The FTC is seeking a preliminary injunction to prevent two of the country’s largest supermarket chains, Kroger and Albertsons, from merging. The case was heard in the U.S. District Court for the District of Oregon, where U.S. District Judge Adrienne Nelson, a former Oregon Supreme Court justice, will soon render a verdict.

The merger would make Kroger-Albertsons the second largest retail store after Walmart. The FTC alleges that, in hundreds of local grocery and labor markets, the merger increases Kroger’s market share to a degree sufficient to activate the structural presumption against the merger. Kroger, unsurprisingly, has advanced various standard arguments in favor of mergers: that it is necessary to compete with even larger retailers (in this case, Walmart), will result in lower prices for consumers, and that any anticompetitive harm would be offset by the divestiture plan built into the merger.

As an initial matter, it is unclear whether the central mission of the Sherman Act—to promote healthy competition—is compatible with Kroger’s argument that the merger is necessary to compete with Walmart. While it is undoubtedly true that Walmart is a corporate behemoth whose very existence is an existential threat to competition, it hardly follows that allowing a merger that creates a second behemoth is the best way to reign in the first. Indeed, it is hard to imagine that the drafters of the Sherman Act could even comprehend a corporation as large as Walmart in the first place—and even if they could, it is hard to imagine that they would accept a second, equally large corporation as a legitimate solution.

Kroger’s Defenses Are Unavailing

Putting this aside for a moment though, it is worth taking a closer look at some of the arguments Kroger-Albertsons have advanced to support the merger. First, Kroger has tried to portray Albertsons as a failing firm. Yet testimony has established that Albertsons is not a failing or flailing firm—and in fact, is far from it. Albertsons CEO Vivek Sankaran, testifying in front of Congress in 2022, stated that the firm is in “excellent financial condition” with “more than sufficient resources to continue” with their current plan. Albertsons has admitted that, if the merger does not go through, they have no plans to close any stores. In FY 2023 securities filings, Albertsons told investors that it was “pleased” with their reported $1.3 billion net income. Albertsons COO Susan Morris has also testified that the company is still on track to achieve its savings goals whether or not the merger goes through. What then explains Albertsons leadership’s eagerness to merge? The answer is hardly surprising—their executives have testified that their private equity backers stand to gain tens of millions of dollars in parachute payments should the merger be approved.

Second, Kroger argues that the merger would not produce anticompetitive effects due to the divestiture plan built into the acquisition. The plan is to sell hundreds of stores in overlapping grocery markets to C&S, a wholesale grocer, which, according to Kroger, would mitigate any anticompetitive harm. As the FTC has repeatedly pointed out throughout the trial, there are more than a few reasons to be suspicious of this argument.

The Court should be skeptical of this remedy, as every party in this transaction has a failing record of making divestiture work. For example, in Albertsons’ 2015 acquisition of Safeway, 146 stores were divested to Haggen. Haggen filed bankruptcy within months, and shortly thereafter, Albertsons reacquired 54 of the stores it had previously sold. This is not the only reason for skepticism. As was revealed at trial, Alona Florenz (C&S Senior VP of corporate development and financial planning), writing to a Bain consultant, stated “just be careful with FTC. We want to say we can run them.” It doesn’t take a genius to read the subtext—C&S wants to say that they can run the stores so that, after the merger is approved, they can turn around and gut them for profit.

This interpretation is further supported by the economic realities inherent in the divestiture plan. C&S is primarily a wholesale grocer, meaning that its primary mode of business is selling in bulk to grocers, not operating stores that sell groceries to consumers. It is extremely unlikely that C&S has the infrastructure or know-how to successfully operate hundreds of grocery stores across the country that are acquired simultaneously. Further, it was revealed during discovery that C&S officials themselves believe that they are buying Kroger’s worst stores. Not only have they been caught saying the quiet part out loud, the price that C&S would pay is itself revealing: the deal is priced close to the value of the real estate alone, suggesting that C&S could easily sell off the stores for close to what it paid.

You may be thinking: even if C&S doesn’t stand to lose much on the deal, what’s in it for them? Fortunately, one need not look far for an answer. When Price Chopper and Tops, (two grocery stores) merged, C&S acquired certain stores as part of the divestiture plan. As they have done here, C&S was happy to tell the FTC that they planned to use the newly acquired stores to robustly compete with the newly merged firm. But what actually happened? C&S operated some of the stores at a loss while using others as leverage to increase profits in its wholesale business—its primary money-maker. They sold many of the recently acquired stores to their wholesale customers, who, in return, extended their lucrative contracts with C&S.

As further evidence of C&S’s true intentions, the acquisition price of the divested stores is essentially equal to the value of the real estate alone. And in a previous merger, after telling the Court that they would use stores acquired in a divestiture plan to compete with the merged firm, they turned around and sold enough stores to ensure that their wholesale profits, their primary source of revenue, would eclipse the losses from the self-proclaimed dud firms they acquired and retained. What possible reason would Judge Nelson have to believe that this would go any differently? And to top it off, even if the divestiture plan went exactly as Kroger and C&S say it would, it would fail to cure the anticompetitive harm in hundreds of local markets across the country.

Beware of Dynamic Pricing

Beyond the inadequacy of the divestiture plan, the FTC has raised other concerns that may be even more serious—especially for consumers. In 2018, Kroger began rolling out “digital price tags,” which allow the company to change retail prices in real time. Several lawmakers have expressed concern that these digital price tags could be used to facilitate dynamic pricing, whereby the price charged depends on the identity of the consumer making the purchase. The digital price tags come equipped with cameras, which use the vast amounts of data to which Kroger has access to change the price of an item depending on who the camera sees looking at the shelf. If the merger were to go through, Kroger would acquire all Albertsons’ data about their consumers, which would greatly increase the efficiency with which Kroger can price discriminate.

Kroger, of course, has steadfastly denied that the new technology will be used to raise prices. These denials are a staple of merger cases—firms poised to merge have consistently argued that they won’t raise prices, and far too often, courts have been content to take them at their word. Here, should the merger go through, Kroger has promised to invest $1 billion to keep prices low. Government attorneys correctly pointed out that, not only are these promises completely unenforceable, but history has shown that they are utterly meaningless, as post-merger firms have consistently broken these promises without consequence. Corporations such as Kroger have a fiduciary duty to their shareholders, not to their customers. If they see opportunities to raise profits, this duty requires them to pursue it—consumers be damned. Beyond history, Kroger itself has proven to be untrustworthy—in the course of these proceedings, they were forced to admit that they had engaged in price gouging on consumer staples such as milk and eggs in the midst of the Covid-19 pandemic.

Worker Welfare Matters Too

Beyond hurting consumers, the merger also harms employees. Kroger and Albertsons currently employ around 710,000 people across about 5,000 stores nationwide. Currently, unions can bargain separately with Kroger and Albertsons, and thus have greater leverage to advocate for increased wages and other protections for their workers. Should the merger go through, unions will lose this critical leverage, and would again be subjected to the whims of Kroger’s leadership. Kroger’s attorney, the aptly named Matthew Wolf, told Judge Nelson that “[Kroger] will preserve the unions.” As with his promise that the merger would lead to lower prices, taking Mr. Wolf at his word would be no wiser than taking the word of an actual wolf who tells the farmer that he will diligently guard the hen house.

