Since the launch of ChatGPT back in November of 2022, what was once a concept confined to Sci-Fi novels has now certifiably hit the mainstream. The highly visible advances in artificial intelligence (AI) over the past few years have either been awe-inspiring or dread-inducing depending on your perspective, your occupation, and maybe how much Nvidia stock you owned before 2023. Many white-collar workers now fear that they may face the same job-displacing effects of automation that has plagued their blue-collar peers over the past several decades.

Nevertheless, at least one powerful constituency is absolutely thrilled with the rise of AI and is betting big on its success: Big Tech. Microsoft, currently the second most valuable company in the world with a mind-boggling $3.7 trillion market cap, is a leading AI zealot. This fiscal year alone, Microsoft plans to invest over $80 billion in AI-related projects.

As one of its big selling pitches to investors and consumers, Microsoft argues that AI has prompted massive efficiency gains internally, including eliminating a staggering 36,000 workers since 2023. Microsoft CEO Satya Nadella estimated that as much as 30 percent of the company’s code is now written by AI. Mr. Nadella, of course, has a lot riding on convincing shareholders and consumers that AI is a big deal. So, to what extent this claim is legitimate, or pure marketing fantasy, is uncertain. A recent working paper authored by Microsoft researchers and academics analyzes the productivity increases in (non-terminated) software developers who use AI tools. The authors find that developers using AI tools saw an average 26 percent increase in their productivity. If such experimental results generalize to the broader labor market, AI will certainly have a dramatic impact. Despite evident benefits towards companies from this productivity boon whether workers themselves stand to gain remains uncertain.

A Look into Software Developers’ Compensation

AI models capable of assisting with writing and coding tasks have existed for a couple of years now. Taking Mr. Nadella’s statements at face value, such models enjoy widespread utilization by developers and coders working for Big Tech. As such, if workers—and not just their employers—stand to benefit from AI, then worker compensation should reflect at least some evidence of these productivity gains.

Simple economic models of the labor market suggest that a technology that boosts the marginal productivity of labor will cause a concomitant increase in worker pay. After all, in competitive labor markets, workers should capture 100 percent of their marginal revenue product (MRP), which increases with productivity, though such an outcome rests upon a strong and often-violated assumption that the relevant labor market is perfectly competitive. When an employer has buying power, it can drive a wedge between the worker’s MRP and her wage. In lay terms, this means the employer can appropriate value created by the worker without sharing in the gains, the Pigouvian definition of exploitation. Thus, the extent to which workers benefit from this AI-induced productivity remains unclear. (In addition, a monopsony reduces employment relative to a competitive labor market; Microsoft’s mass firings since its acquisition of Activision in 2023 is also consistent with the exercise of monopsony power.)

While a recent article in The Economist highlights how the AI boom has led to some “superstar coders” seeing their “pay [] going ballistic,” this subset of workers represents a tiny sliver of the total labor market of developers. In that same article, The Economist also produced a graph showing a dramatic slowdown in hiring—job postings for software developers have dropped by more than two-thirds since the beginning of 2022. To understand how AI is affecting workers, we need to look at the labor market at large. Unfortunately, our analysis suggests that software developers have not yet benefited (and may never fully benefit) from their increase in productivity.

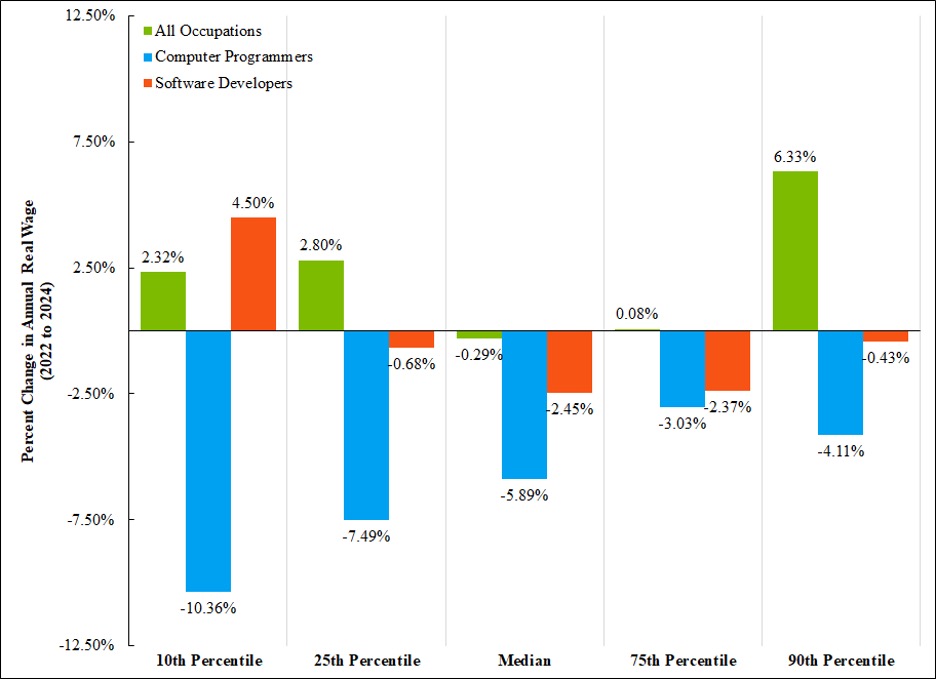

Figure 1 below takes the broadest look at how all software developers and computer programmers in the United States have (or have not) benefited from the rise in AI. The results are not pretty: While 2022 inflation has hit all workers hard, eroding much of their nominal wage increases, both computer programmers and software developers are faring much worse than the average worker. Per the BLS, the median wage of computer programmers decreased by 5.89 percent between 2022 and 2024.

