Haters sometimes accuse the Federal Reserve of being a shadowy cabal of private bankers that slipped loose from democratic oversight. But we at The Sling trust our patriotic central bankers, who have never had anything to hide. To help the Fed tell its side of the story, we submitted a Freedom of Information Act (FOIA) request to retrieve recent meeting minutes.

Readers may be surprised to learn that although the Fed has acquired a great deal of independent authority, in some circumstances it must consult with other financial regulators, including the Federal Deposit Insurance Corporation (FDIC). The FDIC’s five-member board includes the FDIC Chair, the Comptroller of the Currency, two members of the minority party, and, much to the Fed’s chagrin, the Director of the Consumer Financial Protection Bureau (CFPB)—an agency created in the wake of the Great Financial Crisis to protect consumers from financial scams and frauds. The CFPB is housed within and funded by the Fed, yet sometimes in its short history it has been led by a director who violates Fed norms by having different values and expressing different opinions than the Fed Chair.

The below meeting minute excerpts shine light on the internal operations of the Fed and its valiant efforts to rein in consensus-destroyer Rohit Chopra, the outgoing director of the CFPB.

Minutes of the Board of Governors of the Federal Reserve System

At its meeting yesterday, the Board discussed how the market-implied path for the federal funds rate forecasted certain headwinds to central bank hegemony (aka “bankocracy”). In particular, over the intermeeting period, options on interest rate futures indicated that market participants were increasingly exasperated with Rohit Chopra.

Such developments reflected elevated concerns among investors that Chopra would not only continue to penalize a broad range of business innovation by returning billions of dollars to swindled consumers, but would also decline to rubber-stamp the Fed’s Basel III endgame proposal to allow banks to hold only a single-digit percentage of capital as a cushion against potential losses. Congress had directed the Fed to impose these reserve requirements shortly after the Great Financial Crisis. That the process is still in the proposal stage over a decade later confirms what the Fed tells every interviewer: its biggest fault is being a perfectionist. The Fed is strongly committed to crafting every clause just right, and sometimes unweaves an entire tapestry at night to punish itself for typos and ward off inappropriate suitors. In any event, the Fed recently retained a new associate therapist; a development that warrants greater investor confidence in a declining VIX and short-term higher yields on its regulatory efforts. Members also concurred that although the Fed sets the price of money, it cannot reasonably be characterized as a “price control agency” because reasons.

Market-based measures of exasperation were further articulated by one Board member who explained that Chopra’s un-collegial actions never would have been tolerated by past chairs: “Paul [Volcker] would have been shocked.” The Board then reviewed other deviations from consensus, such as Chopra’s decision to jeopardize national security by stopping financial institutions from stockpiling strategic junk fee reserves—a policy in marked tension with his professed goal of increasing capital reserves.

A second Board member remarked upon Chopra’s stellar credentials and their alignment with the Fed milieu: Harvard undergrad, Wharton MBA, and close relationships with “financiers, convicted felons, and everything in between.” The member likewise approvingly noted that so far, Chopra has not publicly questioned Supreme Court dicta retconning the existence of the Fed as Constitutionally sound based on the rigorous principle of being a “special arrangement sanctioned by history.” The member further recognized and commended Chopra’s benefits orientation sessions, which helped Board colleagues and staff sign up for the best available health and life insurance options, making Open Enrollment much less stressful. Perhaps as a gesture of good faith, Chopra could also set up a dollar movie night for the incoming staff?

Polite nodding ensued.

A third Board member recalled Chopra’s efforts to oppose political debanking, which encompassed legal action to advance free speech and due process in the banking sector.

Polite nodding ensued again.

Staff then interceded with an update: venture capitalists with a deep portfolio of stage-agnostic bank run expertise have just redefined “debanking” to encompass anti-money laundering requirements that target drug trafficking, terrorism, and fraud. Industry sentiment, as reflected by the whims of the world’s richest man, thus favored action to “Delete CFPB.”

Furrowed brows and smirks ensued.

Consistent with the shift in investors’ perceptions of the balance of risks, nominal Treasury yields across the maturity spectrum increased significantly. Credit quality remained solid in the cases of large and midsize firms, but deteriorated in other sectors. Delinquency rates for credit cards inched upwards. Market data, in other words, suggested aggregate dissatisfaction with Chopra.

A fourth Board member noted Chopra’s decisions to enact a rule that helps consumers easily switch banks, initiate a review of the FDIC’s merger policies under the guise of “financial stability,” and otherwise leverage the so-called “Chopra Doctrine,” a radical enforcement ideology that consists of actually reading a statute and then using it. Moreover, it was Chopra who first recruited Lina Khan to work at the Federal Trade Commission.

Anger and literal shaking ensued, as these actions transgress the most fundamental Fed consensus norm: the banker welfare standard.

Ultimately, Board consensus deemed Chopra “not a great culture fit” due to his “unreserved and sometimes devastating facial expressions.”

Board members’ ensuing discussion included consideration of options for enhancing Chopra’s understanding of institutional norms, including through collegial exchanges of kitchen utensils and educational water sports.

Given the unusual and exigent circumstances, staff were tasked with implementing the discussed actions on an expedited basis by January 20, 2025, as well as with memorializing the actions through videographic means to inform future CFPB directors about Fed norms. As Chopra himself has observed, institutions “must forcefully address” repeat offenders.

The Chair then adjourned the meeting with the standard ritual sacrifice of depositors at a tiny midwestern bank.

ATTENDANCE:

Jerome H. Powell, Chair

Four other Board members

Various associate directors and senior advisers

Several secretaries and lawyers

Emergency backup economists

Laurel Kilgour is a law and policy wrangler. The views expressed herein do not represent the views or sense of humor of the author’s employers or clients, past or present. This is not legal advice about any particular legal situation. Void where prohibited.

After years of inflation-driven concerns over the state of the economy, it seems that the mythical soft landing has been achieved; things aren’t perfect but inflation is down without the United States hitting a recession. The labor market has weakened some in recent months, but is still largely okay and the Federal Reserve has started cutting rates in a move to ease downward pressure on employment. In 2022, Bloomberg Economics put the odds of a recession within the next year at 100 percent. Two years later and not only has there not been a recession, but inflation is down, interest rates are going down, and recent GDP growth has been higher than it was for the previous decade.

Over the last several months, while this situation was crystalizing, many have credited Federal Reserve Chair Jerome Powell with achieving the once-mythical soft landing. That’s a mistake. There are multiple reasons why the Fed has been ineffective at best at wielding monetary policy in its recent inflation fighting. Such an explanation doesn’t fit the available empirics—or its advocates’ own model of how interest rates work.

The issue is especially salient because many of Powell’s defenders, including neoliberal economists and pundits, cling to the view that inflation was driven by demand-side factors. This spending-is-to-blame philosophy conveniently exonerates businesses for having any role in driving inflation. If demand-side explanations can be excluded, then attention would shift back to supply-based theories of inflation, including price gouging and coordinated price increases. And that would lead to very different policy implications.

A Brief History Lesson

Let’s rewind to when the fight over monetary policy was heating up in 2022. A variety of different economic shocks have hit the United States: the worst pandemic in a century, major emergency stimulus, brittle supply chains, and a land war in Europe (between Russia—one of the world’s major oil producers—and Ukraine—one of its major grain producers) have all rocked markets in just two years. Then, corporations in concentrated markets seize on the pricing mayhem to pad profits, extending inflationary pressures. At this point, such rent-seeking is well documented. That includes work from researchers from at least three regional Federal Reserve Banks (Boston, San Francisco, and Kansas City), the Bank of Canada, the International Monetary Fund, and the European Central Bank.

Because of this suite of shocks, inflation spiked more aggressively than it had for decades. That spike prompted the Fed to begin a major series of interest rate hikes to attempt to rein in price increases. This whole time there’s a back and forth among economists and pundits on what caused inflation, how long it would last, and what to do about it.

On one side you had Team Transitory, who said that the cause was a bunch of exogenous shocks, inflation wouldn’t last all that long, and we should wait things out because inflation will naturally subside and using monetary policy risked hurting workers.

On the other was what I called Team Crash The Economy, who said that the cause of inflation was fiscal stimulus leading to excess spending, price growth wouldn’t return to normal on its own, and the Fed should aggressively hike interest rates to cool the economy—including destroying millions of jobs. Larry Summers infamously called for ten percent unemployment while lounging on a beach.

