Housing prices are up, and would-be homeowners are shifting to rental units. The inventory of homes for sale is shrinking because investors are buying up properties with cash offers. Investors then rent the homes to households who cannot afford mortgages. Many feel that the American dream of homeownership is slipping away. Building more homes won’t alleviate the problem if those additions are not in the right location or if investors buy them first.

To address this pinch, right after the New Year, President Trump called for Congress to cap the holdings of institutional investors in the housing market. A very reasonable idea, so long as it is implemented correctly.

Within days of the president’s announcement, the New York Times Opinion section featured an essay titled “The Landlords Are Not The Problem,” noting that institutional investors collectively own “less than 1 percent of the nation’s single-family homes—and less than 5 percent of single-family rentals.” That figure presumes that the relevant geographic area for studying investor pricing power is the nation. But housing investors are not randomly acquiring properties across the nation. Instead, they are selectively acquiring properties in neighborhoods to maximize their pricing power. This purchasing strategy, sometimes called “rentlining,” entails buying homes that are most likely to permit rent extraction from tenants who lack options. Measuring investor ownership using the nationwide housing stock as the denominator artificially deflates the true investor share of the markets in which they operate.

The Wealth Defense Industry Strikes Back

President Trump’s proposal sent members of what Matt Stoller aptly calls the “wealth defense” industry into overdrive. Jay Parsons, former chief economist of RealPage, was quick to tout a study by the American Enterprise Institute (AEI), a libertarian think tank that has been one of the loudest opponents of recent federal and state efforts to restrict investor homebuying. The AEI report, from August 2025, estimated that institutional investors owned a small share of single-family homes when looking at the national, county, and even zip code levels. That report offers the following analysis of single-family home ownership:

Institutional ownership of single-family homes is highly concentrated and varies significantly at the county level. Just 162 counties (or 5% of U.S. counties for which Parcl Labs data are available) account for 80% of all institutionally-owned homes, according to Parcl Labs data. Yet not a single county has a share greater than 10%…[E]ven in metros that have received significant media attention for their more pronounced investor presence, such as Atlanta (4.2%), Dallas (2.6%), and Houston (2.2%), these investors do not dominate any single neighborhood[…] In Atlanta, for instance, the highest institutional investor share in any ZIP Code is 12.4%, while half of its ZIP Codes have a share below 1.5%. No ZIP Code in Houston has an institutional investor share of over 10%[.]

Although this analysis may inspire faint hope as far as it shows that institutional investors haven’t yet taken over most U.S. housing markets, this analysis misses two valid concerns of affordable housing advocates: (1) concentration can be caused by large local players, regardless of their national or statewide holdings, and (2) neighborhoods, not zip codes, are the relevant geographic market.

Institutional Investors Aren’t the Only Source of Pricing Power

The current policy discourse has poorly defined the valid concerns about institutional housing investors. In recent bills proposed to regulate institutional investors, these investors are generally defined as an owner of one hundred or more residences. For example, Florida’s House Bill 1593 regulates the home-buying of a business that “has an interest in more than 100 single-family residential properties in this state.” The AEI report quoted above uses the same one-hundred-home designation. This definition misses the crux of the pricing power issue.

No housing advocate or economist has ever drawn a bright red line at one hundred units as the threshold for corporate pricing power. When scrutinizing the ability of businesses to coordinate and set artificially high prices, economists measure the overall concentration of the relevant market, regardless of the asset portfolio of the participants. Moreover, sometimes different firms that purchase homes are subsidiaries of a larger firm, so a firm may appear to be a small investor but actually be just a tentacle of a larger corporate entity.

In this instance, a more accurate analysis of pricing power examines which local housing markets are controlled by a few big players, rather than analyzing arbitrary ownership thresholds. Owning just five homes in the same neighborhood reasonably conveys investor status, regardless of whether the owner is an institutional investor.

Taking this more expansive view of market concentration allows us to measure pricing power in individual housing markets regardless of national (or statewide) asset portfolios.

Measure Neighborhoods, Not Zip Codes

A second issue with AEI’s claims is that market power must be evaluated in a relevant geographic market. The Merger Guidelines compel us to ask, how much contiguous real estate would a hypothetical landlord have to acquire in order to raise rents over competitive levels? Although zip codes can be a useful and relevant unit of observation, zip code boundaries do not necessarily reflect the areas within which a renter or homebuyer considers their options. A medical student at University of Miami who lives in the trendy Brickell neighborhood for easy access to the metro station (and a short ride to the medical campus) would not consider any apartment in the 33130 zip code as a substitute.

To study this issue, we focused on Atlanta, as the AEI study provided institutional market shares by zip code there. Fulton County provides a map of all official neighborhoods in Atlanta, which we combined with a dataset containing all tax parcels in the county to identify all single-family homes in Atlanta by neighborhood.

Because there are approximately four times as many official neighborhoods as zip codes in Atlanta, neighborhoods provide a more narrowly defined set of smaller geographic housing markets relative to AEI’s zip code analysis. Furthermore, renters and buyers both seem more likely to deliberately target neighborhoods rather than zip codes when searching for their next home.