Figure 1: Real Wages Are Flat for Most Workers, But Have Declined for Programmers and Developers

Source: Bureau of Labor Statistics’ Occupational Employment and Wage Statistics Annual Report; CPI sourced from FRED. Notes: We transformed this nominal data using CPI to be in 2024 dollars. Hence, this chart shows the real change in wages between 2022 to 2024 (i.e., accounting for inflation). 2024 is the most recent data release, and the 2024 data are not inclusive of data from Colorado.

Not even the top ten percent of software developers, including the “superstar coders” as dubbed by The Economist, appear to be thriving. Figure 1 also shows that the highest paid computer programmers (90th percentile) saw their real wages fall by 4.11 percent.

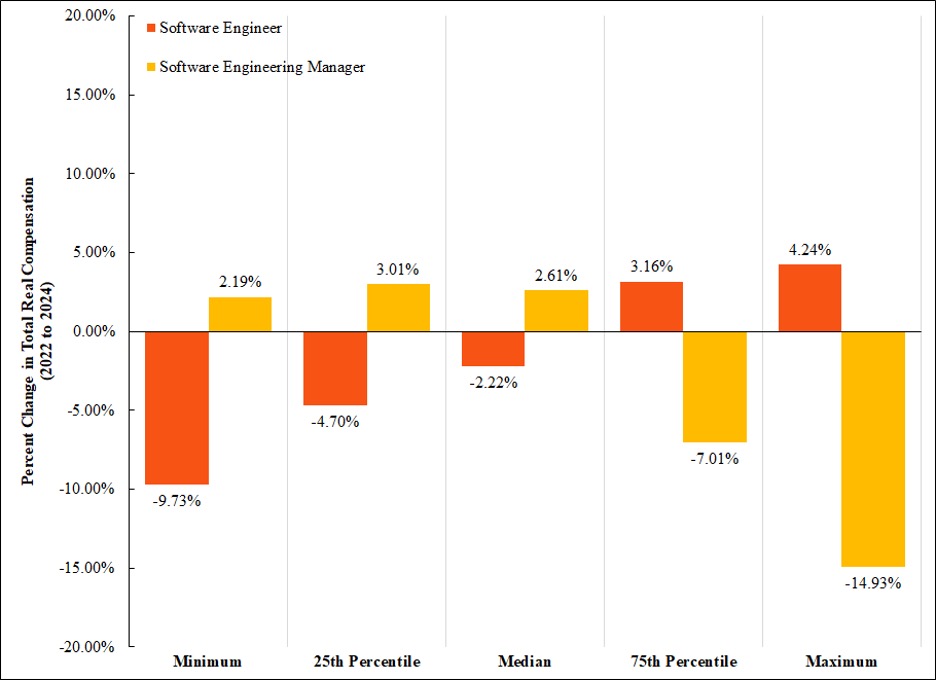

Workers for Big Tech fared no better. Indeed, the percentage change in the median compensation for software engineers employed by Big Tech effectively mirrors that reported in Figure 1—the median software engineer saw a 2.22 percent decrease in their real wages from 2022 to 2024 per data from Levels.fyi.

Figure 2: Software Engineers Working Big Tech Also Have Not Seen a Dramatic Rise in Wages

Source: Levels.fyi 2024 and 2023 year-end reports; CPI sourced from FRED. Notes: Levels.fyi collects self-reported data “for the top paying tech companies and locations.” Total compensation is inclusive of base salaries, stock grants, and bonuses. Note that Levels.fyi’s trend table has slightly different median compensation estimates than the box charts that we source our data from. It is unclear what causes this discrepancy. We transformed this nominal data using CPI to be in 2024 dollars. Hence, this chart shows the real change in total compensation between 2022 to 2024 (i.e., accounting for inflation).

At the very least, we see evidence that software engineering managers (depicted in yellow) have seen their compensation rise (by 2.61 percent), though nowhere near their supposed AI-powered productivity increase.

Microsoft-specific wage data were not easily accessible. The Economist reported that the median pay for software developers at “tech giants including Alphabet, Microsoft and, until recently, Meta” was close to $300,000. Lucky for us, however, Microsoft sponsors thousands of H-1B visas, which provides a source of publicly available salary data. Using these data, we can get a sense of the trend in how Microsoft software engineer compensation has evolved over time. Because they are beholden to their American employer, H-1B visa-holders likely earn wages below their American counterparts. Nevertheless, the trajectory of wages of H-1B workers should roughly track the trajectory of wages of their American peers.

