger cases “inefficient?” The response to such a comment is usually that antitrust serves a useful purpose of deterring harmful conduct and mergers. But doesn’t it also create great Type I errors? Should we not weigh those? Raise this argument at the Spring Meeting and watch the rallying cry of the defense bar for the antitrust status quo.

But even those practitioners of the Consumer Welfare Religion who earnestly seek broader antitrust enforcement have limits in their faith. Consider an argument I pose frequently to disciples of efficiency (cost savings), a tenet of the Consumer Welfare religion. Consider a merger between two firms (both do business in the United States). Suppose one has beneficial ties to a country where child labor is legal, and the other has capital to build plants there. Suppose the firms prove (and the foreign government also corroborates) that the merger will lower costs, increase output, and use child labor as the basis of the lower costs. Disciples will call into question whether their religion has anything to say on this, despite the efficiency doctrine being right there for the taking. Implicit in the discomfort is a recognition that antitrust has other purposes at hand. The hypothetical tests their faith.

The point of this example is not that supporters of consumer welfare are pro-slavery and pro-child labor. The point of the example is that faith wavers, but not for long.

Adding Science by Killing Faith

When a discipline ceases being a science and becomes a faith, it can no longer accept advancements. Entrenchment becomes the norm. And ultimately, the field dies under its own ignorance, perhaps taking society down with it.

The New Brandeisians have modern economics—the science, not the Consumer Welfare faith—on their side as well as the original goals of Congress in passing the antitrust laws. Antitrust law was hijacked by Consumer Welfare theory, and it is time to put an end to that flawed economic science now undertaken as faith. To question the status quo, as Galileo discovered, no doubt creates hostility.

As New Brandeisians fight the fight, it is almost with glee that members of the Consumer Welfare Faith celebrate the losses. With the remorse is an gleeful tone when some members of the defense bar speaks of the FTC’s losing streak. As Homer Simpson once famously said, “Well son, you tried and you failed. The point is, never try.” In terms of single-firm monopolization cases, the agencies, until very recently, appeared to have taken this advice.

Some Solutions and a Conclusion

I do not have answers that will ever be implemented given the strength of the faith and the forces that propel it. I’m sorry if you thought I would, having taken my statement in the introduction that I had such solutions on faith.

That’s the thing about faith. Sometimes it isn’t warranted.

The views in this essay do not reflect the view of my coauthors, my employer (the Great State of Texas), the Utah Project, my school of Kung Fu, or any other group with which I’m affiliated. I speak solely for myself. I do not have any clients. I am not seeking any appointment to any government agency. Nor do I anticipate them seeking me. I don’t anticipate any of those things changing after I write this.

This piece originally appeared in ProMarket but was subsequently retracted, with the following blurb (agreed-upon language between ProMarket’s Luigi Zingales and the authors):

“ProMarket published the article “The Antitrust Output Goal Cannot Measure Welfare.” The main claim of the article was that “a shift out in a production possibility frontier does not necessarily increase welfare, as assessed by a social welfare function.” The published version was unclear on whether the theorem contained in the article was a statement about an equilibrium outcome or a mere existence claim, regardless of the possibility that this outcome might occur in equilibrium. When we asked the authors to clarify, they stated that their claim regarded only the existence of such points, not their occurrence in equilibrium. After this clarification, ProMarket decided that the article was uninteresting and withdrew its publication.”

The source of the complaint that caused the retraction was, according to Zingales, a ProMarket Advisory Board member. The authors had no contact with that person, nor do we know who it is. We would have welcomed published scholarly debate versus retraction compelled by an anonymous Board Member.

We reproduce the piece in its entirety here. In addition, we provide our proposed revision to the piece, which we wrote to clear up the confusion that it was claimed was created by the first piece. We will let our readers be the judge of the piece’s interest. Of course, if you have any criticisms, we welcome professional scholarly debate.

(By the way, given that the piece never mentions supply or demand or prices, it is a mystery to us why any competent economist could have thought it was about “equilibrium.” But perhaps “equilibrium” was a pretext for removing the article for other reasons.)

The Antitrust Output Goal Cannot Measure Welfare (ORIGINAL POST)

Many antitrust scholars and practitioners use output to measure welfare. Darren Bush, Gabriel A. Lozada, and Mark Glick write that this association fails on theoretical grounds and that ideas of welfare require a much more sophisticated understanding.

By Darren Bush, Gabriel A. Lozada, and Mark Glick

Debate seems to have pivoted in the discourse on consumer welfare theory to the question of whether welfare can be indirectly measured based upon output. The tamest of these claims is not that output measures welfare, but that generally, output increases are associated with increases in economic welfare.