In retrospect, Team Transitory was largely correct about the causes; fiscal stimulus played a role, but wasn’t responsible for most of inflation. Technically, Team Crash The Economy was right on the timeframe question, but the reasoning behind why inflation lasted a long time was demonstrably incorrect. Conversely, Team Transitory was technically wrong about the timeframe, but the reasoning was at least partially true.

But then there’s the big question of what the solution was. Both teams have taken victory laps: Team Transitory back in 2023 when inflation eased, except for a few lagging variables (housing, wages) and commodities (oil) that kept overall measures high; and Team Crash The Economy over the summer, when they pointed at decreased inflation and credited Jerome Powell and the Fed for the result.

The Econ 101 Model

The intro macro model for the relationship between inflation and interest rates is largely just an inverse relationship. As interest rates are eased, businesses face cheaper borrowing costs, inducing them to scale up operations, creating new jobs. Then when the labor market tightens, it creates a “wage-price spiral.” As people get paid more, they spend more, leading suppliers to scale up again, further tightening the labor market, leading to higher wages, and on and on. In this econ 101 telling, the key link between inflation and interest rates is those pesky workers demanding higher wages, which create a cycle of increasing demand. That’s why the solution is a form of “demand destruction,” forcing consumers to consume less (by making credit more expensive) in order to reduce demand-side pressure on prices.

So if a central bank finds itself making monetary policy using this framework in an inflationary environment, what does it do? It hikes rates, making borrowing costs prohibitively high, which leads firms to stop expanding and, if the costs increase enough, to actually shrink their business via measures like layoffs, putting an end to wage increases, or even shuttering entirely. And then as wages stagnate (or, in extreme cases, decrease), there’s less demand, so prices don’t continue their rapid increase (or, in extreme cases, fall).

Within the econ 101 frame, this makes sense and is the obvious choice. But in the real world, it didn’t fight inflation. Nearly every step of that theoretical model can be observed and empirics clearly do not show the proscribed pattern. On top of that, there are blatant theoretical holes in that narrative.