Figure 3: H-1B Data Suggest That Microsoft Software Engineers’ Real Wage Stagnated in the 2020s

Source: Data is from H1B Grader.com which states that “salaries data is extracted from the H1B Labor Condition Applications (LCAs) filed with the US Department of Labor by [the] Microsoft Corporation.”Notes: We combined various positions’ pay information to produce this average salary measure. Positions that were consolidated had titles that indicated they were roles in software engineering or development. We explicitly excluded IT-specific roles.

While H-1B software engineers working at Microsoft saw real wage increases during the 2010s, by the 2020s, real wages appear to have stagnated. This trajectory likely reflects the trend for all Microsoft developers, including domestic workers.

While these figures are by no means perfect, if workers truly reaped benefits from their AI-boosted productivity in a significant way, the above charts should have reflected such an outcome. Unfortunately, from what we can see, wages have not captured much of AI’s productivity impact. This lends credence to the hypothesis of monopsony exploitation restraining wage growth—in other words, Microsoft (the employer) is appropriating the productivity gains of its workers, presumably because the workers do not have credible outside employment options to which they could turn easily in response to a wage cut.

Software Developers Face an Uncertain Future

Unfortunately, not only do software developers not receive boosts in their compensation commensurate with their productivity increases, but many also now risk losing their jobs. As noted above, Microsoft has shed 36,000 jobs since 2023.

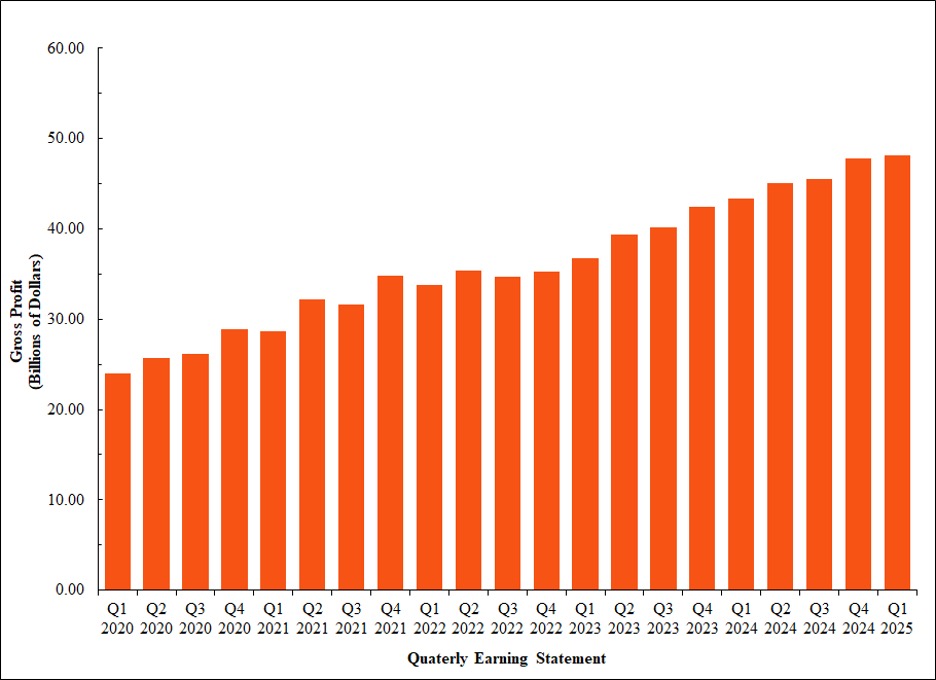

The cause of these mass layoffs does not appear to lie with any underperformance on Microsoft’s part. On the contrary, Microsoft’s gross profits have continued to rise over the past few years, as seen in Figure 4 below.

Figure 4: Microsoft Has Seen Significant Profit Growth in the Past Five Years

Source: MacroTrends.net.