Neighborhood Market Power Analysis

We assembled a dataset of approximately 75,000 single family homes in Atlanta. We identified homes owned by an LLC or other business entity, and we also identified “investor owners,” which we define as homeowners who own at least five homes within a given neighborhood. The vast majority of investor owners are business entities. In line with AEI’s research, we find that investor owners hold a small share of homes in most Atlanta neighborhoods.

While AEI asserts that investor owners do not hold over 12 percent of homes anywhere in Atlanta, we identified Atlanta neighborhoods where investor owners held larger shares of single-family homes. Investor shares of the housing stock are especially large when we exclude owner-occupied homes from the analysis, considering only those homes that are currently empty or occupied by renters.

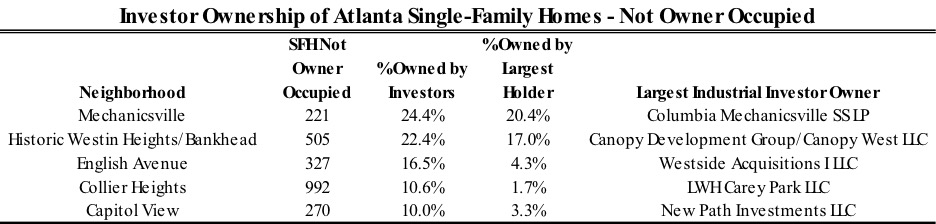

A prominent example is Historic Westin Heights/Bankhead, a neighborhood just outside of Atlanta’s downtown. Bankhead’s single-family housing stock is dominated by Canopy Development Group, which holds 11 percent of all homes in the neighborhood and 17 percent of homes that are not owner-occupied. (According to its website, Canopy “is leading the largest land and property acquisition effort in Atlanta’s Westside Beltline area.” Per the Atlantic Journal-Constitution, Canopy “has used anonymous limited liability corporations to buy up large portions of west Atlanta’s impoverished English Avenue neighborhood.” While Canopy has developed properties as well, it obtained its status via acquisition.). Mechanicsville, named for the mechanics who worked on the rail line, is another neighborhood community with substantial investor ownership, with investors holding 14 percent of all homes and 24 percent of homes that are not owner-occupied.

We identified three other Atlanta neighborhoods with at least 350 single-family homes where at least 10 percent of homes that are not owner-occupied are owned by investors.

It is worth noting that three of the five neighborhoods highlighted by this analysis (Bankhead, Collier Heights, and Capitol View) are among the “Beltline” neighborhoods, communities adjacent to a major urban renewal project. The Beltline project has displaced many long-tenured homeowners in Atlanta, making their former homes available to large-scale landlord investors.

High Shares in a Neighborhood Are Consistent with Direct Evidence

Given the low investor shares at the zip code level (implying lack of pricing power), and given the high investor shares in certain neighborhoods, one can look to direct evidence of investors’ pricing power to resolve the dispute. If investors can be shown to inflate rents, then the narrower geographic market is consistent with the direct evidence of pricing power.

There is a large and growing literature demonstrating the inflationary effect of these types of institutional holdings on rental prices in local housing markets. A July 2020 working paper from St. Louis Fed economists investigated the effect of institutional investors —defined as “entities who purchase multiple housing units under the name of an LLC, LP, Trust, REIT, etc.” — on rental prices. The economists found that institutional investors increase the price-to-income ratio of rental properties, especially in the bottom price-tier. In an antitrust court, such evidence would be considered “direct” evidence of the pricing power of institutional investors, which obviates the need to define a market, estimate share, and infer market power through high market shares.

In another study of rental pricing, Watson and Ziv (2021) analyzed the relationship between ownership concentration and rents in New York City, finding that a ten percent increase in concentration is correlated with a one percent increase in rents. This finding suggests that policymakers should be concerned about concentration of ownership, regardless of whether concentration is comprised of institutional investors or smaller investors.

These findings importantly hold even when looking within individual neighborhoods over time. Using mergers of private-equity backed firms to isolate quasi-exogenous variation in concentration of ownership at the neighborhood level, Austin (2022) found that shocks to institutional ownership cause higher prices and rents. This finding suggests that the association between institutional ownership and higher prices isn’t merely selection bias (institutional investors happening to invest in hot housing markets).

Neighborhood Ownership Caps Make Sense

Although AEI and other housing concentration skeptics are correct that regulating corporate landlords is not a silver bullet to address the ongoing affordability crisis, their analysis and rhetoric understate the reality of housing investor ownership.

A landlord does not need to own one hundred properties in a state to contribute to the concentration of economic power. Corporate landlords target neighborhoods where homes can be purchased cheaply and rented out profitably because renters in that area have limited choices. These renters’ options are limited in part because this targeted approach creates market power in the neighborhood-level housing market.

Landlords, especially those owning many homes in a single community, are part of the housing crisis, especially in rentlined communities like Bankhead in Atlanta. Regulating the accumulation and exercise of market power will always be part of a holistic solution to market failure. Our analysis suggests that a modest cap on the share of rental properties in a neighborhood that a single investor could own—say, of five or ten percent—could weaken the grip of investors and give renters some much-needed relief.