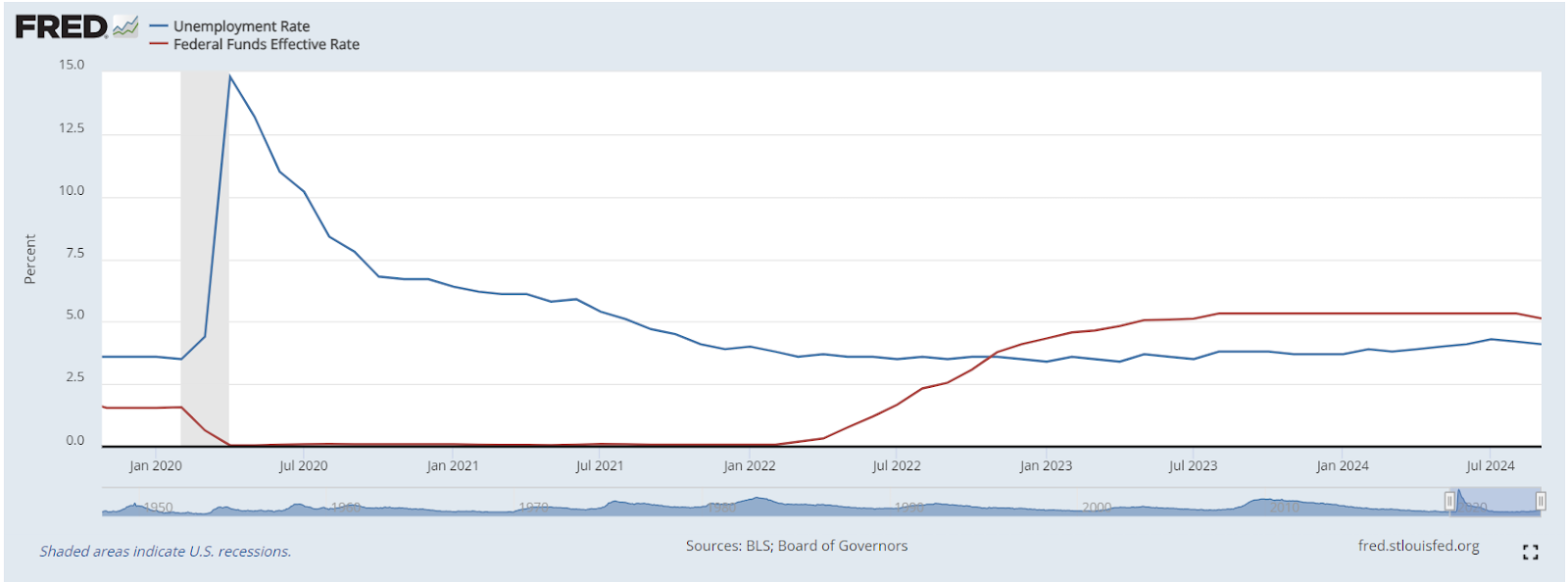

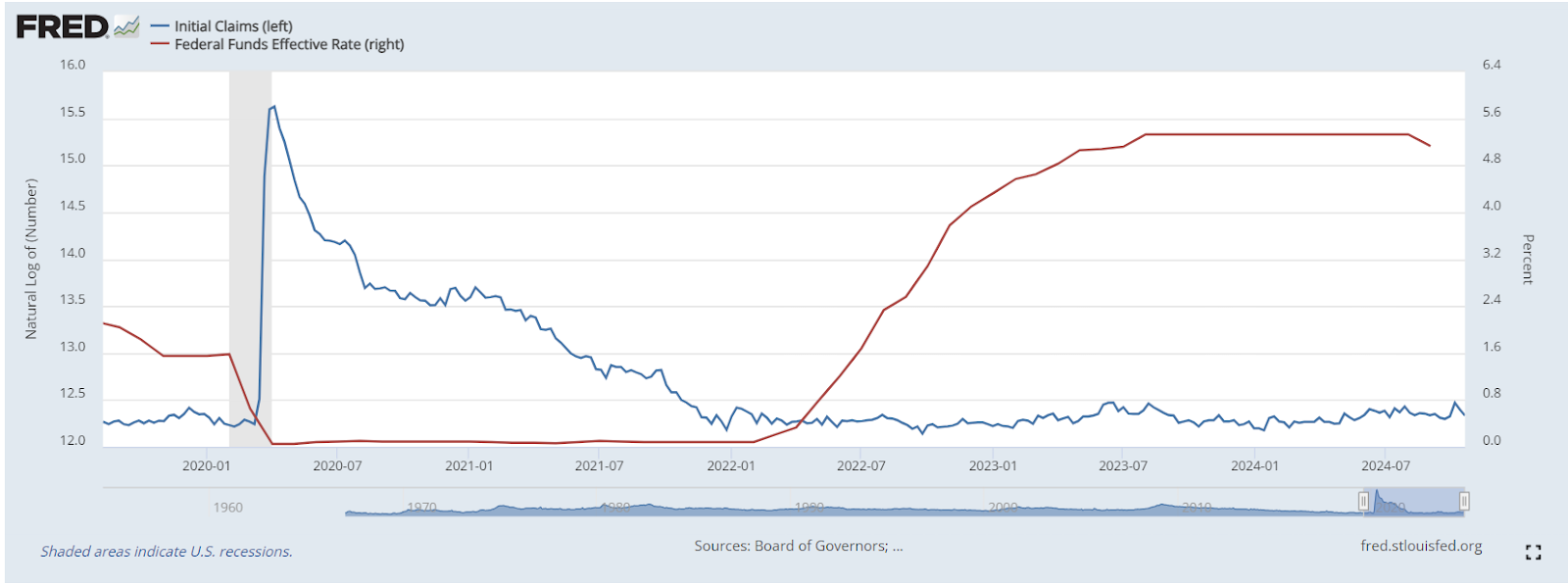

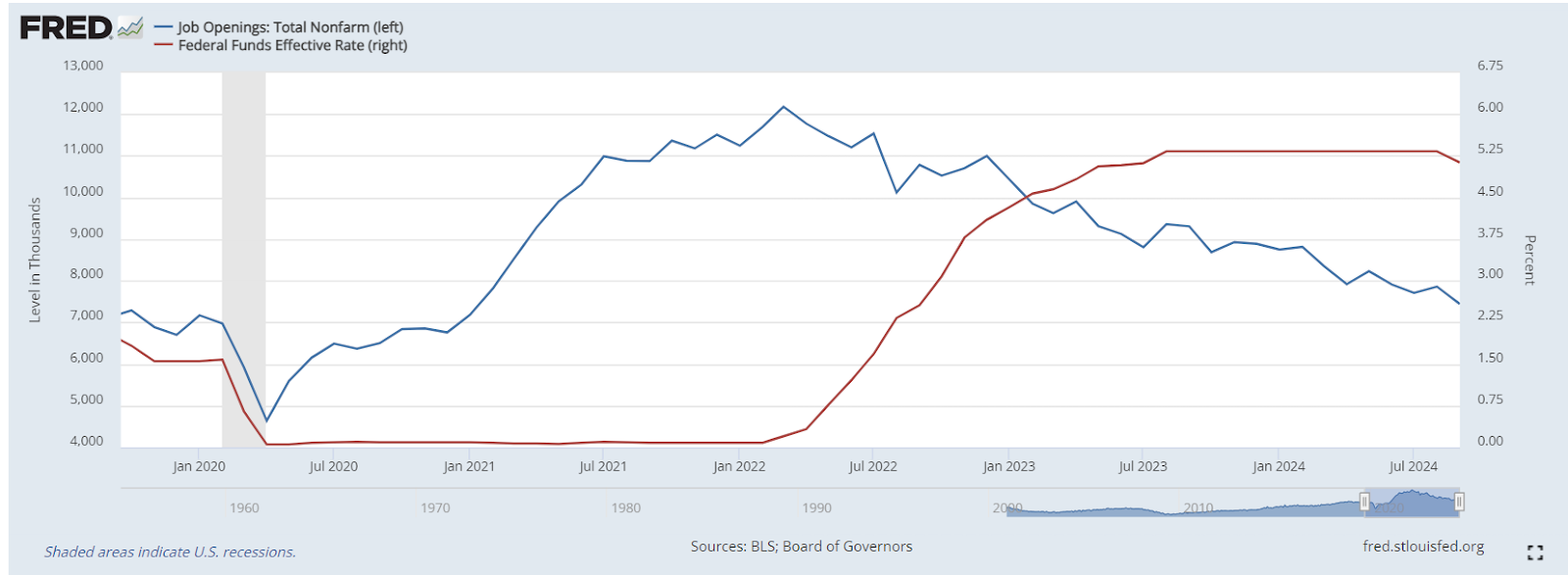

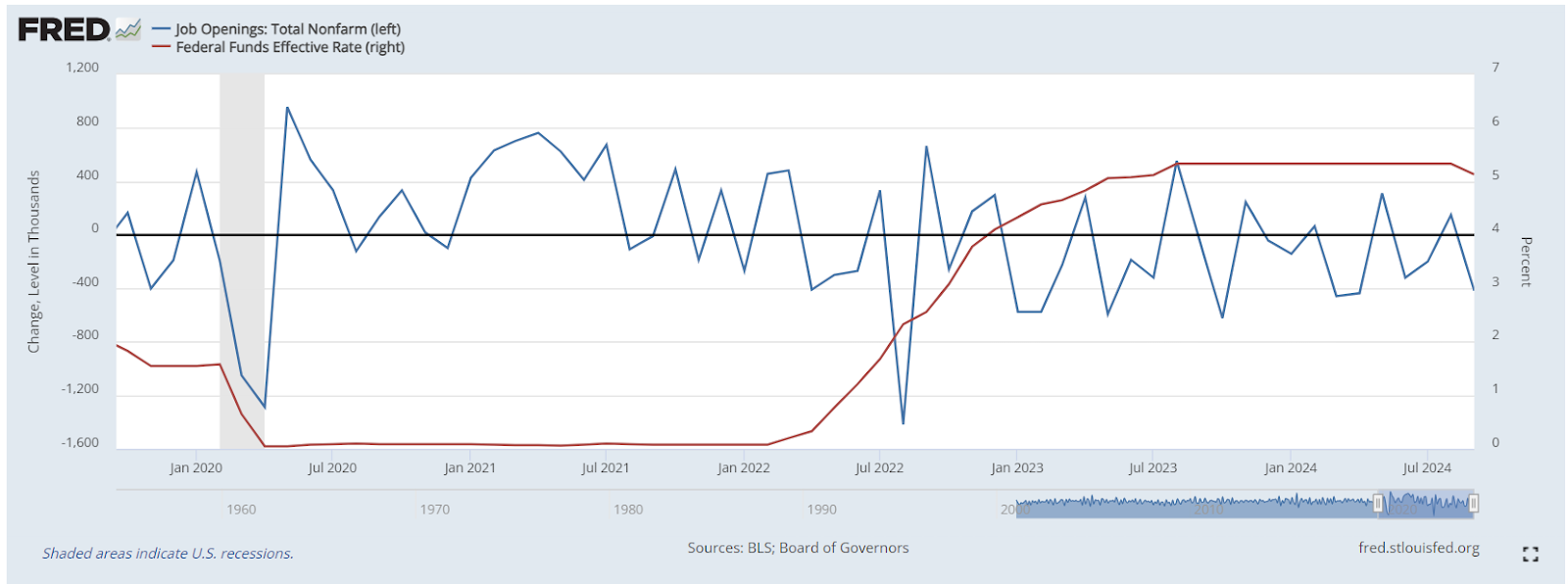

Let’s start with unemployment as the key channel to impact inflation. If the textbook econ 101 model is correct, we should be able to see it in a few different datasets. The unemployment rate (Figure 1) should go up as the Fed began raising rates in March 2022, and should correspond to a rise in initial filings for unemployment insurance (Figure 2) and a fall in job vacancies (Figure 3) and new job creation (Figure 3(a)).

Figure 1: Unemployment rate (blue, left) and effective federal funds rate (red, left) vs. date.

Figure 2: Initial unemployment insurance claims (blue, left) and effective fed funds rate (red, right) vs. date

Only one of those trends is borne out by the data. Job openings have declined, and the monthly change (Figure 3(a)) has been lower recently. It’s worth noting, however, that the number of job openings is still historically high, above anything pre-pandemic. Plus demand destruction requires a decrease in real spending power, which a change in job openings alone won’t do.

Figure 3: Total job openings (blue, left) and effective federal funds rate (red, right) vs. date.

Figure 3(a): Monthly change in job openings (blue, left) and effective fed funds rate (red, right) vs. date.