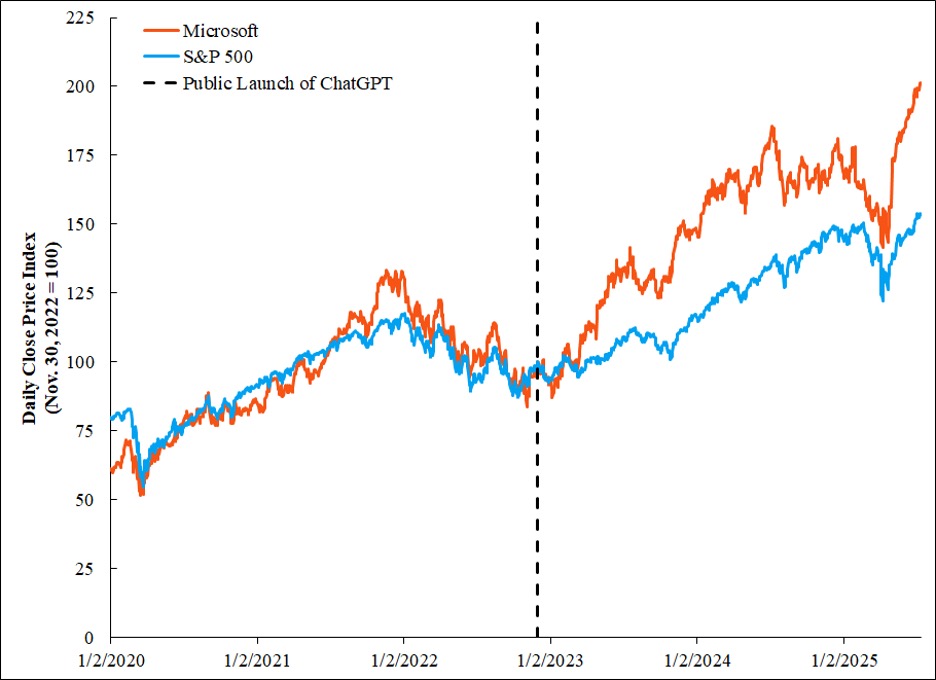

Microsoft stock has also performed tremendously since the release of ChatGPT. If anyone is benefiting from the increased productivity of its workers, it appears it is Microsoft itself. (To be fair, given that Big Tech workers’ compensation packages often include stock, they too benefit from the AI rally even if the compensation figures reviewed above may not reflect such increases.) The combination of layoffs and no real impact on pay appears to at least suggest that AI will function as a substitute, rather than a complement, to human labor.

Figure 5: Microsoft Stock Has Performed Well in the Age of AI

Source: Data retrieved using getsymbols package in Stata, sourced from Yahoo! Finance. Notes: As is standard, we used the adjusted closing stock price. Data is from Jan. 2, 2020 to July 11, 2025. Closing price indexed such that November 30, 2022 equals 100 (notable for being the date OpenAI first publicly released a demo of ChatGPT, which would go on to reach a million users in less than a week).

AI Fits a Trend of Growing Productivity and Wage Stagnation

Whether AI will truly revolutionize the workplace and make many human workers “go the way of the horses” remains to be seen. From what we have analyzed, however, even if AI does not replace human labor, workers should not put too much hope that they will reap the rewards of their increased productivity. AI continues a trend that started back in the 1980s: the divergence between worker’s productivity growth and their wages. Without a significant policy intervention in labor markets, such as a federal job guarantee or unionization to countervail monopsony power, AI may be a technology that continues to exacerbate the inequality of the 21st century.

The news of the layoffs was stunning: Three months after consummating its $68 billion acquisition of Activision, Microsoft fired 1,900 employees in its gaming division. The relevant question, from a policy perspective, is whether these terminations reflect the exercise of newfound buying power made possible by the merger? If so, then Microsoft may have just unwittingly exposed itself to antitrust liability, as mergers can be challenged after the fact in light of clear anticompetitive effects.

The Merger Guidelines recognize that mergers in concentrated markets can create a presumption of anticompetitive effects. When studying the impact of a merger on any market, including a labor market, the starting place is to determine whether the merged firm collectively wielded market power in some relevant antitrust market. That inquiry can be informed with both direct and indirect evidence.

Direct evidence of buying power, as the name suggests, is evidence that directly shows a buyer has power to reduce wages or exclude rivals. Indirect evidence of buying power can be established by showing high market shares (plus entry barriers) in a relevant antitrust market. It bears noting that, when it comes to labor markets, high market shares are not strictly needed to infer buying power due to high search and switching costs (often absent in output markets).

Beginning with the direct evidence, Activision exhibited traits of a firm with buying power over its workers. For example, before it was acquired, Activision undertook an aggressive anti-union campaign against its workers’ efforts to organize a union. Moreover, workers at Activision complained about their employer’s intransigent position on granting raises, often demanding proof of an outside offer. A recent article in Time recounted that “Several former Blizzard employees said they only received significant pay increases after leaving for other companies, such as nearby rival Riot Games, Inc. in Los Angeles.” Activision also entered a consent decree in 2022 with the Equal Employment Opportunity Commission to resolve a complaint alleging Activision subjected its workers to sexual harassment, pregnancy discrimination, and retaliation related to sexual harassment or pregnancy discrimination.

Moving to the indirect evidence, one could posit a labor market for video game workers at AAA gaming studios. Both Microsoft and Activision are AAA studios, making them a preferred destination for industry labor. Independent studios are largely regarded as temporary stepping stones toward better positions in large video game firms.

To estimate the merged firm’s combined share in the relevant labor market, in a forthcoming paper, Ted Tatos and I study CareerBuilder’s Supply and Demand data, filtering on the term “video game” in the United States to recover job applications and postings over the last two years. The table summarizes the results of our search in the Spring 2022, a few months after the Microsoft-Activision deal was announced. Our analysis conservatively includes small employers that workers at a AAA studio such as Activision likely would not consider to be a reasonable substitute.