This claim, even at its tamest, is false. For one, welfare depends on more than just output, and increasing output may detrimentally affect some of the other factors which welfare depends on. For example, increasing output may cause working conditions to deteriorate; may cause competing firms to close, resulting in increased unemployment, regional deindustrialization, and fewer avenues for small business formation; may increase pollution; may increase the political power of the growing firm, resulting in more public policy controversies and, yes, more lawsuits being decided in its interest; and may adversely affect suppliers.

Even if we completely ignore those realities, it is still possible for an increase in output to reduce welfare. These two short proofs show that even in the complete absence of these other effects—that is, even if we assume that people obtain welfare exclusively by receiving commodities, which they always want more of—increasing output may reduce welfare.

We will first prove that it is possible for an increase in output to reduce welfare under the assumption that welfare is assessed by a social planner. Then we will prove it assuming no social planner, so that welfare is assessed strictly via individuals’ utility levels.

The Social Planner Proof

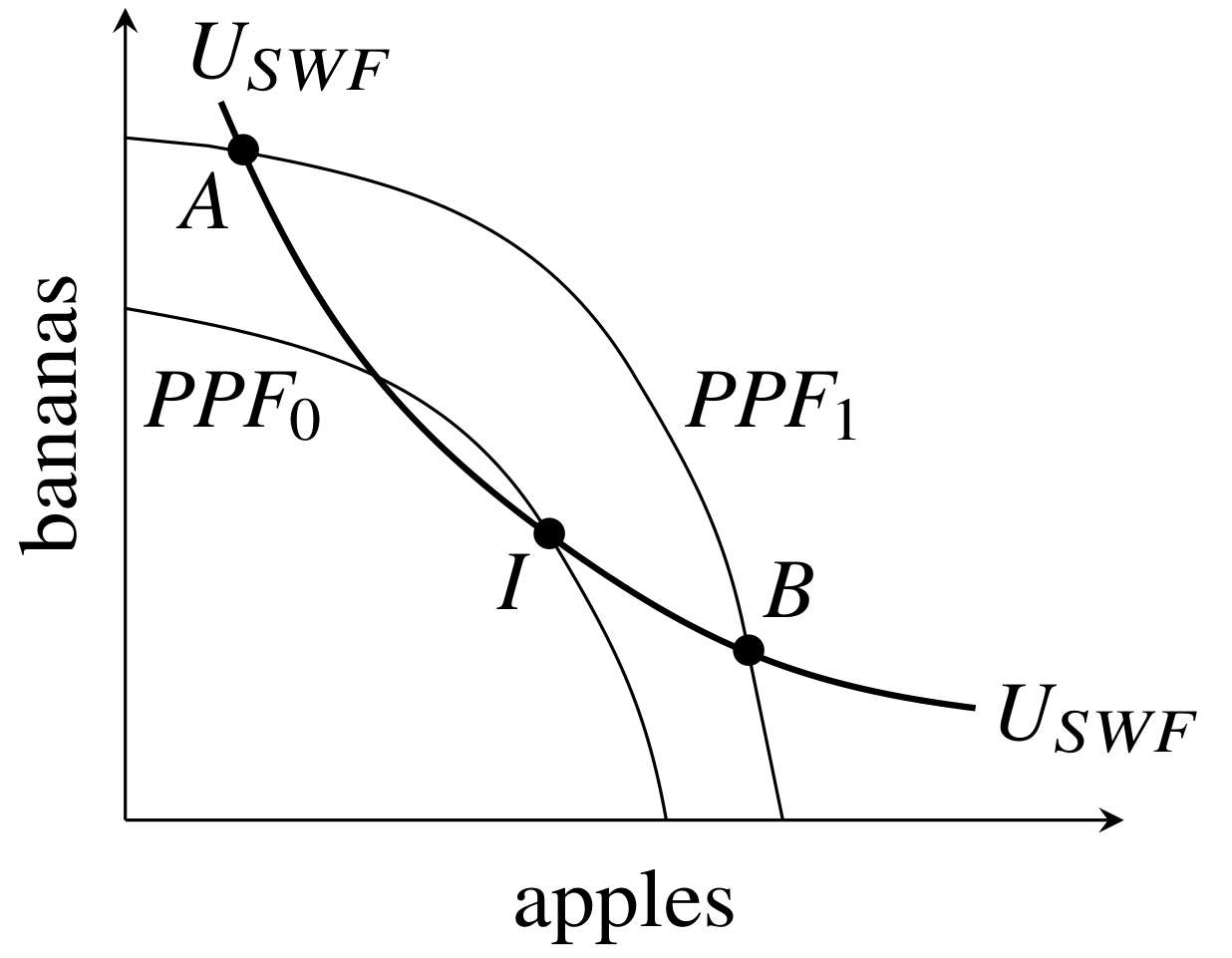

Here we show that a shift out in a production possibility frontier does not necessarily increase welfare, as assessed by a social welfare function.