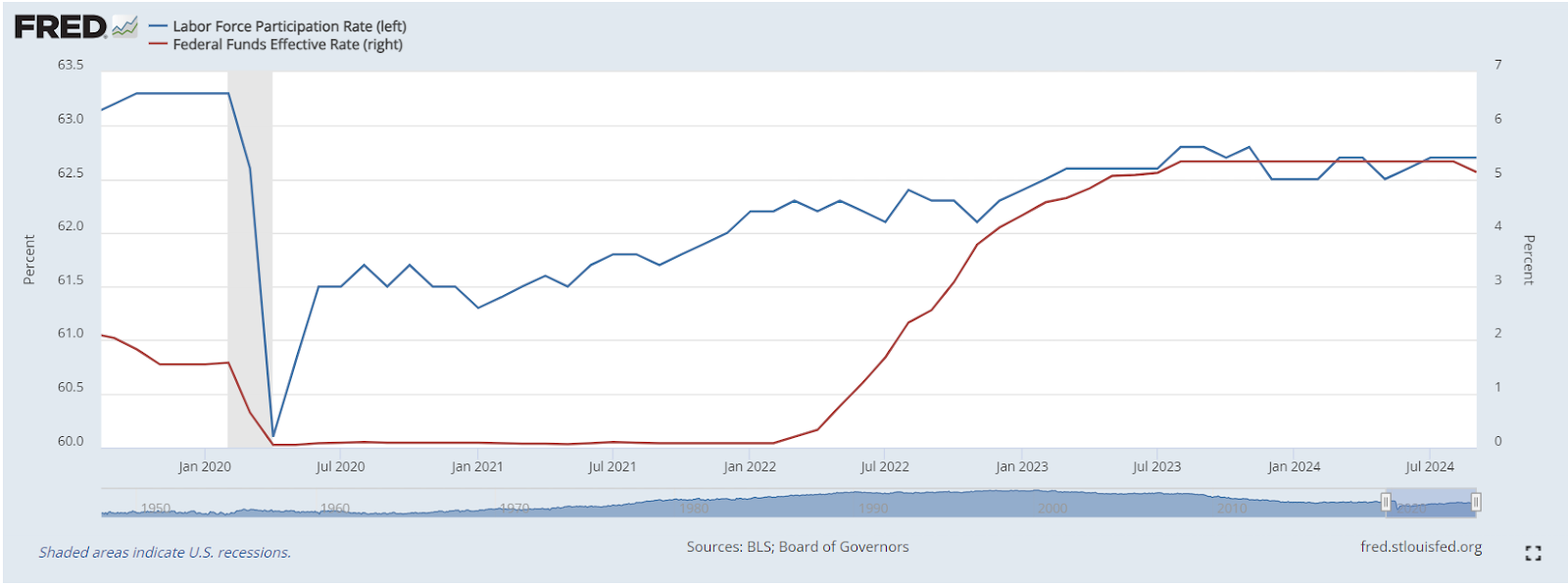

No dice. But maybe what happened is that work prospects got bad and that led a lot of people to exit the labor force entirely. Except that didn’t happen either. The labor force participation rate (Figure 4) has remained below 2019 levels, but reached its post-pandemic relative maximum of 62.8 percent in August 2023, the month at the end of the Fed’s rate hikes, and remained steady since.

Figure 4: Labor force participation rate (blue, left) and effective fed funds rate (red, right) vs. date.

Now let’s expand the intro model a little bit to see if there are factors that could be a viable channel to get from rate hikes to a fall in inflation. When the Fed increases rates, there are a bunch of things that should be expected to happen as a result of higher borrowing costs:

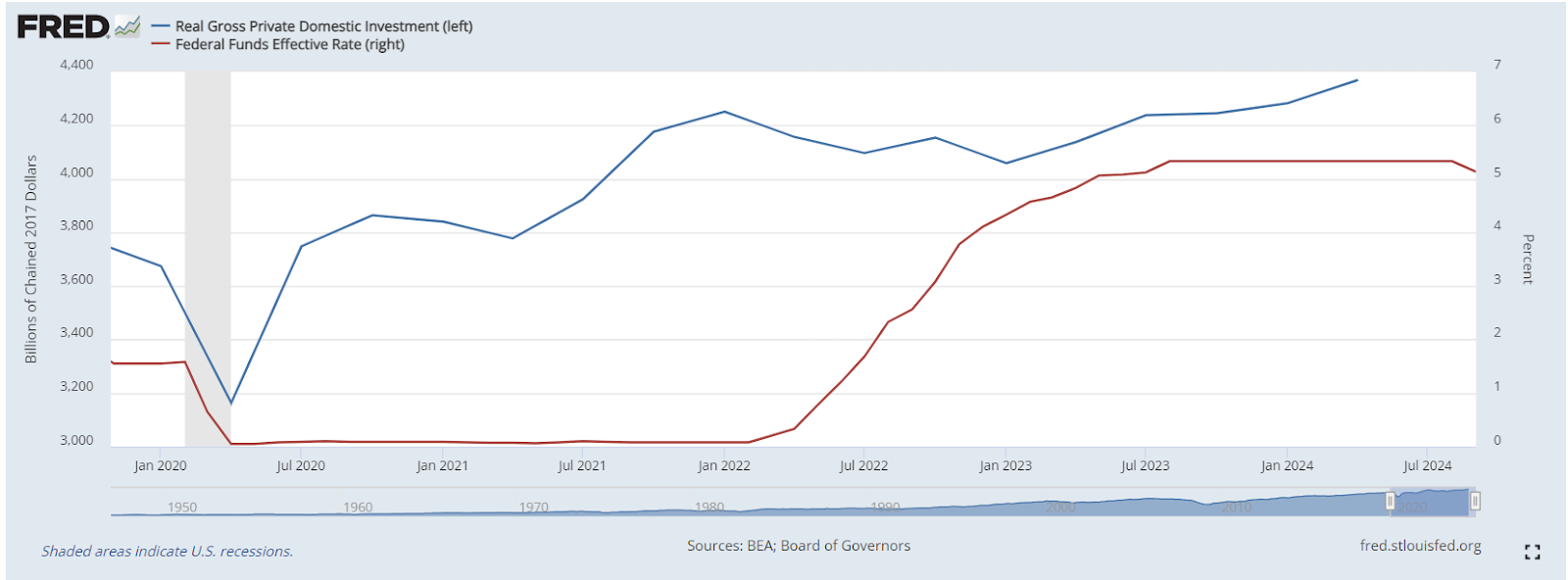

- Private investment (Figure 5) should fall, reflecting firms being unable to afford expanding with less access to credit.

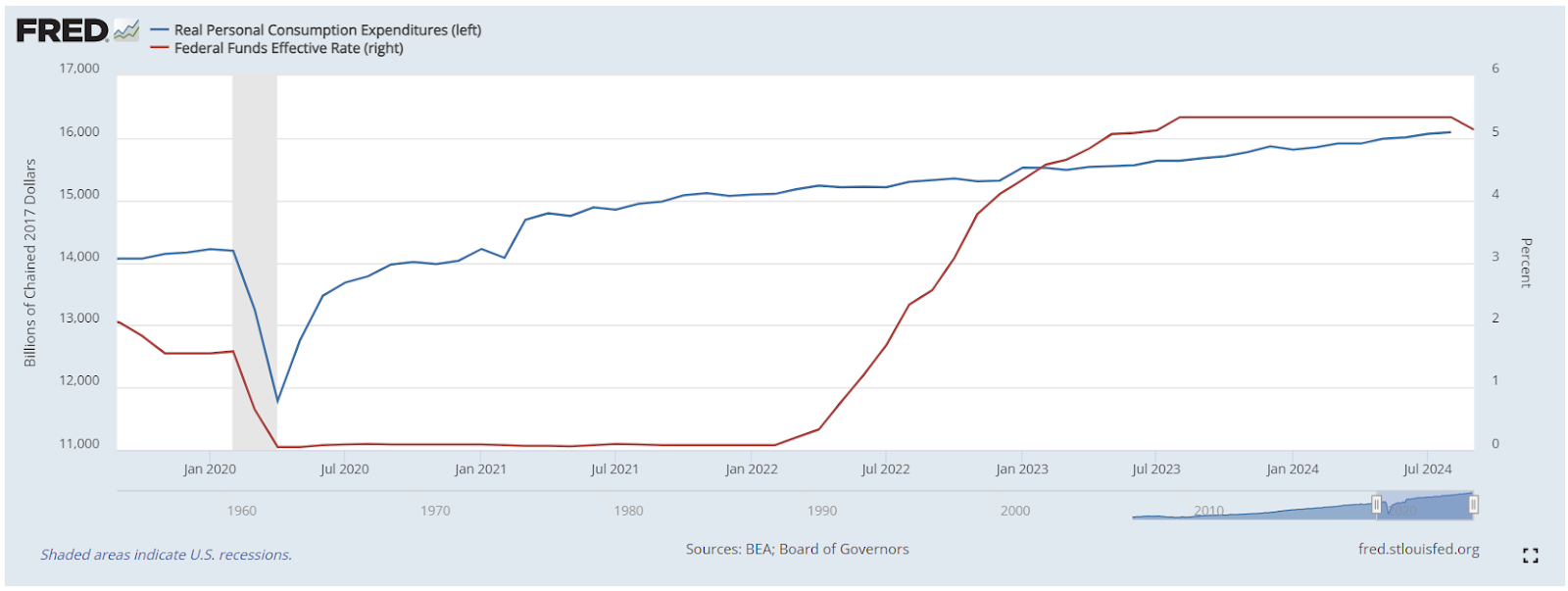

- Consumer expenditures (Figure 6) should fall, reflecting their lines of credit (including personal loans, mortgages, car loans, and credit cards) costing more to use and wage growth slowing.