Job Postings Among Top Studios in Video Game Industry – CareerBuilder Data

| Company Name | Number of Job Postings | Percent of Postings | Corporate Entity |

| Activision Blizzard, Inc. | 1,270 | 26.0% | Microsoft |

| Electronic Arts Inc. | 856 | 17.5% | |

| Rockstar Games, Inc. | 287 | 5.9% | Take-Two |

| Ubisoft, Inc. | 258 | 5.3% | |

| 2k, Inc. | 143 | 2.9% | Take-Two |

| Zenimax Media Inc. | 128 | 2.6% | Microsoft |

| Epic Games, Inc. | 112 | 2.3% | |

| Lever Inc | 106 | 2.2% | |

| Wb Games Inc. | 101 | 2.1% | |

| Survios, Inc. | 100 | 2.0% | |

| Riot Games, Inc. | 91 | 1.9% | Tencent |

| Zynga Inc. | 84 | 1.7% | Take-Two |

| Funcom Inc | 79 | 1.6% | Tencent |

| 2k Games, Inc. | 74 | 1.5% | Take-Two |

| Complete Networks, Inc. | 65 | 1.3% | |

| Gearbox Software | 58 | 1.2% | Embracer |

| Digital Extremes Ltd | 43 | 0.9% | Tencent |

| Naughty Dog, Inc. | 43 | 0.9% | Sony |

| Mastery Game Studios, LLC | 26 | 0.5% | |

| Crystal Dynamics Inc | 25 | 0.5% | Embracer |

| Skillz Inc. | 25 | 0.5% | |

| Microsoft Corporation | 24 | 0.5% | Microsoft |

| Others | 887 | 18.2% | |

| TOTAL | 4,885 | 100.0% |

As indicated in the first row, Activision lies at the top in number of job postings in the CareerBuilder data, with 26.0 percent. Prior to the Activision acquisition, Microsoft accounted for 3.1 percent of job postings (the sum of Zenimax Media and Microsoft rows). Based on these figures, Microsoft’s acquisition of Activision significantly increased concentration (by more than 150 points) in an already concentrated market (post-merger HHI above 1,200). This finding implies that the merger could lead to anticompetitive effects in the relevant labor market, including layoffs.

It bears noting that the HHI thresholds established in the 2023 Merger Guidelines (Guideline 1) were most likely developed with product markets in mind. Indeed, the Guidelines recognize in a separate section (Guideline 10) that labor markets are more vulnerable to the exercise of pricing power than output markets: “Labor markets frequently have characteristics that can exacerbate the competitive effects of a merger between competing employers. For example, labor markets often exhibit high switching costs and search frictions due to the process of finding, applying, interviewing for, and acclimating to a new job.” High switching costs are also present in the video game industry: Almost 90 percent of workers at AAA studios in the CareerBuilder Resume data indicate that they did not want to relocate, making them more vulnerable to an exercise of market power than the HHI analysis above implies.

As any student of economics recognizes, a monopsonist not only reduces wages below competitive levels, but also restricts employment relative to the competitive level. So the immediate firing of 1,900 workers is consistent with the exercise of newfound monopsony power. In technical terms, the layoffs could reflect a change in the residual labor supply curve faced by the merged firm.

Why would Microsoft exercise its newfound buying power this way? To begin, many Microsoft workers, prior to the merger, could have switched to Activision in response to a wage cut. Indeed, we were able find in the CareerBuilder data that a substantial fraction of former Microsoft workers left Microsoft Game Studios to work for Activision. (More details on the churn rate to come in our forthcoming paper.) Post-merger, Microsoft was able to internalize this defection, weakening the bargaining position of its employees, and putting downward pressure on wages. In other words, Microsoft is more disposed to cutting Activision jobs than would a standalone Activision. Moreover, by withholding Activision titles from competing multi-game subscription services—the FTC’s primary theory of harm in its litigation, now under appeal—Microsoft can give an artificial boost to its platform division. This input foreclosure strategy would compel Microsoft to downsize its gaming division and thus its gaming division workers.

Alternative Explanations Don’t Ring True

The contention that these 1,900 layoffs flowed from the merger, as opposed to some other force, is supported in the economic literature in other labor markets. A recent paper by Prager and Schmitt (2021) studied the effect of a competition-reducing hospital merger on the wages of hospital staff. Consistent with economic theory, the merger had a substantial negative effect on wages for workers whose skills are much more useful in hospitals than elsewhere (e.g., nurses). In contrast, the merger had no discernable effect on wages for workers whose skills are equally useful in other settings (e.g., custodians). As Hemphill and Rose (2018) explain in their seminal Yale Law Journal article, “A merger of competing buyers can exacerbate the merged firm’s incentive to buy less in order to drive down input prices.”

Microsoft has its defenders in academia. According to Joost van Dreunen, a New York University professor who studies the gaming business, the video game industry is “suffering through a winter right now. If everybody around you is cutting their overhead and you don’t, you’re going to invoke the wrath of your shareholders at some point.” (emphasis added) This point—which sounds like it was fed by Microsoft’s PR firm—is intended to suggest that the firings would have occurred absent the merger. But there are two problems with this narrative. First, Microsoft’s gaming revenues are booming (up nine percent in the first quarter of its 2024 fiscal year), which makes industry comparables challenging. What were the layoffs among video game firms that also grew revenues by nine percent? Second, video programmers and artists are not “overhead,” such as HR workers or accountants. (Apologies to those workers.) Thus, their firing cannot be attributed to some redundancy in deliverables.

Microsoft’s own press statement about the layoffs vaguely states that it has “identified areas of overlap” across Activision and its former gaming unit. But that explanation is just as consistent with the labor-market harm articulated here as with the “eliminating redundancy” efficiency.

Bobby Kotick, the former CEO of Activision, received a $400 million golden parachute at the end of the year for selling his company to Microsoft. That comes to about $210,500 per fired employee, or about two years’ worth of severance for each worker laid off. Too bad those resources were so regressively assigned.