Judge Nelson should grant the FTC’s preliminary injunction blocking the merger between Kroger and Albertsons. Albertsons is a healthy firm whose presence in the market is essential to competition, and their desire to merge is motivated by the fact that their executives stand to make tens of millions of dollars should it be consummated. The divestiture plan, even if it plays out exactly as Kroger says it would, is inadequate to mitigate the anticompetitive harm that would result from the merger. C&S, the acquirer, has openly stated that it is taking on Kroger’s worst firms, has a strong economic incentive to pawn off the newly acquired firms to secure greater profits in its primary revenue source as a wholesaler, and has a known track record of doing exactly that. The acquisition, which would include all of Albertsons’ consumer data, would allow Kroger to exponentially increase the sophistication and efficiency of their dynamic pricing regime. And, after admitting to price gouging amidst a global pandemic, Kroger offers nothing more than its legally unenforceable word that it won’t use the immense increase in market share to raise prices or harm workers. This merger will harm competition, consumers, and workers. The Court should reject it.

Corey Lipton is in his final year of the JD/MPP program at the University of Michigan.

Last month, Capital One announced that it plans to purchase Discover in a deal worth $35.3 billion. For their campaign to secure regulatory approval, Capital One is trying to act like a benevolent pro-consumer company that will use economies of scale to lower interest rates and ramp up competition with Visa and Mastercard. But that’s probably baloney.

There’s something missing in the conversation around this merger–namely, along what axis competition among card issuers actually happens. Most coverage seems to assume that everything can be grouped into “costs for consumers,” but that’s not the case. To really get at what the deal’s competitive effects would be, we need to understand what kinds of companies Capital One and Discover are, the industries in which they operate, and what competition in those spaces looks like.

Subprime Borrowers Are Likely to Be Injured

There’s a lot of uncertainty about how regulators will handle this deal. For one, there are a lot of different agencies involved in overseeing credit card competition. In order to go anywhere, the merger first requires sign off by both the Office of the Comptroller of the Currency (OCC) and the Federal Reserve Board (Fed). This is because Capital One is a nationally chartered bank, making the OCC its primary regulator, while Discover is regulated primarily as a bank holding company, which is the Fed’s ambit. To add more acronyms, the Federal Deposit Insurance Corporation (FDIC), while not primarily involved in the merger approval, could play an advisory role, especially since it is the primary regulator of Discover Bank, which is owned by Discover. Similarly, the Consumer Financial Protection Bureau (CFPB) could flag issues with the merger as it serves as a secondary regulator for all large financial institutions. Finally, the Department of Justice (DOJ) could review the merger under the antitrust laws.

While the OCC, Fed, and FDIC have all dragged their feet in updating merger guidelines and have a history of rubber-stamping bank consolidation, the CFPB and DOJ are significant hurdles. The CFPB’s Rohit Chopra and DOJ’s Jonathan Kanter are both ardent anti-monopolists. Under Chopra, the CFPB has been aggressive in reining in the worst abuses from financial services companies. Kanter, for his part, has also implied a willingness to take on bank mergers that other regulators approved. The DOJ also has a bit more latitude to flex its muscles with financial network mergers than when two traditional banks merge.

The most obvious merger harm, on which the DOJ will focus like a laser, is whether the merger will allow the combined firm to raise interest rates on cardholders. Capital One and Discover both cater to subprime (credit score in the 600s) borrowers. And there is less competition for subprime borrowers, which is part of why Capital One was a successful upstart in the credit card industry to begin with. Given that subprime borrowers already have the most limited options in where they can get credit, and given that these cardholders likely shop for credit cards based on which offers the lowest interest rate, it follows that the merger could cause significant harm to an especially at-risk consumer base. The DOJ should define a market (or submarket) for subprime cardholders.

Even for those cardholders with higher credit scores who may not consider interest rates while selecting a card, card issuers do compete on rewards programs, security measures, annual fees, and other features. The merger could eliminate competition between Capital One and Discover on those dimensions as well.

Be Skeptical of Purported Benefits to Merchants

In addition to the horizontal competition mentioned above, Capital One will also gain Discover’s payment processing network, which constitutes vertical integration. As a result, the merged firm will simultaneously hold more market share in credit card issuing, becoming the single largest firm in the space, while also operating a payment network. The deal would, unequivocally, decrease competition in the card issuer space, where just ten firms dominate the industry. But what will happen on the payment processing side is less clear. Capital One argues this aspect of the deal will enhance competition. But for whom?

Card processing is a space dominated by just two firms: Visa and Mastercard. Far, far, far below them, American Express (AMEX) and Discover operate around the edges of that duopoly. As of the end of 2022, Visa and Mastercard’s networks process about 84 percent of all cards in circulation, 76 percent of the total purchase volume, and hold 69 percent of the total outstanding balance across all credit card networks. Capital One’s best case for the merger being procompetitive is that it can become a viable third competitor to those two card processing behemoths. On its face, this seems like a reasonable point, but the mechanics of how it might work are rather fuzzy.

If and when Capital One moves their cards onto the Discover network fully, they will no longer have to pay processing fees to Visa and Mastercard. (It turns out that Capital One represents a much larger share of the total cards of the Mastercard payment processing network). No longer having to pay for those fees is the headline cost saving measure in the deal, but there are potentially others. The merged company may be able to leverage economies of scale to reduce marketing, administrative, or customer service costs as well. So the merged firm may be able to reduce merchant swipe fees or interest rates for cardholders because of those savings. But would they? It’s hard to see a good reason for them to, absent some kind of binding obligation.

Perhaps the merged firm would want to compete more aggressively against Visa and Mastercard for merchants. But cutting merchant fees seems like a pretty naive reading of how credit card purchases work. Discover is already accepted at the overwhelming majority of American retailers. Because most merchants will accept Visa, Mastercard, Discover, and AMEX in the status quo, it’s difficult to picture the merged firm providing a deal so sweet that merchants would proactively encourage using cards on the Discover network over others, especially given the potential risk of losing customers who hold other cards. The merged firm would have to offer exceptionally low fees to entice merchants to proactively discourage using other card networks. Maybe they can get some merchants to offer a small discount for using cards on their network, but to accomplish that at a scale necessary to dent Visa’s and Mastercard’s omnipresence is difficult to imagine.

But there’s also a sneaky reason to expect that the merger might result in some higher merchant fees. As the American Economic Liberties Project’s Shahid Naeem said, the proposed deal is “an end-run around the Durbin Amendment and will raise fees for American businesses and consumers.” The Durbin Amendment is a component of the Dodd-Frank Act that caps transactions on debit card transaction fees, which merchants pay to the debit card issuers, at $0.21. However there are two built-in exceptions; (1) for debit issuers with less than $10 million in assets; and (2) as Marc Rubenstein pointed out, for Discover, by name. And Capital One has been clear that they want to move all their debit cards over to Discover’s network, which could make all Capital One debit cards eligible for higher fees to merchants.

Moreover, we already have a case study of how a single firm acting as issuer and processor might pan out: American Express already operates as a vertically integrated card issuer-payment processor, and AMEX charges higher merchant fees than Visa or Mastercard. So we shouldn’t expect vertical integration to automatically result in reduced merchant fees.

Be Skeptical of Purported Benefits to Cardholders

Likewise the merged firm could pass along any savings from avoided processing fees to cardholders in the form of lower interest rates. But there’s not much reason to expect that either: Recall that the horizontal aspect of the merger places upward pressure on rates for subprime customers. Any efficiencies flowing from reduced processing costs would have to overcome that upward price pressure.