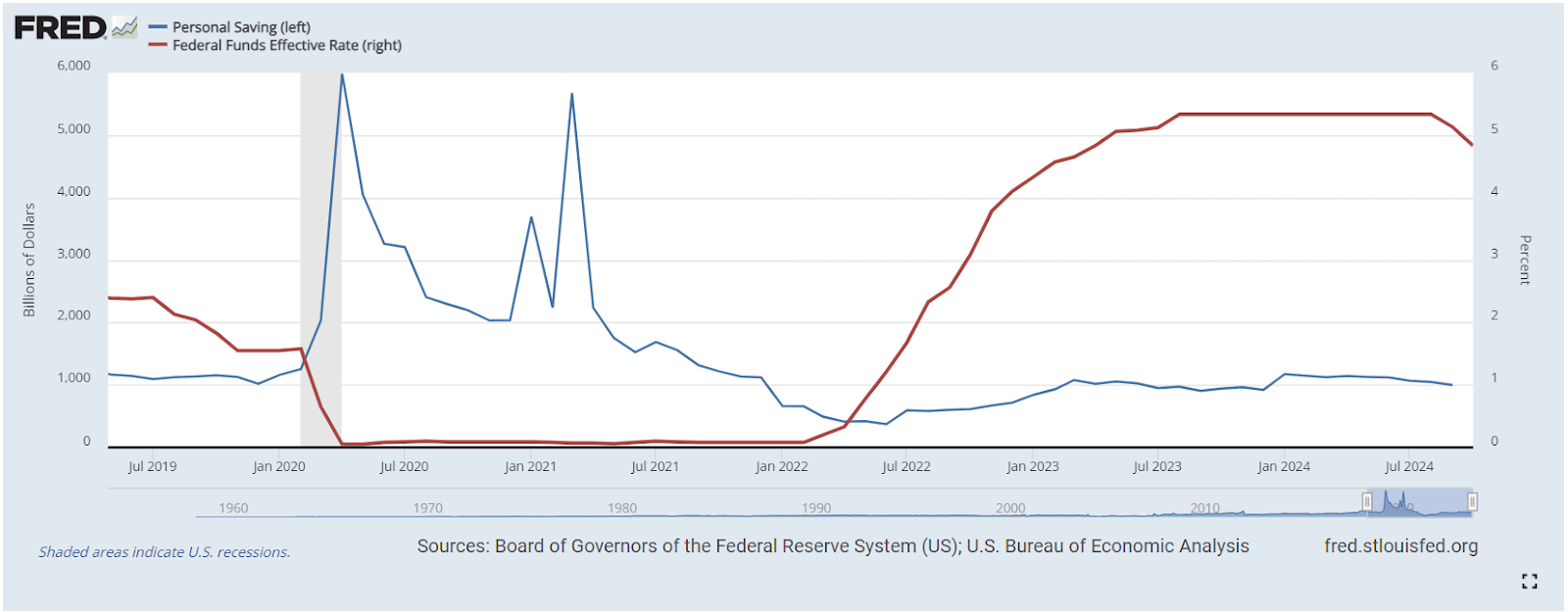

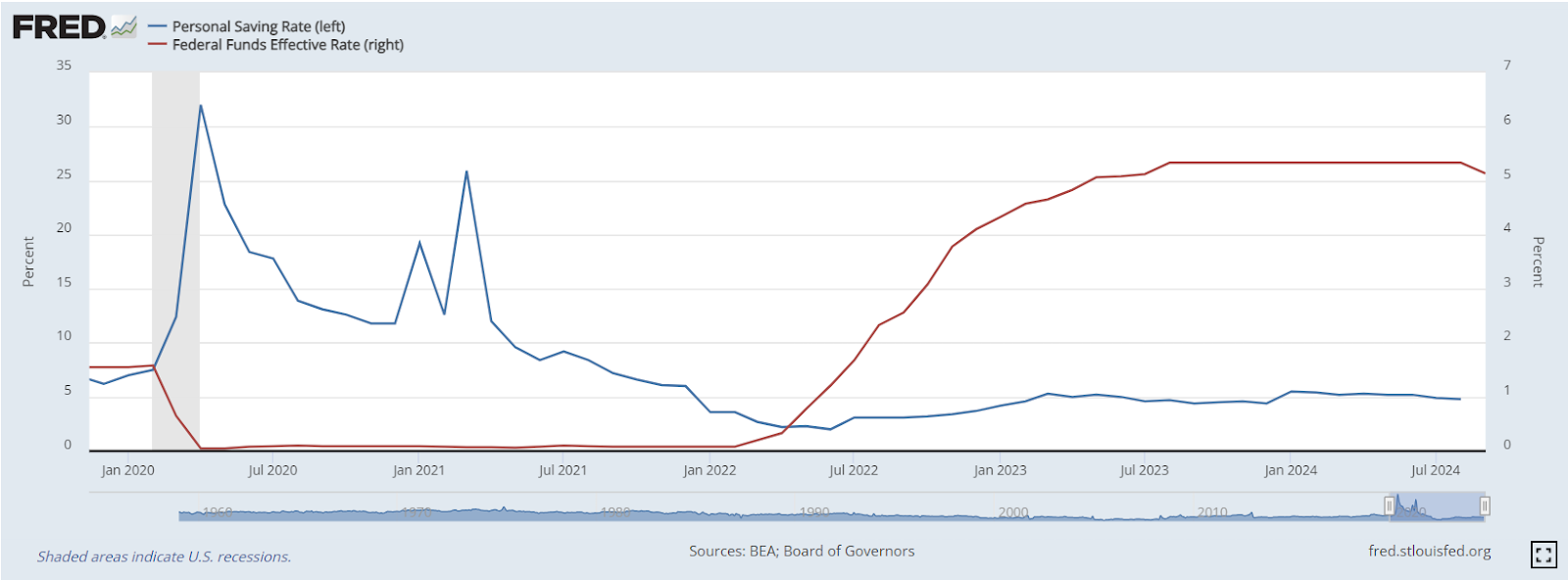

- Personal savings (Figure 7) should decrease as people eat into savings as a substitute for consumer credit. The savings rate (Figure 8) should fall, as more personal income is diverted directly to consumption to cover for using less credit.

Any of these could potentially be a mechanism for monetary policy to lower aggregate demand.

Figure 5: Real gross private investment (blue, left) and effective fed funds (red, right) vs. date.

Figure 6: Real consumption expenditures (blue, left) and effective fed funds rate (red, right) vs. date.

Figure 7: Personal Savings in nominal billions of dollars (blue, left) and effective fed funds rate (red, right) vs. date

Figure 8: Personal savings rate (blue, left) and effective fed funds rate (red, right) vs. date.

Yet exactly none of those causes are reflected in the data. (Total personal savings looks at first glance like it dipped, but it actually increased and stabilized during the course of the rate hikes.) If demand destruction does occur, it would presumably be through some combination of those factors. If there’s no loss of jobs, no drop in investment or consumption, and no change in personal savings rates, how exactly does increasing interest rates lead to lower inflation?

The short answer, at least in this case, is that it probably didn’t. This entire model of monetary policy presupposes demand-side causes of price increases, which were only a minority of the post-Covid inflation.

Inflation Doesn’t Capture the Full Cost of Living

That isn’t to say that the Fed’s rate hikes did nothing to impact workers and consumers. They actually made things worse. One long standing debate from the past couple of years is why public sentiment has remained negative on the economy even as most indicators have been broadly positive. A big part of that sentiment gap can be explained by differences in how lay people and economists use the same word. In an everyday sense, “inflation” means a rise in cost of living. But in economics, “inflation” is a change in the price level of a fixed basket of goods compared across time. That creates tension in how we discuss inflation; it’s atechnical measure that is often used in a general sense.

That meaning gap wouldn’t be a huge issue if the technical measure was a consistently good proxy for how people experience changes in the cost of living. There are prices that are important to the cost of living, however, that are excluded from the basket used to measure inflation. Chief among them is the cost of borrowing.

From a mechanical point of view, excluding interest rates on consumer credit is very reasonable; if they were to be left in, then it would muddle the relationship between interest rates and inflation since inflation would be defined as a function of interest rates. While it makes sense for technical economic analysis, this exclusion makes measures of inflation a poor approximation of the actual situation people experience.

Consumers experience higher interest rates on their access to credit as a sort of inflation. After all, it makes their lives more expensive. As a result, people’s lives can get more costly even in the face of easing inflation. (Not to mention that lower inflation still doesn’t represent a drop in prices.)