The Federal Trade Commission’s scrutiny of Microsoft’s acquisition of game producer Activision-Blizzard did not end as planned. Judge Jacqueline Scott Corley, a Biden appointee, denied the FTC’s motion for preliminary injunction, ruling that the merger was in the public interest. At the time of this writing, the FTC has pursued an appeal of that decision to the Ninth Circuit, identifying numerous reversible legal errors that the Ninth Circuit will assess de novo.

But even critics of Judge Corley’s opinion might find agreement on one aspect: the relative lack of enforcement against anticompetitive vertical mergers in the past 40+ years. As Corley’s opinion correctly observes, United States v. AT&T Inc, 916 F.3d 1029 (D.C. Circuit 2019), is the only court of appeals decision addressing a vertical merger in decades. Absent evolution of the law to account for, among other recent phenomena, the unique nature of technology-enabled content platforms, the starting point for Corley’s opinion is misplaced faith in case law that casts vertical mergers as inherently pro-competitive.

As with horizontal mergers, the FTC and Department of Justice have historically promulgated vertical merger guidelines that outline analytical techniques and enforcement policies. In 2021, the Federal Trade Commission withdrew the 2020 Vertical Merger Guidelines, with the stated intent of avoiding industry and judicial reliance on “unsound economic theories.” In so doing, the FTC committed to working with the DOJ to provide guidance for vertical mergers that better reflects market realities, particularly as to various features of modern firms, including in digital markets.

The FTC’s challenge to Microsoft’s proposed $69 billion acquisition of Activision, the largest proposed acquisition in the Big Tech era, concerns a vertical merger in both existing and emerging digital markets. It involves differentiated inputs—namely, unique content for digital platforms that is inherently not replaceable. The FTC’s theories of harm, Judge Corley’s decision, and the now-pending appeal to the Ninth Circuit provide key insights into how the FTC and DOJ might update the Vertical Merger Guidelines to stem erosion of legal theories that are otherwise ripe for application to contemporary and emerging markets.

Beware of must-have inputs

In describing a vertical relationship, an “input” refers to goods that are created “upstream” of a distributor, retail, or manufacturer of finished goods. Take for instance the production and sale of tennis shoes. In the vertical relationship between the shoe manufacturer and the shoe retailer, the input is the shoe itself. If the shoe manufacturer and shoe retailer merge, that’s called a vertical merger—and the input in this example, tennis shoes, is characteristic of a replaceable good that vertical merger scrutiny has conventionally addressed. If such a merger were to occur and the newly-merged firm sought to foreclose rival shoe retailers from selling its shoes, rival shoe retailers would likely seek an alternative source for tennis shoes, assuming the availability of such an alternative.

When it comes to assessing vertical mergers in digital content markets, not all inputs are created equal. To the contrary, online platforms, audio and video streaming platforms, and—in the case of Microsoft’s proposed acquisition of Activision—gaming platforms all rely on unique intellectual property that cannot simply be replicated if a platform’s access to that content is restricted. The ability to foreclose access to differentiated content that flows from the merger of a content creator and distributor creates a heightened concern of anticompetitive effects, because rivals cannot readily switch to alternatives to the foreclosed product. This is particularly true when the foreclosed content is extremely popular or “must-have,” and where the goal of the merged firm is to steer consumers toward the platform where it is exclusively available. (See also Steven Salop, “Invigorating Vertical Merger Enforcement,” 127 Yale L.J. 1962 (2018).)

The 2020 Vertical Merger Guidelines fall short in their analysis of mergers involving highly differentiated products. The guidelines emphasize that vertical mergers are pro-competitive when they eliminate “double marginalization,” or mark-ups that independent firms claim at different levels of the distribution chain. For example, when game consoles purchase content from game developers, they may decide to add a mark-up on that content before offering it for consumer consumption. (In the real world of predatory pricing and cross-subsidization, the incentive to add such a mark-up is a more complex business calculation.) Theoretically, the elimination of those markups creates an incentive to lower prices to the end consumer.

But this narrow focus on elimination of double marginalization—and theoretical downward price pressure for consumers—ignores how the reduction in competition among downstream retailers for access to those inputs can also degrade the quality of the input. Let’s take Microsoft-Activision as an example. As an independent firm, Activision creates games and downstream consoles engage in some form of competition to carry those games. When consoles compete on terms to carry Activision games, the result to Activision includes greater investment in game development and higher quality games. When Microsoft acquires Activision, that downstream competition for exclusive or first-run access to Activision’s games is diminished. Gone is the pro-competitive pressure created by rival consoles bidding for exclusivity, as is the incentive for Activision to innovate and demand greater third-party investment in higher quality games.

Emphasizing the pro-competitive effects of eliminating double marginalization—even if that means lower prices to consumers—only provides half of the picture, because consumers will likely be paying for lower quality games. Previous iterations of the Vertical Merger Guidelines emphasize the consumer benefits of eliminating double marginalization, but they stop short of assessing the countervailing harms of mergers involving differentiated inputs. They should be updated accordingly.