The issue with any arguments about passing savings from processing costs onto cardholders is that they misunderstand the mechanism by which interest rates are set. Interest rates, both on credit cards and other types of loans, are primarily a function of the cost of borrowing at a given time (the “Prime rate”) plus a markup (the “APR margin”). The cost of borrowing is largely dependent on where the Fed sets interest rates. Hence, processing costs do not tend to enter the pricing calculus for annual credit card interest rates (which are invariant to the number of transactions). Further, a recent report from the CFPB shows that larger card issuers charge 8-10 percent higher interest rates than smaller credit card issuers, suggesting that cost efficiency actually results in higher interest rates for cardholders, not lower. The base interest rate controlled by the Fed is exogenous to all of this; the only question is how much of a premium the lender will charge.

Based on that finding, there are a couple of reasons why the merged firm would be likely to keep premiums over the Fed rates (and hence credit card interest rates) generally high, rather than pass savings on to consumers. To start, the emphasis on subprime lending creates more reason for higher markups; subprime borrowers are considered riskier, so they usually have to pay more to borrow to cover the increased odds of missing repayment. Additionally, because subprime lenders have more limited choices and because that’s the market segment Discover and Capital One both target, the merged firm’s share of subprime credit card issuing will likely require less competition than prime credit card issuing, allowing them to offer worse borrowing terms.

Be Skeptical of Other Purported Merger Benefits

Capital One further claims that the merger would make the combined firm a more potent competitor to Visa and Mastercard, potentially causing the two behemoths to reduce their own merchant fees. But this dynamic is frustrated for three reasons: built-in advantages to Visa’s and Mastercard’s business models, friction in transferring cards onto the Discover network, and disproportionate impacts on Mastercard and Visa that might actually leave only one dominant card processor.

First, Visa and Mastercard partner with lots (like lots and lots) of financial institutions rather than issuing their own cards. And that could give them a lot of advantages over Capital One/Discover. For one thing, people shop around for credit cards to varying extents. Some people look for cards with no annual fees, others make selections based off of perks like airline miles, and some people just get credit cards from the institutions they frequent. Where Mastercard and Visa really get a lot of their strength is from the partner institutions that issue the cards on their networks. This includes consumer-facing banks, credit unions, and financial institutions as well as retailers. And that comes with a lot of in-built advantages. For a start, it allows Visa and Mastercard to share responsibility on offerings like customer service with the issuer. If you go to your credit union and get their Visa credit card, you don’t need to direct every question you have to a Visa call center; many times you can call your credit union and they can answer your questions. That is both convenient and it can foster a larger degree of trust in the card, especially when the issuer is something like a credit union or local bank with whom depositors have a long history.

But there’s another, possibly even stronger, advantage to the Visa/Mastercard model–people can get cards with brand-specific rewards. Imagine you’re a contractor who buys a lot of supplies from Home Depot. The idea of a card that rewards you specifically for spending money at Home Depot could be very tempting, especially because you can often apply for it on your phone right in the store. Or if you shop at Costco, you might get a Costco card. If you travel, maybe you’d like a Southwest or American Airlines rewards card. You can get a Visa or Mastercard for any of those brands and many more. Capital One could try to set up similar partnerships, but that would likely come at the expense of their own card issuing, which is and would continue to be even after the merger, the biggest part of its business.

Second, the argument that the merger will create a more potent rival to Visa and Mastercard depends on the possibility of moving many or all of the credit cards issued by Capital One onto their in-house Discover network. That can be done, but it could well be a mess. Moving significant consumer credit accounts from one payment network to another is a big undertaking and, when it’s been done in the past, has caused major issues including consumers being unable to access their accounts or experiencing a big hit to their credit rating.

Plus there’s something of a catch 22 involved in migrating credit cards from one payment network to another. If Capital One is aggressive in transferring all of its cards onto Discover, then the odds that they actually could save on lower operating costs are much better. Fees for using a payment network are a major cost for card issuers. Moving aggressively also creates more opportunities for fatal mistakes, however, like damaging customers’ credit. On the flip side, Capital One moving only a few of its cards over would give more transition time, but would require them to continue paying fees to Visa and Mastercard without truly becoming a competitor. Either route could also complicate efforts to create rewards programs that rival Visa’s and Mastercard’s programs; other companies may not be eager to participate given uncertainty around how the transfer will play out.

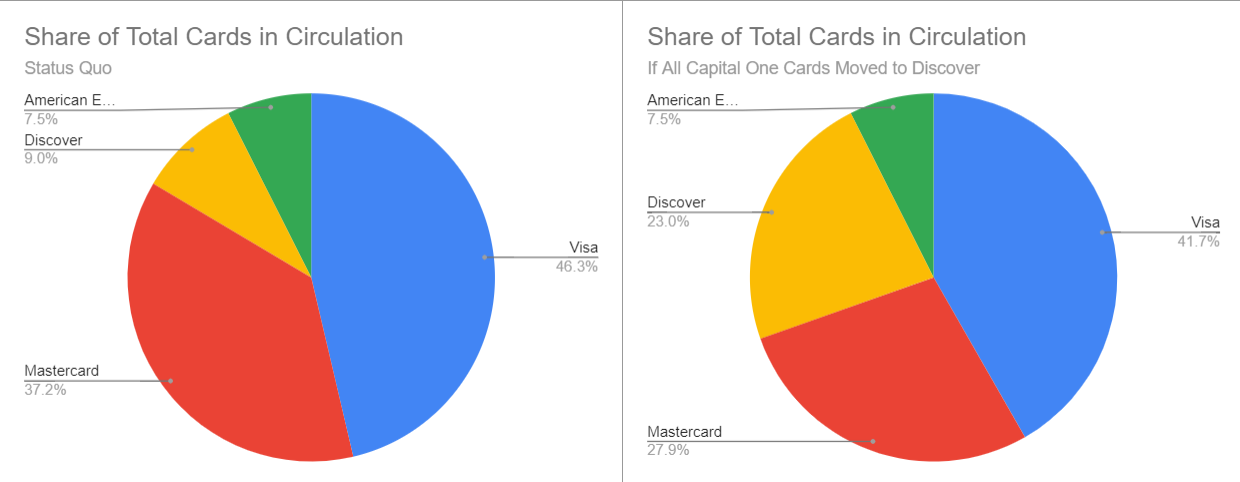

Finally, if Capital One moved all of its cards over to the Discover network, it could usurp about 10 percent of Visa’s transaction volume and around 25 percent of Mastercard’s (Capital One has a lot of cards on both, but Visa has a much larger pool of other issuers’ cards on its network, so Capital One represents a markedly smaller share of traffic on their network). As of 2022, Visa’s network had 385 million cards, Mastercard’s had 309 million, and Discover’s had 75 million. That means that the new distribution (assuming the transaction volume is distributed roughly evenly across cards on all the processing networks) could look like Visa with 347 million, Mastercard with 232 million, and Discover with 191 million.

If that’s how it plays out, there’s some risk that Capital One/Discover would actually cement Visa’s advantage even more. Sure, Visa loses some 39 million cards, but Mastercard, which is already the smaller of the two, loses twice that. So, more than anything, it could be that the one true rival to Visa is weakened, leading a duopoly to become a monopoly. As far as how that impacts market share, Visa would go from 46 percent to 42 percent, Mastercard would plummet from 37 percent to 28 percent, and Discover would jump from 9 percent to 23 percent (for simplicity, AMEX is being treated as exogenous), as shown in the charts below.