Suppose in the figure below that the original production possibility frontier is PPF0 and

the new production possibility frontier is PPF1. Let USWF be the original level of social welfare, so that the curve in the diagram labeled USWF is the social indifference curve when the technology is represented by PPF0. This implies that when the technology is at PPF0, society chooses the socially optimal point, I, on PPF0. Next, suppose there is an increase in potential output, to PPF1. If society moves to a point on PPF1 which is above and to the left of point A, or is below and to the right of point B, then society will be worse off on PPF1 than it was on PPF0. Even though output increased, depending on the social indifference curve and the composition of the new output, there can be lower social welfare.

The Individual Utility Proof

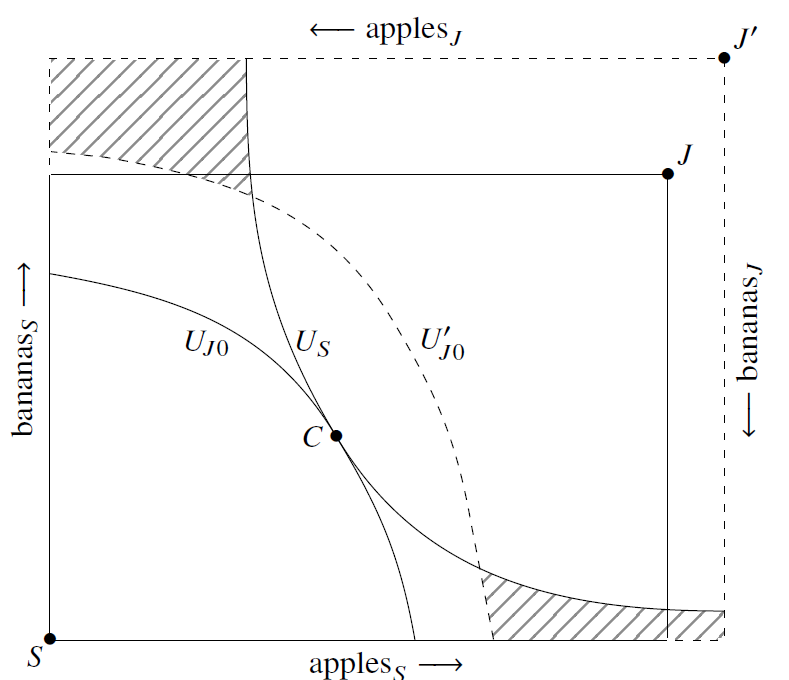

Next, we continue to assume that only consumption of commodities determines welfare, and we show that when output increases every individual can be worse off. Consider the figure below, which represents an initial Edgeworth Box having solid borders, and a new, expanded Edgeworth Box, with dashed borders. The expanded Edgeworth Box represents an increase in output for both apples and bananas, the two goods in this economy.

The original, smaller Edgeworth Box has an origin for Jones labeled J and an origin for Smith labeled S. In this smaller Edgeworth Box, suppose the initial position is at C. The indifference curve UJ0 represents Jones’s initial level of utility with the smaller Edgeworth Box, and the indifference curve US represents Smith’s initial level of utility with the smaller Box. In the larger Edgeworth Box, Jones’s origin shifts from J to J’, and his UJ0 indifference curve correspondingly shifts to UJ0′. Smiths’ US indifference curve does not shift. The hatched areas in the graph are all the allocations in the bigger Edgeworth Box which are worse for both Smith and Jones compared to the original allocation in the smaller Edgeworth Box.

In other words, despite the fact that output has increased, if the new allocation is in the hatched area, then Smith and Jones both prefer the world where output is lower. We get this result because welfare is affected by allocation and distribution as well as by the sheer amount of output, and more output, if mis-allocated or poorly distributed, can decrease welfare.

GDP also does not measure aggregate Welfare

The argument that “output” alone measures welfare sometimes refers not to literal output, as in the two examples above, but to a reified notion of “output.” A good example is GDP. GDP is the aggregated monetary value of all final goods and services, weighted using current prices. Welfare economists, beginning with Richard Easterlin, have understood that GDP does not accurately measure economic well-being. Since prices are used for the aggregation, GDP incorporates the effects of income distribution, but in a way which hides this dependence, making GDP seem value-free although it is not. In addition, using GDP as a measure of welfare deliberately ignores many important welfare effects while only taking into account output. As Amit Kapoor and Bibek Debroy put it:

GDP takes a positive count of the cars we produce but does not account for the emissions they generate; it adds the value of the sugar-laced beverages we sell but fails to subtract the health problems they cause; it includes the value of building new cities but does not discount for the vital forests they replace. As Robert Kennedy put it in his famous election speech in 1968, “it [GDP] measures everything in short, except that which makes life worthwhile.”