Partial foreclosure will suffice

During the evidentiary hearings in the Northern District of California, the FTC repeatedly pushed back against the artificially high burden of having to prove that Microsoft had an incentive to fully foreclose access to Activision games. In the midst of an exchange during the FTC’s closing arguments, FTC’s counsel put it directly: “I don’t want to just give into the full foreclosure theory. That’s another artificially high burden that the Defendants have tried to put on the government.” And yet, in her decision, Judge Corley conflates the analysis for both full and partial foreclosure, writing, “If the FTC has not shown a financial incentive to engage in full foreclosure, then it has not shown a financial incentive to engage in partial foreclosure.”

Although agencies have acknowledged that the incentive to partially foreclose may exist even in the absence of total foreclosure (see, for instance, the FCC’s 2011 Order regarding the Comcast-NBCU vertical transaction), the Vertical Merger Guidelines do not make any such distinction. Again, that incomplete analysis hinges in part on the failure to distinguish between types of inputs. Take for instance a producer of oranges merging with a firm that makes orange juice. Theoretically, the merged firm might fully foreclose access to oranges to rival orange juice makers, who may then go in search for alternative sources of oranges. Or the merged firm might supply lower quality produce to rival firms, which may again send it in search of an alternative source.

But a merged firm’s ability and incentive to foreclose looks different when foreclosure takes the subtler form of investing less in the functionality of game content with a gaming console, subtly degrading game features, or adding unique features to the merged firm’s platforms in ways that will eventually drive more astute gamers to the merged firm (even though the game in question is technically still available on rival consoles). Such eventualities are perhaps easier to imagine in the context of other content platforms—for example, if news content were less readable on one social media platform than another. When a merged firm has unilateral control over those subtle design and development decisions, the ability and incentive to engage in more subtle forms of anticompetitive partial foreclosure is more likely and predictable.

In finding that Microsoft would not have a financial incentive to fully foreclose access to Activision games, Judge Corley’s analysis hinges on a near-term assessment of Microsoft’s financial incentive to elicit game sales by keeping games on rival consoles. (Never mind that Microsoft is a $2.5 trillion corporation that can afford near-term losses in service of its longer-view monopoly ambitions.) Regardless, a theory of partial foreclosure does not mean that Microsoft must forgo independent sales on rival consoles to achieve its ambitions. To the contrary, partial foreclosure would still allow users to purchase and play games on rival consoles. But it also allows for Microsoft’s incentive to gradually encourage consumers to use its own console or game subscription service for better game play and unique features.

Finally, Judge Corley’s analysis of Microsoft’s incentive to fully foreclosure is irresponsibly deferential to statements made by Activision Blizzard CEO Bobby Kotick that the merging entities would suffer “irreparable reputational harm” if games were not made available on rival consoles. Again, by conflating the incentives for full and partial foreclosure, the court ignores Microsoft’s ability to mitigate that reputational harm—while continuing to drive consumers to its own platforms—if foreclosure is only partial.

Rejecting private behavioral remedies

In a particularly convoluted passage in the district court’s order, the Court appears to read an entirely new requirement into the FTC’s initial burden of demonstrating a likelihood of success on the merits—namely, that the FTC must assess the adequacy of Microsoft’s proposed side agreements with rival consoles and third-party platforms to not foreclose access to Call of Duty. Never mind that these side agreements lack any verifiable uniformity, are timebound, and cannot possibly account for incentives for partial foreclosure. Yet, the Court takes at face value the adequacy of those agreements, identifying them as the principal evidence of Microsoft’s lack of incentive to foreclose access to just one of Activision’s several AAA games.

In its appeal to the Ninth Circuit, the FTC seizes on this potential legal error as a basis for reversal. The FTC writes, “in crediting proposed efficiencies absent any analysis of their actual market impact, the district court failed to heed [the Ninth Circuit’s] observation ‘[t]he Supreme Court has never expressly approved an efficiencies defense to a Section 7 claim.’” The FTC argues that Microsoft’s proposed remedies should only have been considered after a finding of liability at the subsequent remedy stage of a merits proceeding, citing the Supreme Court’s decision in United States v. Greater Buffalo Press, Inc., 402 U.S. 549 (1971). Indeed, federal statute identifies the Commission as the expert body equipped to craft appropriate remedies in the event of a violation of the antitrust laws.

In its statement withdrawing the 2020 Vertical Merger Guidelines, the FTC announced it would work with the Department of Justice on updating the guidelines to address ineffective remedies. Presumably, the district court’s heavy reliance on Microsoft’s proposed behavioral remedies is catalyst enough to clarify that they should not qualify as cognizable efficiencies, at least at the initial stages of a case brought by the FTC or DOJ.

If this decision has taught us anything, it is that the agencies can’t come out with the new Merger Guidelines fast enough. In particular, those guidelines must address the competitive harms that flow from the vertical integration of differentiated content and digital media platforms. Even so, updating the guidelines may be insufficient to shift a judiciary so hostile to merger enforcement that it will turn a blind eye to brazen admissions of a merging firm’s monopoly ambitions. If that’s the case, we should look to Congress to reassert its anti-monopoly objectives.

Lee Hepner is Legal Counsel at the American Economic Liberties Project.