And if that’s how it plays out, it could give Mastercard or American Express an opening to try and merge with each other or with other payment networks (i.e. PayPal or Klarna) and pitch it as the only way to preserve any true competition with Visa. The argument there is basically two pronged. First, Mastercard and AMEX are weaker and much less competitive, so they need a leg up to survive. Second, Capital One got to merge, so shouldn’t they? This is a common tactic corporations use in concentrated markets to justify even further concentration. See, for example, airlines.

The Merger Is Likely Anticompetitive On Net

That’s a lot to digest, but broadly, there are six things that need to be kept in mind when evaluating the Capital One/Discover merger:

- The merger will have impacts across multiple types of financial products. The two biggest are credit card issuing and credit card payment processing.

- Both Capital One and Discover focus largely on subprime borrowers. That means that, even though concentration in the issuer space may not generally be an issue, it could be much worse for those with the least access to credit already.

- Even for cardholders who do not consider interest rates while selecting a card, card issuers do compete on rewards programs, security measures, annual fees, and other features that could be gutted if a company has the market share to get away with it.

- Capital One is donning a veneer of consumer champion, mostly by claiming that it will be able to compete more effectively with Visa and Mastercard.

- Capital One’s ability to compete with Mastercard and Visa is complicated by a number of factors, including built-in advantages to Visa and Mastercard’s existing partnerships and friction in transferring Capital One cards to Discover.

- Even in the event that the merger does weaken Visa and Mastercard, it would likely asymmetrically harm Mastercard, potentially making Visa even more dominant.

The proposed merger between Capital One and Discover is complicated for a lot of reasons. Both companies offer an assortment of financial services (see this handy list from US News and World Report). Consequently, the merger will send ripples throughout an array of different banking and financial markets. Yet the meat of the deal centers on credit card issuing and payment processing. Ultimately, there are a lot of reasons why claims about Capital One’s acquisition of Discover being beneficial for consumers should be taken with a grain of salt. There are a lot of antitrust concerns, whether focusing on the card issuer space or payment processing. In particular, the deal would combine two of the largest subprime credit card issuers and could lead to worse terms for subprime borrowers. On the network side, while there is some possibility that Capital One could make the Discover network competitive with Visa and Mastercard, it could just as easily flounder or even make things worse by weakening Mastercard disproportionately. Between all of these competitive harms and other issues, plus concerns around community reinvestment (a concern raised here) and other past regulatory issues (especially recent probes of Discover), this deal could cause serious harm and deserves to face rigorous scrutiny moving forward.

In condemning Nippon Steel’s proposed acquisition of U.S. Steel, many politicians, from John Fetterman to Donald Trump, are ignoring the severe costs of the alternative tie-up with a domestic steel-making rival—the harms to competition in both labor and product markets from the alternative merger with Cleveland-Cliffs (the “alternative merger”). Whatever security concerns might flow from ceding control of a large steel operation to a Japanese company must be assessed against the likely antitrust injury that would be inflicted on domestic workers and steel buyers by combining two direct horizontal competitors in the same geographic market. This basic economic point has been lost in the kerfuffle.

Harms to Labor

The first place to consider competitive injury from the alternative merger is the labor market, in which Cleveland-Cliffs and U.S. Steel compete for labor working in mines. If Cleveland-Cliffs (“Cliffs”) had been selected by U.S. Steel, there would only be one steel employer remaining in some geographic markets such as northern Minnesota and Gary, Indiana. This consolidation of buying power would have reduced competition in hiring of steel workers, almost certainly driving down workers’ wages by limiting their mobility.

To wit, Minnesota’s Star Tribune noted that “Cleveland-Cliffs and U.S. Steel have long histories on Minnesota’s Iron Range, controlling all six of the area’s taconite operations. Cliffs fully owns three of the six taconite mines, and U.S. Steel owns two.” Ownership of the sixth mine is shared between Cliffs (85%) of U.S. Steel (15%). A Cliffs/U.S. Steel merger also would have made the combined company the sole industry employer in the region surrounding Gary, per the American Prospect. Additional harms from newfound buying power include reduced jobs and greater control over workers who retain their jobs.

The newly revised DOJ/FTC Merger Guidelines explain that labor markets are especially vulnerable to mergers, as workers cannot substitute to outside employment options with the same ease as consumers substituting across beverages or ice cream. But the harm to labor here is not merely theoretical: A recent paper by Prager and Schmitt (2021) found that mergers among hospitals had a substantial negative effect on wages for workers whose skills are much more useful in hospitals than elsewhere (e.g., nurses). In contrast, the merger had no discernible effect on wages for workers whose skills are equally useful in other settings (e.g., custodians). A paper I co-authored with Ted Tatos found labor harms from University of Pittsburgh Medical Center’s acquisitions of Pennsylvania hospitals. And Microsoft’s recent acquisition of Activision was immediately followed by the swift termination of 1,900 Activision game developers, a fate that was predictable based on the combined firm’s footprint among gaming developers, as well job-switching data between Microsoft and Activision.

This is the type of harm that the U.S. antitrust agencies would almost assuredly investigate under the new antitrust paradigm, which elevates workers’ interests to the same level as consumers’ interests. Indeed, the Department of Justice recently blocked a merger among book publishers under a theory of harm to book authors. Under Lina Khan’s stewardship, the Federal Trade Commission is likely searching for its own labor theory of harm, potentially in the Kroger-Albertsons merger.

And the Nippon acquisition would largely avoid this type of harm, as Nippon does not compete as intensively, compared to Cliffs, against U.S. Steel in the domestic labor market. To be fair, Nippon does have a small American presence: It has investments in several U.S. companies and employs (directly and indirectly) about 4,000 Americans—but far fewer than U.S. Steel (21,000 U.S. based employees) and Cliffs (27,000 U.S. based employees). Importantly, Nippon employs no steelworkers in Minnesota, and its plants in Seymour and Shelbyville, Indiana are roughly a three-hour drive from Gary.

It bears noting that United Steelworkers (USW), the union representing steelworkers, has come out against the Nippon/U.S. Steel merger, alleging that U.S. Steel violated the successorship clause in its basic labor agreements with the USW when it entered the deal with a North American holding company of Nippon. This opposition is not proof, however, that the alternative merger is beneficial to workers, or even more beneficial to workers than the Nippon deal. Recall that the union representing game developers endorsed Microsoft’s acquisition of Activision, which turned out to be pretty rotten for 1,900 former Activision employees. Sometimes union leaders get things wrong with the benefit of hindsight, even when their hearts are in the right place.

Harms to Steel Buyers

Setting aside the labor harms, the alternative merger would result in Cliffs becoming “the last remaining integrated steelmaker in the country.” Mini-mill operators like Nucor and Steel Dynamics do not serve some key segments served by integrated steelmakers, such as the market for selling steel to automakers. In particular, automakers cannot swap out steel made from recycled scrap at mini-mills with stronger and more malleable steel made from steel blast furnaces. According to Bloomberg, a combined Cliffs/U.S. Steel would become the primary supplier of coveted automotive steel.

The prospect of Cliffs acquiring U.S. Steel triggered the automotive trade association, the Alliance for Automotive Innovation, to send a letter to the leadership of the Senate and House subcommittees on antitrust, explaining that a “consolidation of steel production capacity in the U.S. will further increase costs across the industry for both materials and finished vehicles, slow EV adoption by driving up costs for customers, and put domestic automakers at a competitive disadvantage relative to manufacturers using steel from other parts of the world.”