Any industry-specific measure of price-weighted “output” or firm-specific measure of price-weighted “output” is similarly flawed.

For these reasons, few, if any, welfare economists would today use GNP alone to assess a nation’s welfare, preferring instead to use a collection of “social indicators.”

Conclusion

Output should not be the sole criterion for antitrust policy. We can do a better job of using competition policy to increase human welfare without this dogma. In this article, we showed that we cannot be certain that output increases welfare even in a purely hypothetical world where welfare depends solely on the output of commodities. In the real world, where welfare depends on a multitude of factors besides output—many of which can be addressed by competition policy—the case against a unilateral output goal is much stronger.

Addendum

The Original Sling posting inadvertently left off the two proposed graphs that we drew as we sought to remedy the Anonymous Board Member’s confusion about “equilibrium.” We now add the graphs we proposed. The explanation of the graphs was similar, and the discussion of GNP was identical to the original version.

The Proof if there is a Social Welfare Function (Revised Graph)

The Individual Utility Proof (Revised Graph)

The New Merger Guidelines (the “Guidelines”) provide a framework for analyzing when proposed mergers likely violate Section 7 of the Clayton Act that is more faithful to controlling law and Congressional intent than earlier Guidelines. The thirteen guidelines presented in the new Guidelines go quite a long way in pulling the Agencies back from an approach that placed undue burden on plaintiffs and ignored important factors such as the trend in market concentration and serial mergers that were addressed by earlier Supreme Court precedent. The Guidelines also incorporate the modern, more objective economics of the post-Chicago school of economics. For these reasons, and others, the Guidelines should be applauded.

Unfortunately, remnants of Judge Bork’s Consumer Welfare Standard remain. In several places the Guidelines refer to a merger’s anticompetitive effects as price, quantity (output), product quality or variety, and innovation. These are all effects that can shift demand curves or equilibrium positions in the output market and thus increase consumer surplus, the only goal recognized by the Consumer Welfare Standard.

To their credit, the Guidelines also mention input markets, referring to mergers that decrease wages, lower benefits or cause working conditions to deteriorate. Lower wages reduce labor surplus (rent), a consideration that would come within a Total Trading Partner Surplus approach. However, the traditional goals of antitrust as articulated by Congress and many Supreme Court opinions, including protecting democracy through dispersion of economic and political power, protection of small business, and preventing unequal income and wealth distribution, are conspicuously absent.

The basis for these traditional goals is well known. Prominent economist Stephen Martin has documented the judicial and congressional statements concerning the antitrust goal of dispersion of power. The historical support for the goal of preserving small business can be found in a recent paper by two of the authors of this piece. Lina Khan and Sandeep Vaheesan, and Robert Lande and Sandeep Vaheesan, have laid out the textual support for the antitrust inequality goal. Moreover, welfare economists have empirically demonstrated significant positive welfare effects from democracy, small business formation, and income equality.

Indeed, the Brown Shoe opinion, on which the Guidelines heavily rely, examined whether the lower court opinion was “consistent with the intent of the legislature” which drafted the 1950 Amendments, and the opinion itself refers to the goal of “protection of small businesses” in at least two places. The legislative history of the 1950 Amendment deemed important by the Brown Shoe Court evinced a clear concern that rising concentration will, according to Senator O’Mahoney, “result in a terrific drive toward a totalitarian government.”

The remnants of the Consumer Welfare Standard are most evident in the Guidelines’ rebuttal section on efficiencies. The Guidelines open the section with the recognition that controlling precedent is clear that efficiencies are not a defense to a merger that violates Section 7; accordingly, the section is offered as a rebuttal rather than a defense. In essence, if the merging parties can identify merger-specific and verifiable efficiencies, it can rebut a finding that the merger substantially lessened competition. The Guidelines do not define “efficiencies.” However, the context makes clear that Guidelines mean to follow previous versions of the Merger Guidelines, that assume “efficiencies” are primarily cost savings. A defendant can offer a rebuttal to a presumption that a merger may significantly harm competition, if such cost savings are passed through to consumers in lower prices, to a degree that offsets any potential post-merger price increase. There are at least six reasons why the Agencies should jettison this “efficiency” rebuttal.