Put everything together and you get a story that goes something like this: multiple shocks, mostly, though not entirely, stemming from disruptions to supply usher in a major episode of inflation. As supply constraints eased, inflation fell. Although not before many unscrupulous firms took advantage of the situation by raising prices by more than their costs increased.

Meanwhile, neoliberal economists like Jason Furman and Larry Summers publicly pressured the Fed into hiking rates in an attempt to elevate unemployment and usher in demand destruction. Jerome Powell and the Fed ultimately did so, which made consumer credit more expensive, in turn that kept consumer confidence low because even though inflation was easing, it didn’t feel like it. Through those higher borrowing costs, the Fed has been responsible for eroding consumer confidence, threatening democracy, and slowing the green energy transition.

Yet what the data indicate is that these trends happened in parallel; over similar timeframes but not with a causal relationship between them. The expected changes to unemployment, investment, consumption, and personal saving are all missing. Absent those channels, there isn’t a link that gets from higher interest rates to lower inflation. It’s entirely possible that there is a causal channel somewhere, but until it’s identified and explicated, there is no reason to defer to the econ 101 model.

Particularly given the stink that neoclassical economists made about evidence for sellers’ inflation, they should be held to a similar standard for their crediting of the Fed for lower inflation and implicitly putting the blame on consumers and workers. The data just don’t fit their model.

Economist and New York Times columnist Paul Krugman took to the pages of the gray lady on August 13 to stress the importance of central bank independence. The piece was a response to recent comments from Republican presidential nominee Donald Trump and his running mate JD Vance, both of whom have argued that presidents should have a “say” in the Federal Reserve’s interest rate decisions.

Krugman acknowledged that situations could arise “in which even the executive branch should weigh in on monetary policy.” It would be appropriate, for instance, if “a rogue Fed chair, appointed by a president from the other party, engag[ed] in what amounts to economic sabotage.” Ironically, Krugman overlooked the extent to which his “rogue Fed chair” scenario is currently playing out under Jerome Powell.

On July 31, Powell—a Republican first chosen to lead the Fed by then-President Trump (and reappointed by President Joe Biden in 2022 against the advice of the Revolving Door Project and others)—announced that he was keeping the federal funds rate at a 23-year high for the twelfth consecutive month despite ample evidence of falling inflation coupled with rising unemployment. This is data that Powell is obviously aware of. He even admitted, at his semiannual testimony before Congress on July 9, that “this is no longer an overheated economy” and that “the labor market appears to be fully back in balance.”

Since then, fresh data showing a further increase in unemployment and decrease in inflation have prompted calls from progressive economists and lawmakers for Powell to convene an emergency meeting to cut the benchmark rate before the Federal Open Market Committee’s next scheduled meeting in mid-September. He has so far ignored those calls, and we are left to assume that Krugman approves of Biden’s silence in the face of what looks like economic sabotage from the Fed.

Powell’s intransigent hawkishness looks awfully suspicious, especially after Trump and other Republicans urged the Fed not to reduce rates before the November election lest it help Democrats. But Powell’s refusal to lower rates despite all economic indicators pointing to the need for an immediate cut is not the only time his actions have raised questions about the central bank’s independence. In February, Powell warned on 60 Minutes that the “U.S. federal government is on an unsustainable fiscal path.” As journalist Conor Smyth has observed, “Powell’s comments on the deficit certainly seem to cross the line from apolitical technocratic commentary to intervention in straightforwardly political matters.” It is “odd,” Smyth continued, “to believe the Fed as it currently exists is a model of independent technocracy.”

Financial regulation is another arena where we can question the political independence of Powell’s Fed. While testifying before Congress last month, Powell sneakily revised what it means for a financial regulation to have “broad support.” Powell was discussing Basel III Endgame, a long-suffering proposal to increase capital requirements for about three dozen of the biggest banks in the United States, but his argument presumably applies to other proposed reforms.

On July 10, Powell told the House Financial Services Committee that to satisfy his standard, a modified Basel III proposal must first receive a “good and solid vote” from the Fed’s seven-member board of governors. Apparently, the 4-2 majority vote with which the original proposal passed last summer (there was a vacancy on the board at the time) is not up to snuff. But Powell is not just seeking what sounds like unanimity from the board, which would be ridiculous enough in itself. He also said that for Basel to be finalized, it must receive “broad support among the broader community of commenters on all sides.”

Make no mistake: Powell’s insistence on the need to listen to “all sides” is a demand for deference to Wall Street. The FIRE (finance, insurance, and real estate) sector vociferously opposes stronger regulations and draws on its deep well of economic and political resources to neuter or kill proposed rules that pose real or perceived threats to its bottom line.

By instructing regulators to acquiesce to the big bank CEOs who have led a historically fierce campaign in opposition to the Basel framework, Powell is practically inviting financial industry executives to quash, through negative public feedback, any regulation they don’t like. In the words of former Fed attorney and current business law professor Jeremy Kress, Powell’s attempt to equate “broad support” with investor-class support is “absurd and dangerous.”

The Battle Over Basel

It’s been over a year since the Fed, the Federal Deposit Insurance Corporation (FDIC), and the Office of the Comptroller of the Currency (OCC) jointly requested public comment on their interagency plan to strengthen capital requirements for large banks. If approved, the proposed rule would require banks with total assets of $100 billion or more to increase their capital reserves to shield themselves from potential losses. The goal is to force such institutions to be more self-reliant and less dependent on public bailouts.

The proposal marks the final step in implementing the Basel Committee on Banking Supervision’s framework for increasing the resilience of the financial system, an effort launched in the wake of the 2007-09 economic crisis. That task remains more crucial than ever. As Bloomberg reported recently, the OCC has privately warned that 11 of the 22 major banks it supervises are “insufficient” or “weak” when it comes to managing operational risk. The main architect of U.S. regulators’ draft rule is Fed Vice Chair for Supervision Michael Barr, a Democrat appointed by President Biden in 2022.

In July 2023, Powell joined Barr and the two other Democrats on the board in voting to publish the Basel proposal. Yet Powell also indicated his openness to diluting it. As The American Prospect’s Robert Kuttner explained earlier this year, the Fed chair’s statement “virtually coached industry critics on which holes to poke in the draft rule.”

The banking industry swiftly launched what Better Markets president Dennis Kelleher has called “probably” the most intense fight against a proposed financial rule since the Great Depression. Ironically, this attack began just months after the meltdown of Silicon Valley Bank, Signature Bank, and First Republic Bank—the second-, third-, and fourth-largest bank failures by assets in U.S. history—which was caused in large part by Powell-led deregulation and supervisory missteps.

As Kuttner noted, Basel opponents’ contention that higher capital levels “will reduce lending and be bad for small businesses” is designed to camouflage the fact that stronger requirements “would reduce bank speculative activities and modestly cut into exorbitant bank profits and executive bonuses.”

The American Bankers Association and the Bank Policy Institute—the industry’s most powerful lobbying groups—as well as congressional Republicans have led the offensive against Basel. But not all opposition to the proposal has come from Wall Street and the GOP. In addition to those right-wing forces, a handful of Democratic lawmakers, nonprofit groups aiming to expand access to mortgages, pension funds, and some renewable energy developers are worried about the potential for negative unintended consequences.

By contrast, Americans for Financial Reform (AFR), a progressive advocacy group that supports the proposal issued last year, has debunked pervasive myths about bank capital hikes. As AFR pointed out, the reason why capital cushions are so thin is because banks prefer to lavish their shareholders and executives with dividend bumps, stock buybacks, and bonuses while counting on the public to rescue them in cases of failure (“to privatize their gains and socialize any losses”).

Banks can easily afford to increase the amount of capital they have on hand (at the expense of their bigwigs), and studies show that higher capital levels lead to more—not less—lending. AFR lamented that bank-led fearmongering about the loss of affordable housing in low-income communities of color is one way that Wall Street has convinced some liberals to back its crusade against Basel.

In any case, AFR urged U.S. regulators to “make sure risk weights for home mortgages are appropriately weighted to address any genuine negative impacts.” For his part, Barr made clear that the Fed intended to do so, saying in January 2024: “We want to make sure that the rule supports a vibrant economy, that supports low- and moderate-income communities, that it gets the calibration right on things like mortgages.”