Moreover, a U.S. Steel regulatory filing detailed how antitrust concerns in the output market factored in its decision to reject Cliffs’s bid. U.S. Steel’s proxy noted: “A transaction with [Cliffs] would eliminate the sole new competitor in non-grain-oriented steel production in North America as well as eliminate a competitive threat to [Cliffs’s] incumbent position in the U.S., and put up to 95% of iron ore production in the U.S. under the control of a single company.”

Once again, the lack of any material presence by Nippon in the United States ensures that such consumer harms are largely limited to the Cliffs tie-up. An equity research analyst with New York-based CFRA Research who follows the steel industry noted that Nippon has a “very small footprint currently in North America.”

Balancing Security Concerns Against Competition Harms

Regarding national security concerns from a Nippon-U.S. Steel tie-up, The Economist opined these harms are exaggerated: “A Chinese company shopping for American firms producing cutting-edge technology that could help its country’s armed forces should, and does, set off warning sirens. Nippon’s acquisition should not.” If the concern is control of a domestic steelmaker during wartime, the magazine explained, U.S. Steel’s operations “could be requisitioned from a disobliging foreign owner.” For the purpose of this piece, however, I conservatively assume that the security costs from a Nippon tie-up are economically significant. My point is that there are also significant costs to workers and automakers from choosing a tie-up with Cliffs, and sound policy militates in favor of measuring and then balancing those two costs.

Finally, this perspective is based on the assumption that U.S. Steel must find a buyer to compete effectively. Maintaining the status quo would evade both national security and competition harms implicated by the respective mergers. But if policymakers must choose a buyer, they should consider both the competition harms and the national security implications. Ignoring the competition harms, as some protectionists are inclined to do, makes a mockery of cost-benefit analysis.

The news of the layoffs was stunning: Three months after consummating its $68 billion acquisition of Activision, Microsoft fired 1,900 employees in its gaming division. The relevant question, from a policy perspective, is whether these terminations reflect the exercise of newfound buying power made possible by the merger? If so, then Microsoft may have just unwittingly exposed itself to antitrust liability, as mergers can be challenged after the fact in light of clear anticompetitive effects.

The Merger Guidelines recognize that mergers in concentrated markets can create a presumption of anticompetitive effects. When studying the impact of a merger on any market, including a labor market, the starting place is to determine whether the merged firm collectively wielded market power in some relevant antitrust market. That inquiry can be informed with both direct and indirect evidence.

Direct evidence of buying power, as the name suggests, is evidence that directly shows a buyer has power to reduce wages or exclude rivals. Indirect evidence of buying power can be established by showing high market shares (plus entry barriers) in a relevant antitrust market. It bears noting that, when it comes to labor markets, high market shares are not strictly needed to infer buying power due to high search and switching costs (often absent in output markets).

Beginning with the direct evidence, Activision exhibited traits of a firm with buying power over its workers. For example, before it was acquired, Activision undertook an aggressive anti-union campaign against its workers’ efforts to organize a union. Moreover, workers at Activision complained about their employer’s intransigent position on granting raises, often demanding proof of an outside offer. A recent article in Time recounted that “Several former Blizzard employees said they only received significant pay increases after leaving for other companies, such as nearby rival Riot Games, Inc. in Los Angeles.” Activision also entered a consent decree in 2022 with the Equal Employment Opportunity Commission to resolve a complaint alleging Activision subjected its workers to sexual harassment, pregnancy discrimination, and retaliation related to sexual harassment or pregnancy discrimination.

Moving to the indirect evidence, one could posit a labor market for video game workers at AAA gaming studios. Both Microsoft and Activision are AAA studios, making them a preferred destination for industry labor. Independent studios are largely regarded as temporary stepping stones toward better positions in large video game firms.

To estimate the merged firm’s combined share in the relevant labor market, in a forthcoming paper, Ted Tatos and I study CareerBuilder’s Supply and Demand data, filtering on the term “video game” in the United States to recover job applications and postings over the last two years. The table summarizes the results of our search in the Spring 2022, a few months after the Microsoft-Activision deal was announced. Our analysis conservatively includes small employers that workers at a AAA studio such as Activision likely would not consider to be a reasonable substitute.

Job Postings Among Top Studios in Video Game Industry – CareerBuilder Data

| Company Name | Number of Job Postings | Percent of Postings | Corporate Entity |

| Activision Blizzard, Inc. | 1,270 | 26.0% | Microsoft |

| Electronic Arts Inc. | 856 | 17.5% | |

| Rockstar Games, Inc. | 287 | 5.9% | Take-Two |

| Ubisoft, Inc. | 258 | 5.3% | |

| 2k, Inc. | 143 | 2.9% | Take-Two |

| Zenimax Media Inc. | 128 | 2.6% | Microsoft |

| Epic Games, Inc. | 112 | 2.3% | |

| Lever Inc | 106 | 2.2% | |

| Wb Games Inc. | 101 | 2.1% | |

| Survios, Inc. | 100 | 2.0% | |

| Riot Games, Inc. | 91 | 1.9% | Tencent |

| Zynga Inc. | 84 | 1.7% | Take-Two |

| Funcom Inc | 79 | 1.6% | Tencent |

| 2k Games, Inc. | 74 | 1.5% | Take-Two |

| Complete Networks, Inc. | 65 | 1.3% | |

| Gearbox Software | 58 | 1.2% | Embracer |

| Digital Extremes Ltd | 43 | 0.9% | Tencent |

| Naughty Dog, Inc. | 43 | 0.9% | Sony |

| Mastery Game Studios, LLC | 26 | 0.5% | |

| Crystal Dynamics Inc | 25 | 0.5% | Embracer |

| Skillz Inc. | 25 | 0.5% | |

| Microsoft Corporation | 24 | 0.5% | Microsoft |

| Others | 887 | 18.2% | |

| TOTAL | 4,885 | 100.0% |

As indicated in the first row, Activision lies at the top in number of job postings in the CareerBuilder data, with 26.0 percent. Prior to the Activision acquisition, Microsoft accounted for 3.1 percent of job postings (the sum of Zenimax Media and Microsoft rows). Based on these figures, Microsoft’s acquisition of Activision significantly increased concentration (by more than 150 points) in an already concentrated market (post-merger HHI above 1,200). This finding implies that the merger could lead to anticompetitive effects in the relevant labor market, including layoffs.

It bears noting that the HHI thresholds established in the 2023 Merger Guidelines (Guideline 1) were most likely developed with product markets in mind. Indeed, the Guidelines recognize in a separate section (Guideline 10) that labor markets are more vulnerable to the exercise of pricing power than output markets: “Labor markets frequently have characteristics that can exacerbate the competitive effects of a merger between competing employers. For example, labor markets often exhibit high switching costs and search frictions due to the process of finding, applying, interviewing for, and acclimating to a new job.” High switching costs are also present in the video game industry: Almost 90 percent of workers at AAA studios in the CareerBuilder Resume data indicate that they did not want to relocate, making them more vulnerable to an exercise of market power than the HHI analysis above implies.

As any student of economics recognizes, a monopsonist not only reduces wages below competitive levels, but also restricts employment relative to the competitive level. So the immediate firing of 1,900 workers is consistent with the exercise of newfound monopsony power. In technical terms, the layoffs could reflect a change in the residual labor supply curve faced by the merged firm.