On Wednesday, the UK Competition and Markets Authority (CMA) provisionally concluded that Microsoft’s proposed acquisition of Activision could result in higher prices, fewer choices, or less innovation for UK gamers. It also released a set of proposed remedies to address the likely anticompetitive harms, including a mandatory divestiture of (1) Activision’s business associated with its popular Call of Duty franchise; (2) the entirety of the Activision segment; or (3) the entirety of both the Activision segment and the Blizzard segment, which would also cover the World of Warcraft franchise.

Assuming Microsoft won’t go for any structural remedy, the deal is likely on ice, and the U.S. Federal Trade Commission (FTC) would not have to bring any enforcement action against Microsoft. Although this is likely the right outcome from a competition perspective, the antitrust geeks (myself included) will suffer dearly from not getting to observe the theatrics around a hearing and the associated written decisions.

Setting aside Microsoft’s significant holdings in gaming studios, Microsoft’s attempted purchase of Activision can be understood as a vertical merger, in the sense that Microsoft sells its Xbox gaming platform (the downstream division) to consumers, in competition against Sony’s PlayStation and Nintendo’s Switch—and Activision supplies compelling games (the upstream division) for the various gaming platforms. The Xbox platform can be understood either as Microsoft’s traditional gaming console or as its nascent cloud-based Xbox Game Pass platform.

Challenges of vertical mergers have not been successful of late, prompting many scholars to call for new vertical merger guidelines. Among the suggested remedies would be a “dominant platform presumption,” advocated by antitrust law professor Steve Salop, which would shift the burden of proof to the acquiring firm whenever it was deemed a dominant platform.

It’s All About the Departure Rate

Input foreclosure is the term used by economists to describe how a vertically integrated firm—think post-merger Microsoft—might withhold a key input from distribution rivals, thereby impairing the rivals’ ability to compete for customers. When the theory of harm is input foreclosure, proof of anticompetitive effects largely turns on how special or “must-have” the potentially withheld input is for downstream rivals. Economists define the “departure rate” as the share of the rival’s customers who would defect if they could not access the withheld input. Under these models, anticompetitive effects also require that the downstream firm possess a significant market share.

In the Justice Department’s attempt to block AT&T’s acquisition of Time Warner in 2018, the agency’s economic expert leaned on an estimated departure rate generated by a third-party consultant. That third-party consultant originally produced results consistent with a low departure rate, suggesting that losing CNN would not cause too much customer defection, only to be changed to a high departure rate before being handed to the economic expert for incorporation into his work. Regardless of how the work was performed, it strained credulity that CNN was considered a must-have input by cable distribution rivals and their customers. Moreover, AT&T’s (local) share of the distribution market, even in its limited footprint, was not substantial.

In contrast, Microsoft wields a commanding share of gaming platforms, by some estimates as high as 60 to 70 percent of global cloud gaming, but only 25 percent of gaming consoles per Ampere Analytics. Call of Duty is considered a must-have input among gaming platforms, based in part on CMA’s analysis of internal “data on how Microsoft measures the value of customers in the ordinary course of business.” For modeling purposes, it still would be incumbent on the agency’s economist to measure the departure rate, and here it might be difficult to find a natural experiment—for example, where a platform temporarily lost access to Call of Duty—to exploit. As part of its investigation, CMA “commission[ed] an independent survey of UK gamers,” which could have been used to asked Call of Duty users whether they might leave a platform if they couldn’t access their favorite game. CMA noted that Microsoft has already employed a strategy “of buying gaming studios and making their content exclusive to Microsoft’s platforms … following several previous acquisitions of games studios.”

Microsoft has made commitments to Sony and Nintendo to continue releasing its new Call of Duty games for ten years. Yet such commitments are hard to enforce, and could be undermined through trickery. For example, Microsoft could offer access only at some unreasonable price, or only under unreasonable conditions in which (say) the rival platform also agreed to purchase a set of boring games, alongside Call of Duty, at a supracompetitive price. Without a regulator to oversee access, the commitment could be ephemeral, much like T-Mobile’s access commitment to Dish, to remedy T-Mobile’s acquisition of Sprint, which is widely recognized as a farce. Despite its disfavor of behavioral remedies, CMA noted in its notice of possible remedies that it would nevertheless “consider a behavioural access remedy as a possible remedy,” yet concludes that the agency is “of the initial view that any behavioural remedy in this case is likely to present material effectiveness risks.”

Microsoft reportedly entered into a neutrality agreement with organized labor, under which Microsoft would not impair progress towards unionization of Activision employees. Whatever benefits such an agreement might generate for workers, those benefits could not be used to offset the harms suffered by consumers in the product markets under Philadelphia National Bank. Unfortunately, the treatment of offsets is not as clear under monopolization law.

What Goes Around Comes Around

If CMA’s actions ultimately stop the Microsoft-Activision merger, the relatively weaker merger enforcement in the United States would get a pass. U.S. antitrust agencies are readying a revised and more stringent set of merger guidelines, which would bring U.S. standards in line with European authorities. In the meantime, the global reach of the dominant tech platforms—and thus exposure to foreign antitrust regimes—might ironically protect U.S. consumers from the platforms’ most audacious lockups.