By that point, however, JPMorgan Chase CEO Jamie Dimon had already encouraged his fellow bank executives to go above Barr and appeal directly to Powell to sabotage the Biden administration’s bid to strengthen capital requirements. Following his initial expression of nominal support for the Basel proposal, Powell met with big bank CEOs more than a dozen times, including at least four meetings or calls with Dimon.

The pressure clearly worked. In March 2024, during his previous testimony before Congress, Powell advocated for “broad, material changes” to the current draft. He didn’t rule out a complete overhaul, telling lawmakers that re-proposing a watered-down framework and re-opening the public comment period is a “very plausible option.” Presaging language that he used last month, Powell arguedthat such a move may be required to achieve an outcome that has “broad support at the Fed and in the broader world” (emphasis added), portraying that impossible standard as equivalent to maintaining the U.S. central bank’s political independence.

Historian Peter Conti-Brown slammed Powell’s reasoning. “Throwing away regulatory reforms preferred by the party that won the last national election does not preserve Fed independence,” Conti-Brown wrote. “It makes a mockery of it.” By trying to push the proposed rulemaking into the next presidential administration, he added, Powell is “intervening in a way that Republicans and bankers prefer.” Five months ago, Powell called going back to the drawing board a likely next step. On July 9, he told the Senate Banking Committee that doing so is “essential”—further hindering the existing proposal and proving Conti-Brown’s point.

While the current draft calls for a 16% increase in bank capital, the Fed is reportedly seeking to reduce the planned hike to as low as 5%. According to Kress, that would free up approximately $115 billion for big banks to pay out to their executives and shareholders. No wonder Wall Street doesn’t support the original proposal!

Powell informed members of the Senate last month that the Fed board’s “strongly held view” is that regulators “need to put a revised proposal out for comment for some period” because “that has been our practice” whenever significant changes are made. (He amended his wording when addressing House lawmakers, referring to “the strong view of a number of board members”). The OCC and the FDIC—whose outgoing chair Martin Gruenberg played a key role in advocating for double-digit capital hikes—remain opposed to soliciting more feedback before finalizing a reworked proposal given how rapidly the window for action is closing.

It’s Not Just Basel At Risk

Far from an idiosyncratic effort to reshape the English language, Powell’s bid to recast “broad support” as “bank support” is really a calculated move to give economic elites veto power over new financial regulations—including but not limited to Basel III Endgame.

For one thing, as American Banker reported, Powell told Congress last month that “the Fed does not intend to pursue any other regulatory reform items—such as new long-term debt requirements and liquidity standards—until changes to the capital proposal are agreed upon and put forth to the public.” That’s an effective way to freeze ongoing efforts to improve oversight of the financial industry.

Meanwhile, Wall Street is using the drawn-out fight over bank capital hikes as an opportunity to push for weakening a related rule. At issue is the GSIB surcharge, an extra layer of capital the Fed requires eight global systemically important banks (GSIBs) based in the United States to keep on hand to improve their soundness. Even though the Fed’s 2015 vote adopting the rule was unanimous, it is now mulling potential modifications to how the surcharge is calculated, a move that could save megabanks billions of dollars each year.

Besides higher capital requirements, there are other rulemaking proposals that Powell has worked hard to obstruct. That includes an international bid to require lenders to disclose their plans for meeting greenhouse gas reduction commitments. What’s more, Powell’s Fed has refused to join other federal agencies in proposing long-delayed limits on incentive-based compensation for bank executives, a remuneration model that has historically encouraged excessive risk-taking.

Since becoming Fed chair, Powell has not hesitated to slow-walk many proposed financial regulations. Now, his alt-definition of “broad support” gives him license to postpone their finalization indefinitely.

The Fed Chair, Not The Vice Chair For Supervision, Sets The Regulatory Agenda

With his opposition to more robust financial regulation, Powell is further insulating capital from democratic oversight, as if the judicial dictators on the Supreme Court hadn’t already given the ruling class near-total authority to wreck the lives of working people.

It’s incumbent upon congressional Democrats to use the full extent of their authority to limit the high court’s jurisdiction, as Ryan Cooper has argued in The Prospect. That’s important for so many reasons, including if Basel supporters end up pursuing a public-interest litigation strategy to secure strong capital requirements, such as the one outlined by Kress. In addition, if Democratic presidential nominee Kamala Harris gets the chance to appoint a Fed chair in the future (Powell’s term expires in 2026), she ought to remember how Powell operated and tap someone willing—or better yet, eager—to rein in Wall Street.

Throughout 2021, the Revolving Door Project implored Biden not to reappoint Powell. As we warned, Powell’s time as a partner at the Carlyle Group—a union-busting, fossil fuel-investing private equity firm—signaled his sizable appetite for financial predation. We and other public interest watchdogs argued that whatever merits Powell may have regarding his purported commitment to the Fed’s full employment mandate (a commitment we were right to question in light of the sustained flurry of interest rate hikes he initiated in early 2022), his ethical shortcomings and propensity for deregulation should be disqualifying.

Alas, we were ignored. As a result, numerous proposals to check the power of financial oligarchs are on the cutting-room floor with three months to go before a presidential election that Trump and Vance—corporatists with no intentions of protecting the public from financial speculation or swindling—have a chance to win. If Harris can prevent that from happening, she must nominate a Fed chair who is dedicated to dovish monetary policy and robust financial regulatory policy. Ignoring the latter is a recipe for disaster.

After more than a year of aggressive rate hikes, the Federal Reserve has now held them steady after each of the past two Federal Open Market Committee meetings. After peaking at levels not seen in decades, inflation has leveled off in the three-to-four percent range for months now. On top of that, job openings, and consumption all seem to have slowed notably. All of this adds new context to the debate between proponents and opponents of Fed hawkishness.

When elevated inflation first became a serious concern following macroeconomic shocks—from a global pandemic, huge recession fighting policy, and (later) the Russian invasion of Ukraine—economists and pundits quickly split into two broad camps on what was happening. On the one side, there were those who saw high inflation as a passing issue due to serious disruptions caused by giant exogenous shocks. That group, dubbed “team transitory,” believed that this bout of inflation was not due to overstimulation of the economy. On the other side were those who insisted inflation was being driven by the demand side; they argued that the fiscal stimulus had been too large, and that the job market in the recovery was too strong. That view relied on the idea that prices were responding to elevated demand from excess savings, rather than price shocks in the supply chain or corporate price manipulation.

In retrospect, the evidence shows that team transitory was right (although additional shocks to the macroeconomy kept inflation high longer than most of them predicted). And yet, despite the mounting evidence and the early signs of economic cooling, the Fed has not reversed course. A big part of why is a compulsion to try and get inflation to two percent. But that fixation now poses a serious threat to our economic well being.

Back at the start of this year, I wrote a piece covering the Federal Reserve’s two percent inflation target and why taking it as gospel is misguided. Since then, there has been considerable discussion about whether the target rate should be changed, with the case for abandoning two percent made in The Financial Times last spring by Columbia University’s Adam Tooze. Following that, the FT published a letter to the editor arguing against Tooze’s point, Harvard economist Jason Furman agreed that it was worth reconsidering, and former Treasury Secretary (and sleazy fintech businessman) Larry Summers thoroughly dissented.

As Nobel Laureate Paul Krugman has written, the primary concern about easing the two percent target revolves around nebulous fretting about the credibility of the Fed. As he put it, proponents “fear that if they ease off at, say, 3 percent inflation, markets and the public will wonder whether they will eventually accept 4 percent, then 5 percent and so on.” Such concerns seem rather oblivious to the Fed’s extremely strong (potentially too strong) inflation-fighting strategy. Surely, they’ve built up enough of an inflation hawk reputation that they can take a slight hit. Moreover, despite inflation running slightly high still, financial markets seem at ease with the current level and inflation expectations have remained anchored. All of this makes warnings of a loss of faith in the Fed seem like a bit of a reach.

Before we get into the weeds, it’s worth explaining the origins of the two percent figure. What’s the importance of that specific figure? As I wrote, “the target is more tradition than science.“ The exact figure originated from a television interview with the New Zealand Finance Minister in the 1980s. At the time, New Zealand was experiencing serious inflation, nearly ten percent, and the government wanted to give the central bank a codified target. Since then, two percent as a target has become the norm among rich countries. However, not every central bank that uses it as a baseline clings to it as aggressively as the Fed; a number of them, including the Bank of Canada and the Reserve Bank of Australia, use a more flexible version of the target. In Canada, the target is two percent plus or minus one percent. In Australia, it’s two to three percent. A quick glance shows that such ranges are not at all unusual. Until relatively recently, the Fed’s target was similarly flexible by de facto.