Why would Microsoft exercise its newfound buying power this way? To begin, many Microsoft workers, prior to the merger, could have switched to Activision in response to a wage cut. Indeed, we were able find in the CareerBuilder data that a substantial fraction of former Microsoft workers left Microsoft Game Studios to work for Activision. (More details on the churn rate to come in our forthcoming paper.) Post-merger, Microsoft was able to internalize this defection, weakening the bargaining position of its employees, and putting downward pressure on wages. In other words, Microsoft is more disposed to cutting Activision jobs than would a standalone Activision. Moreover, by withholding Activision titles from competing multi-game subscription services—the FTC’s primary theory of harm in its litigation, now under appeal—Microsoft can give an artificial boost to its platform division. This input foreclosure strategy would compel Microsoft to downsize its gaming division and thus its gaming division workers.

Alternative Explanations Don’t Ring True

The contention that these 1,900 layoffs flowed from the merger, as opposed to some other force, is supported in the economic literature in other labor markets. A recent paper by Prager and Schmitt (2021) studied the effect of a competition-reducing hospital merger on the wages of hospital staff. Consistent with economic theory, the merger had a substantial negative effect on wages for workers whose skills are much more useful in hospitals than elsewhere (e.g., nurses). In contrast, the merger had no discernable effect on wages for workers whose skills are equally useful in other settings (e.g., custodians). As Hemphill and Rose (2018) explain in their seminal Yale Law Journal article, “A merger of competing buyers can exacerbate the merged firm’s incentive to buy less in order to drive down input prices.”

Microsoft has its defenders in academia. According to Joost van Dreunen, a New York University professor who studies the gaming business, the video game industry is “suffering through a winter right now. If everybody around you is cutting their overhead and you don’t, you’re going to invoke the wrath of your shareholders at some point.” (emphasis added) This point—which sounds like it was fed by Microsoft’s PR firm—is intended to suggest that the firings would have occurred absent the merger. But there are two problems with this narrative. First, Microsoft’s gaming revenues are booming (up nine percent in the first quarter of its 2024 fiscal year), which makes industry comparables challenging. What were the layoffs among video game firms that also grew revenues by nine percent? Second, video programmers and artists are not “overhead,” such as HR workers or accountants. (Apologies to those workers.) Thus, their firing cannot be attributed to some redundancy in deliverables.

Microsoft’s own press statement about the layoffs vaguely states that it has “identified areas of overlap” across Activision and its former gaming unit. But that explanation is just as consistent with the labor-market harm articulated here as with the “eliminating redundancy” efficiency.

Bobby Kotick, the former CEO of Activision, received a $400 million golden parachute at the end of the year for selling his company to Microsoft. That comes to about $210,500 per fired employee, or about two years’ worth of severance for each worker laid off. Too bad those resources were so regressively assigned.

The mid-sized town of Springfield maintained a speed limit of 25 miles per hour on a one-mile stretch of Main Street that was home to both an elementary school and a middle school. The speed limit had been in force for decades. Children as young as three walked on the sidewalks and sometimes unexpectedly darted across the street. By forcing drivers to slow down, the speed limit minimized the risk of serious injury and death. While collisions occurred occasionally on this busy road, no pedestrian, driver, or passenger, had ever suffered a serious injury. For years, the 25-mph limit attracted little attention, positive or negative, and was accepted by residents as a fact of life in the town.

One day though, a group of prominent businesspeople and professionals petitioned for a change. These local notables called on the mayor to eliminate the speed limit because it contributed to congestion on the important road and delayed drivers from reaching their destination. In their petition, they contended that removal of the speed limit would allow people to spend less time on the road and more time being productive at their place of work and socializing with their near and dear. They commissioned an economic study that concluded that removing the speed limit would allow children visiting their grandparents to spend less time in the car and more time with their doting grandma or grandpa. Attempting to preempt concerns about road safety, they claimed the speed limit was not necessary, as drivers would naturally be concerned for the safety of kids. They argued that police could pull drivers over for reckless behavior or for driving unsafely. Further, drivers who negligently caused injuries or deaths would face serious consequences, including prison. That threat would deter dangerous driving.

Given the standing of opponents of the speed limit, the mayor soon after lifted speed restrictions on the road. He declared, “The 25 mph may have worked when we led more leisurely lives and could afford to spend an extra 10 or 15 minutes in traffic. But that is the past, we are all busy people now. The speed limit is an impediment to the smooth flow of traffic today.” He did not dismiss concerns about traffic safety and directed the town’s police force to pull over drivers who drive in an “unreasonably unsafe manner.”

The new system appeared to work fine at first. Vehicles proceeded past the schools much faster than they had previously. Congestion was a thing of the past. As proponents of the repeal predicted, the people of Springfield were getting to spend a little more time with their coworkers, friends, and families.

But the repeal of the speed limit was not an unalloyed benefit for the town. With a local bottleneck relieved, many people stopped using the town’s famous monorail and got into their cars, trucks, and vans instead. Many living near Main Street who had previously walked to nearby grocery stores and restaurants started driving. Although traffic congestion on Main Street had been addressed, it had a cost. Rescinding the speed limit encouraged more driving and increased air pollution.

Some drivers who scrupulously followed the 25-mph speed limit began to drive more aggressively. Because there was no speed limit, some felt emboldened to drive past the school at 50 mph or faster, so long as they couldn’t spot any children in harm’s way. That speed was not illegal under the letter of the law unless an observing police officer deemed it to be “unreasonably unsafe.” No one knew quite what this meant. It was rumored that police officers considered the time of day, level of traffic, weather conditions, the proximity of children to the road, and the importance of driver’s trip before passing judgment. When teachers at the elementary school complained that the sound of cars sometimes traveling at 70 mph scared the young children, the mayor said, “While we can’t quantify the subjective terror felt by kids, we can measure the shortened commutes for Springfielders.” To keep their children safe, the elementary school ended recess and other outdoor activities for all children up through fourth grade.

Enforcement of the new “unreasonably unsafe” standard for the rule also drew concern. When a local executive was pulled over for driving 80 mph, the police officer, whose conversation was recorded on a bodycam, let him off with a friendly “warning,” obsequiously saying, “I get it, sir. You are a busy man. If we had kept the 25 mph as some wanted, you’d be spending time stuck here, instead of tending to your important work.”

But others were not so lucky. Black drivers, especially those driving late model cars, were frequently pulled over for going 30 mph. That was only five miles per hour faster than the old speed limit, but many officers deemed it “unreasonably unsafe.” The discriminatory pattern of enforcement was impossible to ignore.

Proponents of the new approach dismissed growing criticisms. They said the improved flow of traffic trumped other considerations. They conceded fewer people were taking the monorail and walking for short trips, but insisted these are not “traffic-related” issues. The city should address these problems though other measures, they said. Moreover, discriminatory enforcement was not inherent to the new standard and could be resolved. The mayor pledged to improve police training and socialize officers “not to see color” in performing their duties.

But after one deadly incident, even the strongest proponents were at a loss for defenses. One afternoon, the 20-year-old scion of a local real estate magnate took his new red Ferrari out for a spin. He wanted to test its acceleration and went from zero to 60 mph on Main Street in four seconds. Focused on his immediate aim, he did not notice a 12-year-old schoolboy who had run into the street to retrieve an errant soccer ball and struck him. The boy was killed instantly. The local prosecutor pledged to prosecute the driver and seek the maximum possible sentence. But whatever the result, no prison sentence would bring the young boy back to life or provide solace to his parents and siblings.