First, lower prices resulting from cost savings are quite a bit different than lower prices resulting from entry (rebuttal by entry). New entry reduces concentration, but cost savings at best will only lower output price, and higher prices (or reduced output) is not the sole problem that results from high concentration except under a strict Consumer Welfare Standard.

Second, to the extent the Guidelines equate efficiencies with cost savings (as in earlier merger guidelines), they have adopted the businessman’s definition of efficiencies. In contrast, economic theory suggests that some cost savings lower rather than raise social welfare. For example, cost savings from lower wages, greater unemployment, or redistribution between stakeholders can both lower welfare and reduce prices. An increase in consumer or producer surplus that comes at the expense of input supplier surplus can also lower welfare.

Third, only under the output-market half of a surplus theory of economic welfare, which is the original Consumer Welfare Standard, can one clearly link cost savings to economic welfare, because lower cost increases consumer and/or producer surplus. As we show elsewhere, this theory has been thoroughly discredited by welfare economists. In fact, for economists, “efficiency” only means Pareto efficiency. As discussed by Gregory Werden and by Mas-Colell et al.’s leading Microeconomics textbook (Chapter 10), the assumptions necessary to ensure that maximizing surplus results in Pareto Efficiency are extreme and unrealistic. These assumptions include quasilinear utility, perfectly competitive other markets, and lump sum wealth redistributions that maximize social welfare. This discredits the surplus approach, which is the only way to reconcile Pareto Efficiency, which is what efficiencies mean in economic theory, with cost savings, which is the definition implied in the Guidelines.

Fourth, the efficiency section is superfluous. As many economists have recognized, most recently Nancy Rose and Jonathan Sallet, the merging parties are already credited for efficiencies (cost savings) in the “standard efficiency credit” which undergirds Guideline 1. After all, absent any efficiencies, why allow any merger that evenly weakly increases concentration? A concentration screen that allows some mergers and not others must be assuming that all mergers come with some socially beneficial cost savings. Why do we need another rebuttal section when cost savings have already been credited?

Fifth, there is no empirical research to suggest that mergers that increase concentration actually lower costs and pass on sufficient benefits to consumers to constitute a successful rebuttal. As one district court commented, “The Court is not aware of any case, and Defendants have cited none, where the merging parties have successfully rebutted the government’s prima facia case on the strength of the efficiencies.” We have identified nine studies measuring either cost savings or productivity gains or profitability from mergers spanning industries like health insurance, banking, utility, manufacturing, beer, and concrete industries. Five of these studies find no evidence of productivity gain or a cost reduction. The other four studies find productivity gains in terms of cost savings; but three of these four studies report a significant increase in prices to the consumers post-merger, and the remaining study does not report price effects post-merger. In other words, we have not been able to find any empirical study showing post-merger pass on of cost savings to consumers. These results are consistent with those of Professor Kwoka, who performs a comprehensive meta-analysis of the price effects of horizontal mergers and finds that the post-merger price at the product-level increases by 7.2 percent on average, holding all other influences constant. More than 80 percent of product prices show increases, and those increases average 10.1 percent.

Sixth, even if there were cost savings from mergers it is unlikely that they would be merger- specific and verifiable. Earlier versions of the Merger Guidelines expressed skepticism that economies of scale or scope could not be achieved by internal expansion (1968 Merger Guidelines) or that cost savings related to “procurement, management or capital costs” would be merger specific (1997 Merger Guidelines). In their article on merger efficiencies, Fisher and Lande write that “it would be extremely difficult for merging firms to prove that they could not attain the anticipated efficiencies or quality improvements through internal expansion.” Louis Kaplow has argued that the ability to use contracting to achieve claimed efficiencies is seriously underappreciated or studied. Verification of future efficiencies is also inherently problematic. The 1997 Merger Guidelines state that efficiencies related to R&D are “less susceptible to verification.” This problem and other verification hurdles are discussed by Joe Brodley and John Kwoka. In summary, the New Merger Guidelines could be improved by a footnote in Guideline One clarifying the multiple antitrust goals Congress sought to achieve by preventing concentrated markets through mergers. In addition, the Agencies should take seriously the holdings of at least three Supreme Court Opinions, none of which have been overturned (Brown Shoe, Phila. Nat’l Bank and Procter & Gamble Co.) that (as quoted in the Guidelines) “possible economies [from a merger] cannot be used as a defense to illegality.” There are good reasons to abandon an efficiencies rebuttal as well.

Mark Glick, Pavitra Govindan and Gabriel A. Lozada are professors in the economics department at the University of Utah. Darren Bush is a professor in the law school at the University of Houston.