Indeed, the exact figure was only officially adopted by the Fed under then-Chair Ben Bernanke in 2012 (though it had been tacitly endorsed since 1996). In the 1990s, future Fed Chair Janet Yellen was among those who pushed for a higher target rate to allow more discretion on the Fed’s part and guard against deflation.

Additionally, as Krugman has explained, two percent also became typical because it functioned as something of a compromise between economists who wanted absolute price stability (a zero percent inflation target) and those who wanted positive rates to give central banks more room to fight recessions by allowing for a lower real interest rate.

There are arguments about why such a target is good, but practically none of them are specific to two percent. Because inflation measurements tend to skew higher than the true level, it can be important to have a positive target even if the goal is to have functionally no inflation. Certainly, in order to have stable prices, we must have a target that’s relatively low. But that explains why two percent is preferable to, say, ten percent, not why it’s any better than slightly higher inflation. In fact, work by scholars at the University of Massachusetts shows that three to four percent levels don’t constrain growth and can be conducive to stronger economic performance than inflation of two percent.

There is a very good reason, however, why the target needs to be a low positive number. If the target is zero percent or lower, then there is a higher risk of deflation, where people’s money becomes more valuable, which can trigger a recession because the return generated by parking assets deters people and firms from spending and investing, instead opting to sit on their money. This then tanks the “velocity” of money, an econ term for how freely money circulates in the economy; a healthy economy needs money to be moving.

A positive target also allows for monetary policy to better fight recessions. While theoretically possible, banks (including central banks) don’t offer nominal negative interest rates. If they were to, no one would keep their money there (which in turn means they wouldn’t really be impacted by rate changes) unless they were forced to. What central banks can do is create negative real interest rates, but only if inflation is more than zero. (Real interest rates are equal to nominal rates minus the inflation rate.)

On the other hand, there are reasons why holding on tightly to two percent is bad policy. To start, it commits the Fed to prioritizing aggressive inflation fighting over the other half of its mandate: maintaining full employment. Committing to such a low target and refusing to reevaluate is a promise to sacrifice jobs in order to reach such a low level of inflation. Particularly given that there is no strong empirical evidence that two percent is hugely preferable to three or four percent, there is no reason for the Fed to be creating conflict between its dual mandates that otherwise need not exist. This is further exacerbated by the de-linking of employment and inflation captured in the Phillips Curve. In the United States, the relationship simply does not hold. As a result, higher rates from the Fed can force investment and employment down, but without making a dent in inflation.

The obvious counter to such an argument is that the rate hikes haven’t triggered a recession, spiked unemployment, or seriously undermined investment. To the extent that this is true, that can, in itself, be a reason to stop relying on high interest rates to lower inflation; employment is the mechanism by which rate hikes would be expected to influence inflation. The fact that inflation fell without a recession or mass unemployment clearly demonstrates that keeping rates high in pursuit of a two percent target is misguided.

Remember, also, that when the rate hikes started the economy was very strong. And new job openings have fallen since then. Given the significant lag between rate changes and observable macroeconomic adjustments, it’s entirely possible that we are heading in that direction and it’s just taking a while. Regardless, maintaining high rates that risk undermining the labor market and the broader economy still isn’t worth it when it isn’t achieving any meaningful policy goals.

Additionally, given the trend of Secular Stagnation, there’s reason to believe that slightly higher inflation is necessary in order to fight future recessions without hitting the zero lower bound. In an economy with secular stagnation, negative real interest rates become more important because nominal interest rates will stay low most of the time to encourage investment rather than savings. Ironically, this theory was popularized by Larry Summers, who is now one of the champions of inane defenses of central banking as usual.

And, as Adam Tooze pointed out, higher interest rates being deployed to push inflation down can also stress banks and depress developing economies. The Fed’s elevated interest rates create a higher cost of borrowing, undermining banks’ ability to cover any current shortfalls. As the mantra goes, banks borrow short and lend long. All fixed-rate loans that they made before the rate hikes can be locked into a lower rate than the bank can borrow at, meaning they lose more in interest payments than they earn. And if there’s a bank collapse, that can easily spark a financial crisis and lead to a recession.

Developing countries, meanwhile, are going to get loans on much worse terms—that might be difficult to pay off—while rates are high. That in turn could undermine their ability to build out infrastructure and new industries, causing lost income. In all, this means gains from global trade will be lower than they could be, keeping poverty, underdevelopment, and global inequality worse than they might otherwise be.

So why is the Fed’s credibility, rather than resting on good policy, tied intimately to a target of two percent? Former investment banker Stephen King wrote in response to Tooze, “choosing to raise targets when inflation has persistently surprised on the upside smacks of no more than short-run political opportunism.” Similarly, Summers wrote that:

…the chairman needs to respond explicitly or implicitly to the growing chorus suggesting that the Fed should adjust its inflation target. For years, the Fed has been firm in its commitment to 2 percent. Of course, there are legitimate academic arguments about the merits of having a numerical target and, if so, what it should be. But timing and context are crucial.

But their argument runs counter to what is supposed to be the bedrock of Fed credibility: a commitment to following the data. Although both King and Summers concede that there are good academic arguments for changing the target, they argue that now is not the time. But the opposite is true—changing the target now is ideal because it would epitomize the Fed’s commitment to following the evidence and maintaining its dual mandate. All of the best available evidence shows that monetary policy cannot possibly be responsible for disinflation. The only theoretical mechanism for it to have done so would be via the employment rate, which remains strong.

To continue to obsess over two percent simply commits Powell to a course of action that will betray half of the Fed’s mandate and runs counter to the best evidence available. No one seriously advocating a change is calling for a hairpin U-turn. Indeed, they can even follow Furman’s step-by-step guide on how to properly change course.

Additionally, there are reasons why abandoning or altering the two percent target very soon is appropriate, beyond the general issues outlined above. For one, the harm of a recession right now would likely be worse for ordinary people because of the extremely high interest rates. If a recession were to begin before the Fed starts lowering rates, then the job loss and decreased economic mobility that comes with it would also be paired with a very high cost to borrow. That means that people who don’t have significant savings and lose their jobs will find it more costly to use credit cards, personal loans, or home equity to fill the gap until they find work.

On top of that the high interest rates are a barrier to people buying houses, which has multiple downstream impacts. To start, it has locked many out of using a home to build equity, which is one of the biggest forms of wealth building in the American economy (and eliminates one possible form of borrowing for a lot of folks). It also forces more people to live in rental properties, which see rent increases because of additional demand (plus rent is already high because of residential price fixing). To round things out, it hurts people who already have homes as well. High rates can make it prohibitively expensive for people with houses they own to move, even if they would have more opportunities somewhere else. Between getting less money from selling their home and extreme mortgage interest rates, moving would probably mean either lowering their standard of living or becoming a renter, unless they moved to somewhere with a much lower cost of living.

The Fed has even seemingly acknowledged that the target is less than ideal; they frame the target as a long term average of two percent inflation. But that doesn’t actually increase flexibility because it only enables them to ease inflation fighting in the present to the extent that they’re confident that inflation will be below two percent in the future to average things out. A much better and simpler solution would be to revise the target upwards to three percent or create a range of two percent plus or minus one percent, either of which would no longer call for elevated interest rates and both of which have international precedents.

When Paul Volcker’s war on inflation ended not quite half a century ago, the inflation level was still four percent. And the following Reagan years are remembered for a robust economy featuring a historic presidential re-election. The hyperfixation on getting down to two percent accomplishes little—well, unless returning Trump to office is one of Powell’s goals—and risks a whole lot. It exposes banks to huge interest rate risk, makes it harder for developing countries to build themselves up, limits housing options, makes people more vulnerable if a recession does come, and creates an ever-present threat of causing mass unemployment or major cuts to economic investment. Meanwhile, virtually all of the good parts of the target will still apply—some even more so—with a slightly higher or more flexible target.

Dylan Gyauch-Lewis is a researcher at the Revolving Door Project.