The tragic death of the child made clear to almost everyone that the new system was a failure. While its proponents rationalized or offered solutions for increased driving, forcing schoolchildren indoors, and discriminatory enforcement, they had no ready answers for the clearly avoidable fatality. The old 25-mph speed limit had created modest inconveniences, but it would have prevented the fatal accident. In addition to allowing schoolchildren to play safely outside, the old rule encouraged people to use public transit and to walk and reduced the potential for subjective and discriminatory law enforcement. It was an example of what the economist Gardiner Means called a good “canalizing rule.”

For the past 40 years, the federal judiciary has followed the model of Springfield and overturned or weakened bright-line antitrust rules for mergers and other business practices. For instance, the Supreme Court held that manufacturers dictating resale prices on their goods to retailers and wholesalers through contract—an example of a “vertical restraint” imposed on a firm at another level in the same supply chain—was no longer a categorically illegal practice. In place of such clear “speed limits,” it adopted the rule of reason as its default analytical framework—a standard that requires case-by-case assessment of “effects” and has practically legalized many formerly restricted business practices.

Much like Springfield’s decision gave license to residents to drive as they wish on Main Street, the courts have granted corporate executives broad discretion to compete and grow their enterprises as they wish. In theory, this case-by-case approach allows business leaders to engage in socially beneficial mergers and to use vertical restraints to protect against harmful free riding. But as the story of Springfield shows, legal rules are used not only to decide specific cases but also to structure individual and organizational behavior.

Congressional and regulatory enactment of bright-line rules on mergers and unfair practices would channel business strategy in different and better directions. Strong rules against mergers, such as a general prohibition on all acquisitions by firms with more than a 30% share in any market or $10 billion in total assets, might sacrifice the occasional beneficial consolidation (there are ample grounds to be skeptical of such losses to be sure). Yet these bright-line rules would channel business strategy toward internal expansion and development of new production methods. Similarly, a prohibition on non-compete clauses could prevent an employer from stopping an employee from departing for a rival after receiving valuable training on the job, but it would also encourage employers to retain workers through regular raises and promotions and fair treatment and to use more targeted tools for protecting their proprietary information. And bright-line rules for antitrust enforcement would limit governmental discretion and the ability of unscrupulous officials to reward friendly businesses and punish their perceived enemies. These rules would deprive the CEOs of the largest corporations of autonomy and surely make them unhappy. But for the rest of us, life would be better.

The announced PGA-DP World Tour-LIV Golf “partnership” (read, merger) has reverberated throughout the sporting world, sending shockwaves across not only the golf industry but the sports world as well. ESPN reported players reacting with “complete and utter shock” at the announcement, as did, much of the sports media, calling the news “stunning”.

Let’s clear the air. None of this was surprising in the slightest.

The golf industry merger is but the latest example of, as the Propellerheads and the legendary Dame Shirley Bassey melodically put it, history repeating. Sports historians and economists have recounted the episodes of consolidation that have precipitated the modern-day U.S. professional sports leagues. These commercial joinders all share a common theme: a response by an entrenched, dominant entity faced with the threat of entry and the prospect of seeing its monopsony power diluted by the crucible of competition.

The real question with which golfers, as the primary interested party, should concern themselves is quo vadem: where do we go from here? This article aims to shed some light on that question by first recounting what has befallen athletes in other leagues following similar consolidation, evaluating what similar or differing conditions characterize this golf industry consolidation, then evaluating what path such conditions presage for current players. Finally, I address what steps players could take to protect their interests from any wage suppression that may result from the merger.

Wage suppression warrants concern here for the same reason it has in other sports cases (not to mention the broader labor market): the leverage of monopsony power. Monopsony power in a labor market reflects an entity’s ability to restrain wages below the levels that would prevail under competitive conditions. Such actions reflect worker exploitation, defined as the ability to reduce wages below the marginal revenue product (MRP) of labor (the marginal revenues generated by the next unit of labor). When faced with an upward sloping labor supply curve, a firm will set its wages at MRP, just as, under similar competitive conditions in an output market, a seller will set its price equal to marginal cost.

As the FTC has observed, the exercise of monopsony power in input markets reflects the mirror image of monopoly power in output markets. Historically, the PGA Tour has behaved like a monopsonist: it unilaterally set Tour members’ pay below competitive levels, reduced the input of labor, and excluded competitors. (Those familiar with the NCAA antitrust litigation will immediately notice its similarities to the PGA.)

The PGA Tour’s actions mirror those of other entities that held the same power over workers. Faced with the possibility of increased competition for labor, a monopsonist will commonly seek to either 1) prevent such entry or 2) acquire the entrant, and thus reduce or eliminate workers’ ability to choose among alternatives. Prior to the announced merger, the PGA Tour sought to do just that, by threatening golfers who considered joining LIV.

On that note, let’s start with a quick trip down memory lane to acquaint ourselves with how much this latest merger resembles previous sports industry consolidation.

In 1962, the AFL sued the NFL, alleging the latter had monopolized the market for professional football leagues; the district court ruled against the AFL, finding that the NFL did not have monopoly power. In the following year, the 4th Circuit Court of Appeals affirmed the lower court’s finding against the AFL, ending the litigation. In June of 1966, following a series of secret meetings, the two leagues announced the decision to merge. The September 1975, Congressional oversight hearings on the NFL labor-management dispute provide some details of the effects on labor. In his statement, Ed Garvey, Director of the NFL Players’ Association president at the time explained that, between the birth of the AFL and 1966, little if any bargaining between labor and management in the NFL occurred, noting that “Because of competition for player services, salaries nearly tripled, and the NFL was anxious to institute some fringe benefits to attract players to the NFL. When merger plans were announced in the summer of 1966, efforts were mounting within the NFLPA to oppose the merger, but Congress exempted the merger before there could be any serious opposition mounted.” The exemption refers to Congress’ statutory enshrinement of monopoly and monopsony power for major sports leagues in the form of 15 USC Ch. 32, §1291, “Exemption from antitrust laws of agreements covering the telecasting of sports contests and the combining of professional football leagues.” The provision passed in 1966 amended the Sports Broadcasting Act of 1961 to exempt merging sports leagues from antitrust laws as long as the merger “increases rather than decreases the number of football clubs.”

A similar scenario played out in the history of professional basketball in the United States, in which the rise of the American Basketball Association (ABA) militated against the exercise of monopsony power by owners of National Basketball Association (NBA) teams. As sports economist David Berri observed in the Antitrust Bulletin, while NBA players received a wage share of approximately 27 percent in 1970, “By 1972–1973, the NBA had to increase salaries to prevent players from joining a league that clearly was a legitimate competitor.” At the time, the leagues considered merging; however the existence of a reserve clause that gave a team control over a player’s mobility represented an untenable situation for the athletes, who sued to block it in 1970. (Robertson v. National Basketball Association, 556 F.2d 682 (2d Cir. 1977). The 1976 settlement culminated in the Oscar Robertson Rule and resulted in the elimination of the reserve clause (also known as the “option clause”) and rise of free agency rules that exist today.

National Hockey League (NHL) player wages also benefited from inter-league competition. Like other professional sports leagues, the NHL included a reserve clause in player contracts, bestowing exclusive negotiating rights on the original team with which a player signed. In the early 1970s, the World Hockey Association (WHA) entered the market, seeking to fill demand for teams in various major cities that represented relatively smaller markets than those having NHL teams.

Like LIV Golf, the WHA attracted top players by offering greater mobility and the potential for more lucrative compensation. As a result, it signed sixty-seven players, including the legendary Bobby Hull, in its inaugural 1972 season; for the following year, the WHA also signed another hockey superstar, Gordie Howe. While NHL sued to block the players from leaving from the WHA (just as the PGA threatened potential LIV signees with expulsion), a Massachusetts district court denied injunctive relief, allowing two stars, Gerry Cheevers and Derek Sanderson to join the WHA. Concurrently, a federal court in Philadelphia enjoined the NHL from taking legal action to enforcing its reserve clause. (In total, litigation between the WHA and NHL spanned four separate suits.)The following year, 1973, the NHL abolished the reserve clause, replacing it with a one-year option. The 1975 collective bargaining agreement between the NHL and its players’ association included additional modifications, including guaranteed contracts and enabling players to enter into contracts without an option year. Negotiations between the NHL and WHA culminated in the June 22, 1979 NHL expansion, where four WHA teams, the Edmonton Oilers, New England (now Hartford) Whalers, Quebec Nordiques (now Colorado Avalanche), and Winnipeg Jets received NHL expansion slots and the rest of the WHA folded.

At this point, the common thread between the NFL, NBA, NHL and Major League Baseball merits emphasis, as it highlights the dichotomy between the PGA Tour and other major professional sports leagues. While athletes in other leagues have the benefit of a union and a collective bargaining agreement between the players’ association and the league, PGA Tour athletes do not. (Somewhat ironically, the caddies themselves do: The Association of Professional Tour Caddies.) The presence of a union could have cautioned Tiger Woods and Rory McIlroy, who apparently turned down a combined $1.5 billion from LIV only to now find themselves in the same position but sans the lucrative offer.

In response to the threat of entry, the PGA adopted a tripartite strategy that was one part carrot, one part stick, and one part a morality play. The latter, of course, referenced the source of LIV’s funding: a Saudi regime run by crown prince Muhammad bin-Salman, whom the US government found approved the brutal murder of Washington Post journalist Jamal Khashoggi. Of course, the merger exposed the lack of sincerity in such appeals. The carrot refers to the fact that the PGA Tour previously announced more than $100 million in purse increases for 2022, an apparent response to the threat of competition that resembles similar action by the NBA and NFL discussed above. Indeed, the PGA Commissioner acknowledged the treat to the Tour’s margins that LIV represented. As CBS Sports Adam Silverstein reported, Monahan explained that “f you just look at the environment we’re in, the PIF was controlling LIV, and we were competing against LIV.It felt good about the changes we’d made and the position we were in, but ultimately, to get the competitor off the board — to have them exist as a partner, not as an owner…” The PGA also leveraged its stick, banning golfers who participated in LIV tournaments.

The PGA Tour’s threats of lifetime bans against players who sought to avail themselves financially of LIV’s competition with the PGA Tour also bears close resemblance to the reserve clause that existed in baseball (and other major sports). The reserve clause in a contract bound a professional baseball player to a single team; prior to 1887, baseball contracts stipulated that the player agreed to “abide by the constitution and bylaws of organized baseball” a phrase remarkably similar to the language used by PGA Tour Commissioner Jay Monahan in his letter to tour members reminding them that “You have made a different choice, which is to abide by the Tournament Regulations you agreed to when you accomplished the dream of earning a PGA TOUR card.”

The 1889 version of the baseball contract included a clause that permitted a team to “reserve” a player for the following season at a rate at least as high as the player’s current-year compensation. As economists James Quirk and Rodney Fort explained in their book “Pay Dirt: The Business of Professional Sports Teams”, interpretation of the clause effectively granted the owners a perpetual option to retain a player’s services over his entire career, particularly considering that owners agreed not to hire players from other teams’ reserve lists. Subsequently, following the Supreme Court decision in Federal Baseball Club v. National League, 259 U.S. 200 (1922), which granted baseball’s antitrust exemption, the following clause was incorporated in every player contract from the 1920s into the 1950s:

[If] the player and the club have not agreed upon the terms of such contract [for the next playing season], then … the club shall have the right to renew this contract for the period of one year on the same terms, except that the amount payable to the player shall be such as the club shall fix in said notice…

This incarnation of the reserve clause lasted nearly a century, binding a player to a team and prohibiting his ability to obtain better wages elsewhere. During the 1957 Congressional hearings on organized professional team sports, Major League Baseball reported revenues from the previous five years. In a recent paper, sports economist David Berri analyzed these data, showing that, during this period, MLB paid less than 25% of the revenues to players, a clear indication of the wage-restraining effects of the reserve clause. The first major cracks in owners’ hegemony over labor came at the hands of Golden Glove winner Curt Flood in 1969. Upon being traded from St. Louis to the Philadelphia Phillies and told that he had no say in the matter, Flood filed suit, Flood v. Kuhn, 407 U.S. 258 (1972), telling Commissioner Bowie Kuhn that “I do not regard myself as a piece of property to be bought or sold.” While the Supreme Court ruled 5-3 in 1922 to exempt baseball from the jurisdiction of the Sherman Act, an agreement between Major League Baseball and the players’ union granted free agency to players with at least six years of tenure beginning after 1976. This agreement accorded greater bargaining power to players and permitted them to capture a higher wage share. The eponymous 1998 Curt Flood Act revoked baseball’s antitrust exemption as it related to the employment of players, allowing them to enjoy the fruits of competition for their services.

More recently, a group of approximately 1,200 fighters who sued the Ultimate Fighting Championship (UFC) mixed martial arts (MMA) promotion company, won class certification. The Plaintiffs alleged that Zuffa, Inc. (d/b/a, UFC) sought to exclude competition from other promoters in an attempt to exert monopsony power to restrain fighters’ wages. In doing so, Plaintiffs claimed that 1) Defendants’ use of long-term exclusive contracts prevented them from competing elsewhere, 2) Defendants leveraged market power over the labor to force fighters to resign contracts, effectively locking them into perpetuity, 3) acquiring and terminating rival MMA promoters. Documents revealed in the litigation indicated that fighters’ wage share is only approximately 17 percent. Critically, this figure represented a substantial drop from the approximately 29 percent wage share that existed prior to the UFC’s acquisition of Strikeforce.

So what does all this presage for golfers’ futures? Absent potential regulatory intervention, nothing positive.

Two primary external forces counteract the exercise of monopsony power: 1) competitive entry and 2) collective bargaining. While lacking the latter, golfers benefited from the former in the form of LIV, which exposed the PGA’s ability to restrain compensation below competitive levels as evidenced by the purse increases once LIV became a viable competitor. Post-merger, golfers have neither and now find themselves facing an even stronger monopsonist. If golfers hope to maintain any semblance of a fair wage split with the newly formed industry leviathan, their primary recourse is organization into a Professional Golfers Union that can bargain collectively on their behalf. Otherwise, the outcome will mirror the UFC and the state of inequality in American society generally: a small cadre of patricians surrounded a multitude of workers fighting over table scraps. Of course, the newly merged entity will fight tooth and nail against such organization; those with market power seldom if ever concede it willingly. Nonetheless, one would do well to remember that the NBA has crossed swords with its Players’ Association numerous times, yet both sides have prospered. And so has the game.

Ted Tatos teaches econometrics at the University of Utah and regularly consults on economic issues involving antitrust, intellectual property, labor issues, and others. He can be reached at ttatos@eaecon.com.